Last Update 31 Jul 26

Fair value Decreased 78%PSQH: NYSE Compliance Path And Planned Reverse Split Will Unlock Upside

Analysts have revised their price target on PSQ Holdings from $67.50 to $15.00, citing updated assumptions around revenue growth, profit margins, and a lower future P/E multiple.

What’s in the News for PSQ Holdings

- PSQ Holdings received notice that the New York Stock Exchange accepted its plan to regain compliance with listing standards, with an 18 month period from February 10, 2026, to meet Section 802.01B requirements and six months to address Section 802.01C, while the stock remains listed during this review period. Source NYSE compliance update.

- At the July 9, 2026 annual meeting, PSQ Holdings stockholders approved an amendment to the Restated Certificate of Incorporation that allows a reverse stock split of Class A common stock at a ratio between 1 for 5 and 1 for 15, to be implemented at the discretion of the Board of Directors. Source company meeting results.

- PSQ Holdings plans a 1 for 15 stock split or significant stock dividend on July 13, 2026, as recorded in corporate actions. Source corporate actions filing.

- Crecera Brands selected PSQ Payments as its payment processing provider and expects to migrate processing for core brands including Sportsman's Guide, The Golfer's World, and PlayBaseball to PSQ’s platform in early July 2026, with potential access to PSQ’s broader financial technology tools over time. Source client announcement.

- PSQ Holdings onboarded Dream Hunts, LandTrust's hunting experience business, within 48 hours after its previous processor shut off the account, restoring payment processing during the Spring hunting season and highlighting PSQ’s focus on merchants in outdoor recreation and other niche sectors. Source client announcement.

Valuation Changes for PSQ Holdings

- Fair Value has been reduced significantly, moving from $67.50 to $15.00 per share.

- Discount Rate is unchanged at 12.46%, indicating the same assumed cost of capital in the updated analysis.

- Revenue Growth expectations have been adjusted lower, from 41.80% to 36.84%.

- Profit Margin assumptions are effectively flat, moving slightly from 8.33% to 8.32%.

- Future P/E multiple has been cut sharply, from 34.67x to 14.81x, which contributes to the lower fair value estimate for PSQ Holdings.

Key Takeaways

- Focus on specialized fintech solutions and AI-driven credit processes boosts user growth, efficiency, and positions the company for revenue and margin expansion.

- Streamlining operations through divestitures and cost controls enhances profitability and allows concentration on high-growth business areas.

- Reliance on a single fintech segment, narrow customer focus, rising competition, regulatory risks, and potential capital constraints threaten long-term stability and profitability.

Catalysts

About PSQ Holdings- Operates an online marketplace through advertising and eCommerce in the United States.

- The company is capitalizing on increasing consumer demand for values-based commerce by sharply focusing its operations on fintech solutions that explicitly serve merchants and consumers who feel underserved by traditional financial institutions-this enhances potential for accelerated user acquisition, payment volume growth, and revenue expansion.

- Their evolving product suite-with an imminent rollout of crypto payments, private label card programs, and loyalty tools-caters to the growing migration toward digital, privacy-focused, and independent commerce platforms, likely increasing transaction volumes and enabling the entrance into new, high-margin revenue streams, driving future revenue and margin uplift.

- Early adoption and continued investment in AI-driven credit underwriting has already reduced default rates sharply and is expected to improve credit portfolio performance and operational efficiency going forward, supporting lower credit losses and expanding earnings.

- Strategic divestiture of non-core segments (EveryLife, Marketplace) is set to generate non-dilutive capital, reduce operating complexity, and allow a laser focus on high-growth fintech operations, all contributing to improved net margins and earnings.

- Ongoing operating expense reductions and efficiency gains following last year's reorganization, paired with above-industry revenue growth, lay the foundation for sustainable margin expansion and progress toward profitability at scale.

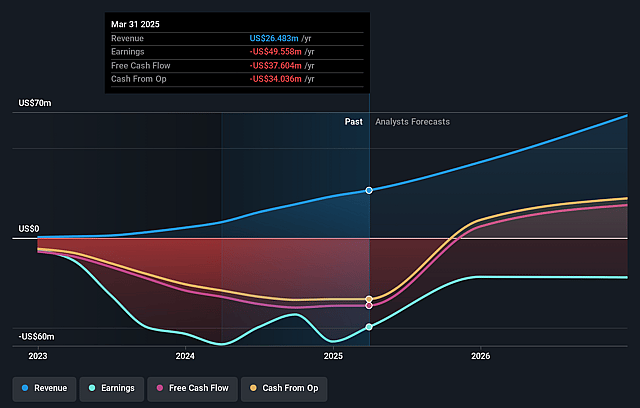

PSQ Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming PSQ Holdings's revenue will grow by 36.8% annually over the next 3 years.

- Analysts are not forecasting that PSQ Holdings will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate PSQ Holdings's profit margin will increase from -107.5% to the average US Interactive Media and Services industry of 8.3% in 3 years.

- If PSQ Holdings's profit margin were to converge on the industry average, you could expect earnings to reach $5.8 million (and earnings per share of $1.4) by about July 2029, up from -$29.1 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.2x on those 2029 earnings, up from -0.5x today. This future PE is lower than the current PE for the US Interactive Media and Services industry at 16.5x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The divestiture of both EveryLife and the Marketplace means PSQ Holdings will lose diversified revenue streams and will become entirely reliant on its fintech segment; this higher single-segment concentration could reduce long-term earnings stability and increase vulnerability to cyclical and industry-specific downturns.

- Heavy dependence on an ideologically targeted customer base ("values-aligned"/patriotic merchants and consumers) exposes the company to the risk of polarization fatigue, demographic shifts toward less ideologically engaged consumers, and ultimately lowers long-term scalability-potentially resulting in limited addressable market growth and revenue pressure.

- Increasing competition from mainstream financial and payments platforms-many of which may add "values-based" features-could compress PSQ's differentiators and require higher spending on customer acquisition and retention, eroding future net margins and profitability.

- The shift toward cryptocurrency payments and digital asset strategies introduces significant regulatory and technological risk; as privacy laws, crypto regulations, or DeFi standards evolve, unexpected compliance costs or technological challenges could negatively impact future earnings and operational margins.

- The company's recent share issuance via ATM offerings, balance-sheet retention of finance receivables, and reliance on lines of credit for credit product financing all point to potential long-term capital needs; if top-line growth or margin expansion stalls, future shareholder dilution or increased leverage may further pressure net income and shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $15.0 for PSQ Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $69.3 million, earnings will come to $5.8 million, and it would be trading on a PE ratio of 15.2x, assuming you use a discount rate of 12.5%.

- Given the current share price of $4.15, the analyst price target of $15.0 is 72.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on PSQ Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.