Last Update 12 May 26

Fair value Decreased 7.22%SSP: Expanding Women’s Sports Programming On ION Will Support Future Upside

Analysts have trimmed their price target for E.W. Scripps by $0.50 to $6.43, citing updated assumptions that combine a slightly higher discount rate with more modest revenue growth expectations and a lower future P/E, partially offset by a stronger projected profit margin.

What's in the News

- Scripps Sports agreed a multi-year broadcast partnership with Professional Bull Riders to air Premier Women’s Rodeo on ION and Grit starting in May, including the 2026 PWR Championship from Fort Worth, Texas. (Key Developments)

- The partnership is set to expand in 2027 with the original series "PWR: Road to the Championship" on Grit and a minimum of 18 hours of women’s rodeo programming across 16 broadcasts on ION and Grit. (Key Developments)

- The Premier Women’s Rodeo tie up is positioned to build on the Women’s Rodeo Championships platform and the Women’s Rodeo World Championship event, which is described as the industry’s richest women only rodeo championship. (Key Developments)

- Ally Financial and Scripps Sports partnered with the Professional Women's Hockey League to air the league’s first game on national linear television in the U.S., the PWHL Takeover Tour matchup between the New York Sirens and Montréal Victoire on ION Television. (Key Developments)

- ION, operated by E.W. Scripps, is described as reaching more than 126 million U.S. households through over the air, pay TV, connected TV and free ad supported streaming, and currently carries national broadcasts for multiple women’s sports leagues. (Key Developments)

Valuation Changes

- Fair Value: trimmed from $6.93 to $6.43, a modest reduction in the estimated value per share.

- Discount Rate: raised slightly from 12.33% to 12.46%, indicating a marginally higher required return in the model.

- Revenue Growth: revised from 3.89% to 1.46%, reflecting more cautious assumptions for future top line expansion.

- Profit Margin: adjusted up from 6.56% to 10.07%, implying a meaningfully higher expected level of profitability.

- Future P/E: reduced from 5.77x to 4.22x, pointing to a lower valuation multiple applied to projected earnings.

Key Takeaways

- Strong growth in streaming and live sports is driving higher ad revenue and margins, offsetting declines in traditional TV advertising.

- Strategic consolidation and disciplined debt management are improving operational efficiency, profitability, and reducing financial risk.

- Ongoing declines in traditional TV revenues, high debt, and slow digital adaptation threaten Scripps' earnings stability, cash flow, and long-term competitiveness.

Catalysts

About E.W. Scripps- Operates as a media enterprise through a portfolio of local television stations, national news, and entertainment networks in the United States.

- The company is rapidly expanding its reach and revenue through connected TV (CTV) and ad-supported streaming platforms, as demonstrated by a 57% year-over-year increase in CTV revenue and rapid streaming viewership growth for its Networks division. This positions Scripps to capture a larger share of advertising budgets shifting away from traditional cable and into digital platforms, supporting top-line growth and potentially increasing EBITDA margins.

- Scripps' significant investments in live sports broadcasting (WNBA, NWSL, NHL, NBA Finals) across both local and national networks are commanding premium ad rates and attracting new advertisers, helping to offset traditional core advertising softness and stabilizing/growing revenues and margins, particularly for its Networks.

- Anticipated deregulation in broadcast ownership rules and industry consolidation, including Scripps' recent station swap with Gray and the creation of new duopolies, is expected to improve operating leverage and profitability by enabling greater scale, operational efficiencies, and enhanced local programming, positively impacting future net margins and cash flow.

- The company expects ongoing margin improvement in its retransmission line due to rising leverage in negotiations with networks, declining fees paid to major networks, and disciplined portfolio optimization-supporting net margin expansion even amidst moderate subscriber losses.

- Robust execution in reducing leverage and extending debt maturities, combined with a focus on using operating cash flow for further debt reduction, is expected to materially reduce interest expense and financial risk over time, improving net income and free cash flow available to equity holders.

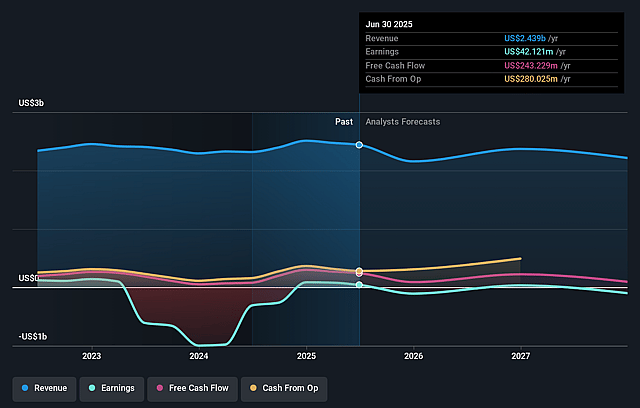

E.W. Scripps Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming E.W. Scripps's revenue will grow by 1.5% annually over the next 3 years.

- Analysts are not forecasting that E.W. Scripps will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate E.W. Scripps's profit margin will increase from -7.6% to the average US Media industry of 10.1% in 3 years.

- If E.W. Scripps's profit margin were to converge on the industry average, you could expect earnings to reach $225.3 million (and earnings per share of $2.16) by about May 2029, up from -$163.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 4.2x on those 2029 earnings, up from -2.1x today. This future PE is lower than the current PE for the US Media industry at 14.8x.

- Analysts expect the number of shares outstanding to grow by 4.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Continued decline in linear TV viewership, combined with a consistent mid-single-digit percentage decline in pay TV subscribers as indicated in the call, puts sustained pressure on core advertising and distribution revenues, directly impacting E.W. Scripps' top-line growth and long-term revenue stability.

- Heavy reliance on cyclical political and sports advertising revenues, which provided offsetting boosts in off-years but have not been sufficient to reverse overall local media revenue declines (down 8% year over year), exposes Scripps to volatility and impedes core earnings growth outside of election/major event cycles.

- Elevated debt levels from prior acquisitions, the recent refinancing at a 9 7/8% interest rate, and ongoing preferred equity with a growing unpaid dividend further increase interest expense and put pressure on cash flow and net income, constraining financial flexibility and elevating refinancing/coverage risks.

- High fixed costs, particularly in the local broadcast segment, combined with advertising category weakness (especially automotive) and management's acknowledgment of only flat to slightly down expense projections, limit margin improvement opportunities and could compress operating margins if revenues continue to weaken.

- The secular shift of advertisers toward digital, programmatic, and large platform alternatives (as noted by the CEO regarding the transformation of search and digital traffic) risks further erosion of Scripps' traditional ad base, particularly among younger demographics, jeopardizing future revenue, profit, and market share.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $6.42 for E.W. Scripps based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $10.0, and the most bearish reporting a price target of just $3.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.2 billion, earnings will come to $225.3 million, and it would be trading on a PE ratio of 4.2x, assuming you use a discount rate of 12.5%.

- Given the current share price of $3.79, the analyst price target of $6.42 is 41.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on E.W. Scripps?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.