Last Update 15 Apr 26

Fair value Decreased 25%KMD: Rights Offer Will Support Leaner Margins And Future Upside Potential

Analysts have revised their fair value estimate for KMD Brands from NZ$0.19 to NZ$0.14. This reflects updated assumptions for slightly lower revenue growth, slimmer profit margins and a higher future P/E multiple.

What's in the News

- KMD Brands has filed a follow-on equity offering totaling about NZ$65.27 million in ordinary shares. (Key Developments)

- The offering includes 623,049,203 ordinary shares at NZ$0.06 each, with a discount of NZ$0.00192 per security. (Key Developments)

- An additional 112,865,446 ordinary shares are offered at NZ$0.06 per share, also with a NZ$0.00192 discount per security. (Key Developments)

- A further 351,837,761 ordinary shares are included at NZ$0.06 per share, again with a NZ$0.00192 discount per security. (Key Developments)

- The transaction features a rights offering structure followed by a subsequent direct listing. (Key Developments)

Valuation Changes

- Fair Value Estimate reduced from NZ$0.19 to NZ$0.14 per share, indicating a material cut to the valuation anchor used in the model.

- Discount Rate unchanged at 12.35%, so the required return assumption remains consistent with the previous analysis.

- Revenue Growth assumption adjusted from 3.34% to roughly 2.91%, reflecting a slightly more conservative view on future top line expansion in NZ$ terms.

- Net Profit Margin revised from about 3.67% to roughly 2.21%, implying expectations for leaner profitability on NZ$ earnings.

- Future P/E lifted from 4.62x to about 5.85x, suggesting the shares are now modeled on a higher earnings multiple despite the lower fair value estimate.

Key Takeaways

- Investments in digital platforms, eCommerce and strategic marketing are expected to enhance online sales, brand recognition, and revenue growth.

- Store expansions and operational upgrades aim to boost direct-to-consumer sales and improve operational efficiency, supporting higher earnings and net margins.

- Persistently challenging wholesale recovery, margin pressures, and global uncertainties impact revenue growth and profitability, with intensified competition and elevated operating expenses adding further strain.

Catalysts

About KMD Brands- Designs, markets, wholesales, and retails apparel, footwear, and equipment for surfing and the outdoors under the Kathmandu, Rip Curl, and Oboz brands in New Zealand, Australia, North America, Europe, Southeast Asia, and Brazil.

- Significant investments in digital platforms and eCommerce enhancements across all brands, including Kathmandu’s redesign of its eCommerce mega menu and new payment methods, are expected to drive further online sales growth, impacting revenue positively.

- The ongoing focus on brand advertising, product innovation, and customer experience, particularly for Kathmandu as the official apparel partner for New Zealand's Olympic teams, is likely to enhance brand recognition and boost future sales, impacting both revenue and net margins.

- Planned strategic new store openings for Rip Curl in key growth markets like Europe and South America are anticipated to contribute to increased direct-to-consumer sales, which could improve earnings through higher-margin channels.

- Upgrades to group ERP systems and a focus on net working capital efficiency could enhance operational efficiency and reduce costs, potentially resulting in improved net margins.

- The reduction in net debt, with the group targeting debt below $50 million by the end of the year, positions the company for better financial flexibility in investing for growth or returning value to shareholders, positively impacting overall earnings per share.

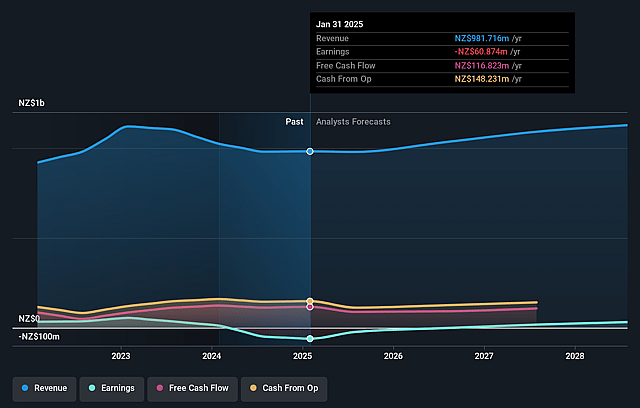

KMD Brands Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming KMD Brands's revenue will grow by 2.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from -8.5% today to 2.2% in 3 years time.

- Analysts expect earnings to reach NZ$24.7 million (and earnings per share of NZ$0.02) by about April 2029, up from -NZ$87.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 5.9x on those 2029 earnings, up from -1.1x today. This future PE is lower than the current PE for the AU Specialty Retail industry at 13.0x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.35%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The wholesale sales channel has been slow to recover, and there is ongoing cautiousness among wholesale accounts, impacting revenue and potentially constraining top-line growth.

- Gross margin pressure is persistent, particularly due to increased promotional intensity and competitive environments for brands like Kathmandu, which could deteriorate net margins.

- Economic and geopolitical uncertainties are contributing to challenging consumer sentiment globally, creating risks to sustaining revenue growth, particularly in North America and Europe, where sales are significant.

- Short-term liquidation by competitors in North America puts pressure on Rip Curl and may impact revenue growth and gross margins through competitive discounting.

- Elevated operating expenses, including strategic investments in marketing and store expansions, are challenging, especially without significant revenue growth, potentially affecting net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of NZ$0.14 for KMD Brands based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be NZ$1.1 billion, earnings will come to NZ$24.7 million, and it would be trading on a PE ratio of 5.9x, assuming you use a discount rate of 12.3%.

- Given the current share price of NZ$0.07, the analyst price target of NZ$0.14 is 52.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on KMD Brands?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.