Last Update 24 Jun 26

TRN: Discount Rate Tweaks May Support Future Upside Potential

Trainline's latest narrative update reflects a modest trimming of the analyst price target in £ terms, as analysts factor in slightly higher discount rates and a marginally higher assumed future P/E, while keeping revenue growth, profit margin and fair value estimates essentially unchanged.

Analyst Commentary

Recent research updates on Trainline point to a modest recalibration in price targets in £ terms, with analysts focusing on discount rates, assumed future P/E levels and the balance between valuation support and execution risk.

Bullish Takeaways

- Bullish analysts view the relatively small cuts of 5 GBp and 10 GBp to the price target as fine tuning rather than a shift in the core thesis, which still rests on Trainline delivering on existing revenue and margin assumptions.

- The decision to adjust the target primarily through the discount rate and assumed future P/E suggests that the underlying earnings profile used in models remains intact, which some investors may see as a sign of confidence in Trainline's operational execution.

- Keeping fair value estimates broadly stable, even as the discount rate is nudged higher, can be read as an indication that analysts still see Trainline's long term cash generation as broadly aligned with previous expectations.

- The focus on valuation inputs rather than cutting revenue or profit forecasts may support the view that, if Trainline executes consistently, there is still room for the stock to move toward analysts' updated fair value ranges over time.

Bearish Takeaways

- Bearish analysts highlight that two successive reductions in the price target, first by 5 GBp and then by 10 GBp, point to a more cautious stance on the risk profile embedded in Trainline's valuation.

- Higher discount rates in the models flag a greater perceived risk around Trainline's future cash flows, which can weigh on the multiple investors are willing to pay even if earnings forecasts are unchanged.

- The use of a marginally higher assumed future P/E while still cutting the price target indicates that, in spite of supportive multiple assumptions, Trainline's valuation headroom in current market conditions may be more limited than previously reflected.

- Repeated target trims, even if modest, can reinforce a wait and see attitude among more cautious investors, who may want clearer evidence of consistent execution before assigning Trainline a higher valuation.

What’s in the News for Trainline

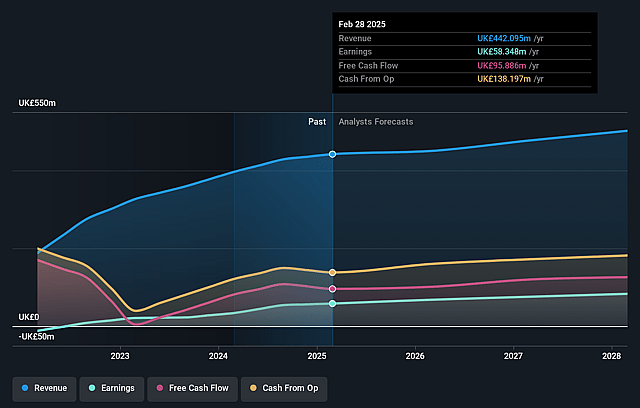

- Trainline issued earnings guidance for fiscal year 2027, with revenue expected in a range of €440 million to €455 million. (Source: Key Developments)

- Trainline completed a share buyback program announced on September 11, 2025, repurchasing 40,453,806 shares, representing 9.84% of the company, for £94 million between September 11, 2025 and April 30, 2026. (Source: Key Developments)

Valuation Changes for Trainline

- Fair Value: Modelled fair value per share remains unchanged at £3.51, with no adjustment to the underlying estimate.

- Discount Rate: The discount rate used in Trainline's valuation has risen slightly from 9.58% to 9.89%, indicating a modest increase in the risk input.

- Revenue Growth: Assumed future revenue growth is effectively unchanged at around 2.59%, with no material adjustment to the trajectory used in forecasts.

- Net Profit Margin: The long term profit margin assumption is stable at about 17.29%, reflecting no change in the earnings quality built into the model.

- Future P/E: The assumed future P/E multiple has risen slightly from 16.58x to 16.72x, representing a marginally higher valuation multiple applied to Trainline's projected earnings.

Key Takeaways

- EU market expansion and competition boost passenger volume, increasing net ticket sales and revenue growth, especially in Spain and Italy.

- Digitalization and ancillary services enhance operational efficiency and diversify income, projected to increase market share and revenue.

- Future growth and revenue may be challenged by U.K. market disruptions, international sales issues, and paused marketing due to carrier competition in France.

Catalysts

About Trainline- Engages in the operation of an independent rail and coach travel platform that sells rail and coach tickets the United Kingdom and internationally.

- The expansion of the third-party ticket retail market in the EU and increased carrier competition, particularly in Spain and Italy, are expected to drive more passenger volume, translating to higher net ticket sales and revenue growth.

- Digitalization and increased penetration of e-tickets in the U.K. are enhancing operational efficiencies and customer convenience, which can lead to increased market share in commuter rail, higher revenue, and better net margins.

- Cost optimization strategies, such as reducing headcount and increasing operating leverage, are projected to enhance net margins and EBITDA margins, impacting bottom-line earnings positively.

- The delay of Project Oval expansion potentially provides a tactical advantage by postponing competitive pressures in the U.K. market, helping maintain current revenue streams and market share.

- Trainline's innovation in ancillary revenue streams, through offering additional services like hotels and travel insurance within the booking flow, is diversifying income sources and is expected to drive additional revenue growth.

Trainline Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Trainline's revenue will grow by 2.6% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 17.6% today to 17.3% in 3 years time.

- Analysts expect earnings to reach £84.5 million (and earnings per share of £0.24) by about June 2029, up from £79.8 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.7x on those 2029 earnings, up from 9.5x today. This future PE is greater than the current PE for the GB Hospitality industry at 16.3x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.89%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The mention of an expected headwind from Transport for London's Project Oval expansion suggests potential future disruptions or challenges in the U.K. market, which could impact growth rates and revenue in the coming years.

- There are industry-wide changes to the presentation of Google's search engine results that have subdued web sales in International Consumer, particularly for foreign travel, which could negatively affect international revenue and market share.

- The decision to pause brand marketing in France due to insufficient carrier competition could lead to slowed growth and reduced revenue in that market until more competition enables more aggressive market positioning.

- The reduction in net commissions in the U.K., agreed back in 2022, poses a risk to Trainline's margins as it directly impacts the profitability and revenue per ticket.

- The uncertainty and timeline associated with regulatory changes and nationalization plans in the U.K., including consolidation in online ticketing platforms and ticket simplification, could impact the competitive landscape and future revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £3.51 for Trainline based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £5.8, and the most bearish reporting a price target of just £2.2.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £488.7 million, earnings will come to £84.5 million, and it would be trading on a PE ratio of 16.7x, assuming you use a discount rate of 9.9%.

- Given the current share price of £2.13, the analyst price target of £3.51 is 39.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Trainline?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.