Last Update 29 Jul 26

Fair value Increased 11%IP: Pricing Power And Plant Closures Will Shape Turnaround Prospects

International Paper's updated fair value estimate of $43.64, compared with $39.36 previously, reflects analysts' higher price targets and expectations for improved pricing power in containerboard following recent kraftliner and containerboard price increase announcements.

Analyst Commentary

Recent research on International Paper highlights a split view on the stock. There is a cluster of upgrades and higher price targets tied to containerboard pricing, while at the same time some analysts are stepping back and moving to more neutral ratings. The common thread is a focus on how well International Paper can execute on pricing and cost management in the current containerboard market.

Bullish Takeaways

- Bullish analysts see International Paper as strongly exposed to potential upside from higher kraftliner and containerboard prices, especially following the announced US$140 per ton price increase for U.S. kraftliner effective September 1.

- Recent upgrades, including JPMorgan moving to Overweight with a higher price target of US$61 from US$51, point to expectations that pricing and price or cost trends could support higher earnings power if execution on these increases holds.

- Several bullish analysts have raised price targets into the mid US$40s, citing improving supply and demand conditions in North American containerboard and updated estimates that reflect current input costs and market pricing.

- Some research highlights what is seen as a positive risk or reward profile at current share levels. International Paper is viewed as more leveraged to pricing shifts than certain peers, which is an important angle for investors focused on valuation sensitivity to price moves.

Bearish Takeaways

- Bearish analysts have moved International Paper to Neutral from Buy and trimmed or reset price targets in the low US$40s, reflecting caution around weaker demand and soft volumes across much of the broader packaging and paper group.

- Some commentary notes that while containerboard pricing efforts are under way, higher costs for freight, recycled fiber, chemicals, electricity and other inputs continue to weigh on margins. This could limit the benefit of any list price moves if cost inflation persists.

- Cautious views point to group stocks having already risen since earlier in the year. Combined with still "lackluster" demand in several end markets, this leads to a more balanced rather than clearly bullish stance on valuation for International Paper.

- Earlier reductions in price targets by several firms before the latest round of upgrades underscore that execution on pricing, cost control and Q2 and beyond results remains key before more investors are likely to gain confidence in a stronger growth or re-rating story for the stock.

What’s in the News for International Paper

- International Paper announced a US$140 per ton containerboard price increase effective September 1, citing higher costs for recycled fiber, freight and electricity, improving demand, and tighter supply after recent facility closures. Source: containerboard and boxboard price hike reports.

- Paper stocks, including International Paper, were the strongest performers in the S&P 500 on a recent Friday after reports of planned containerboard price increases, with International Paper shares up 11.2% for the day. Source: market performance coverage.

- International Paper plans to permanently close its Carrollton South packaging facility in Texas by the end of Q3 2026 as part of a broader plan to close five U.S. plants and align North American capacity with customer demand. Affected employees are set to receive severance, continued benefits, and outplacement support. Sources: company announcement and key developments.

- The company has outlined additional U.S. plant closures and the cessation of preprint operations at its Richwood, Kentucky facility, along with closures in Aurora, Illinois and converting plants in Elk Grove, California and Barrington, New Jersey by the end of Q3 2026. Management plans to transition customers to other sites within each region. Source: key developments.

- International Paper temporarily suspended operations at its Pine Hill, Alabama mill after weather related roof damage and currently expects to resume manufacturing in August 2026, while working with customers to manage any impact. Source: key developments.

Valuation Changes for International Paper

- Fair Value has risen from $39.36 to $43.64. This represents an increase of about 10.8% in the updated estimate for International Paper.

- Discount Rate has moved slightly lower from 7.39% to 7.30%. This reflects a modest adjustment in the required return used in the valuation work.

- Revenue Growth has shifted from 2.49% to 2.83%. The new assumption is modestly higher than before in the model for International Paper.

- Net Profit Margin has edged up from 6.60% to 6.63%. The margin change in the updated assumptions is small but positive.

- Future P/E has increased from 15.1x to 16.4x. The valuation framework now applies a slightly higher earnings multiple to International Paper.

Key Takeaways

- Rising sustainability trends and e-commerce growth are strengthening demand for fiber-based packaging, supporting both revenue growth and pricing power.

- Operational improvements, strategic divestitures, and emerging market expansion are boosting margins, competitiveness, and overall earnings quality.

- Ongoing operational, market, and integration challenges threaten margin improvement, revenue growth, and achievement of long-term financial targets amid industry and macroeconomic headwinds.

Catalysts

About International Paper- Produces and sells renewable fiber-based packaging and pulp products in North America, Latin America, Europe, and North Africa.

- International Paper is benefiting from a long-term shift away from plastic and toward fiber-based, recyclable packaging, as rising sustainability and circular economy priorities among consumers and regulators are boosting demand for its core product lines. This is expected to drive higher revenue and potentially support premium pricing.

- The acceleration of global e-commerce continues to support steady and growing demand for corrugated packaging, giving International Paper a long-term volume growth tailwind and improving top line stability, even amid economic volatility.

- The company's substantial capital investments in automation, advanced manufacturing, and mill reliability-funded by targeted asset divestitures and plant closures-are expected to reduce operating costs and materially expand net margins over the next several years.

- Strategic focus on commercial excellence-including the 80/20 model and improved customer service-is resulting in market share gains in North America and Europe, which should help close the revenue gap with industry peers and lift future earnings.

- Portfolio optimization, including exiting noncore and lower-margin businesses and expanding more heavily into emerging markets with rising packaging consumption, is projected to enhance International Paper's revenue quality and drive higher returns on invested capital over time.

International Paper Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

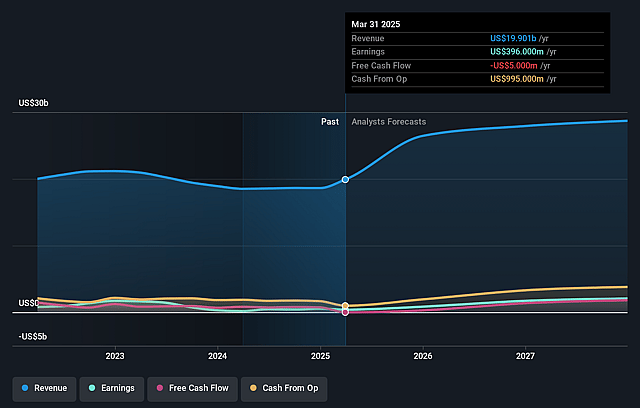

- Analysts are assuming International Paper's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from -10.8% today to 6.6% in 3 years time.

- Analysts expect earnings to reach $1.8 billion (and earnings per share of $3.33) by about July 2029, up from -$2.6 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.4x on those 2029 earnings, up from -8.9x today. This future PE is lower than the current PE for the US Packaging industry at 21.3x.

- Analysts expect the number of shares outstanding to grow by 0.29% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.3%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Chronic mill reliability issues stemming from years of underinvestment continue to impact operational efficiency and have left $150 million in profit on the table year-to-date, with no guarantee of rapid resolution; this threatens both net margins and future earnings.

- Macroeconomic uncertainty and persistent market softness in both North America and especially EMEA, including ongoing tariff negotiations and geopolitical tensions, are suppressing overall industry demand and could limit revenue growth and earnings stability.

- European market remains structurally oversupplied and subject to pricing volatility, with management acknowledging risks that recent price increases may not be sustainable-potentially undermining revenue and EMEA segment EBITDA through 2026 and beyond.

- The company is in the early stages of executing complex asset optimization, cost-outs, and plant closures (especially in EMEA), which pose risk of execution delays and integration challenges; these may elevate restructuring costs and limit the intended improvements to margins and ROIC in the medium term.

- Reliance on cost-out actions and commercial transformation to achieve ambitious $6 billion EBITDA and $1.1 billion commercial excellence targets by 2027, while still carrying significant maintenance obligations, integration risk from the DS Smith acquisition, and pressure from secularly slow growth in key end-markets, increases the probability of missing long-term earnings and free cash flow objectives.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $43.64 for International Paper based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $61.0, and the most bearish reporting a price target of just $39.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $26.5 billion, earnings will come to $1.8 billion, and it would be trading on a PE ratio of 16.4x, assuming you use a discount rate of 7.3%.

- Given the current share price of $44.09, the analyst price target of $43.64 is 1.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on International Paper?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.