Last Update 23 Jun 26

Fair value Increased 11%CNK: Box Office Momentum And Margin Assumptions Will Support Future Returns

The analyst price target for Cinemark Holdings has been raised by about $3.40, with analysts attributing the change to a lower required discount rate, slightly higher profit margin assumptions, and supportive recent research that cites stronger Q1 results and improving Q2 box office trends as key factors.

Analyst Commentary

Recent Street research on Cinemark Holdings points to a cluster of higher price targets, with analysts updating their models after Q1 results and early reads on Q2 box office performance. The commentary gives investors a clearer view of how the market is weighing near term execution against current valuation.

Bullish Takeaways

- Bullish analysts point to Q1 results that exceeded prior expectations as support for raising price targets, suggesting Cinemark’s recent execution and margin profile are tracking ahead of earlier assumptions.

- Several reports highlight improving Q2 trends, including May domestic box office performance, as a reason to adjust revenue and profit expectations upward in the near term.

- Some bullish analysts cite factors such as continued box office strength, windowing progress, and guild renewal tailwinds as potential supports for Cinemark’s earnings power if these drivers hold.

- Reiterations of positive designations, such as top idea status, signal that certain analysts view Cinemark stock as relatively attractive versus peers on risk and reward, based on their updated assumptions.

Bearish Takeaways

- More cautious analysts acknowledge improved fundamentals but argue that much of the optimistic scenario may already be reflected in Cinemark’s current valuation, which they see as limiting upside from here.

- Neutral ratings alongside higher targets indicate that some on the Street are less comfortable with the reward to risk profile, even as they build stronger near term assumptions into their models.

- There is an emphasis on being more selective going forward, with concerns that future gains could depend heavily on continued box office strength and industry tailwinds that are difficult to underwrite with high conviction.

- The mix of Buy and Neutral stances underscores that while execution and Q2 momentum support higher targets, not all analysts are prepared to take a more aggressive view on Cinemark’s growth runway or valuation support at recent levels.

What’s in the News for Cinemark Holdings

- Cinemark Holdings reported its all-time biggest three-day domestic box office opening weekend for a G or PG rated film with Toy Story 5, according to company announcements.

- The Toy Story 5 opening contributed to Cinemark achieving its best-ever domestic June weekend box office and the top-performing domestic box office weekend of 2026, based on the same company update.

- Management highlighted strong demand for Toy Story 5 themed merchandise, which supported higher consumer spending tied to the film’s release, per the company’s announcement.

- Cinemark also reported its highest June weekend domestic food and beverage per capita in company history, helped by an elevated food and beverage menu linked to the Toy Story 5 opening, according to the same source.

Valuation Changes for Cinemark Holdings

- Fair Value, updated to $35.18 from $31.82, has risen modestly based on the latest assumptions.

- Discount Rate, reduced from 12.13% to 10.82%, has fallen slightly, which supports a higher present value for Cinemark Holdings in the updated model.

- Revenue Growth, adjusted from 6.04% to 5.69%, has edged lower, reflecting a slightly more conservative top line outlook in the forecast period.

- Profit Margin, revised from 7.99% to 8.18%, has risen marginally, indicating a small uplift in expected profitability for Cinemark Holdings.

- Future P/E, moved from 17.39x to 18.65x, has increased, implying a somewhat higher valuation multiple being applied in the updated analysis.

Key Takeaways

- Growing demand for premium cinematic experiences, robust film releases, and loyalty programs supports rising revenue, attendance, and resilient box office performance.

- Operational efficiency, market share gains, and targeted customer engagement initiatives drive margin improvement and position Cinemark for long-term profitability.

- Cinemark's profitability and growth are threatened by volatile film release cycles, high fixed costs, inflation, and the ongoing shift to streaming and at-home entertainment.

Catalysts

About Cinemark Holdings- Engages in the motion picture exhibition business.

- Accelerating consumer demand for out-of-home experiences, as seen by surging attendance and record-breaking box office results, alongside a robust release pipeline of blockbuster films through 2025 and 2026, positions Cinemark for ongoing revenue growth and solidifies expectations for higher and more resilient box office receipts over time.

- Expansion of premium cinematic offerings-such as PLF formats (XD, D-BOX, ScreenX), recliner seating, and enhanced concession merchandising-enables Cinemark to drive higher average ticket prices and increase per-visit spend, directly impacting both revenue and net margin improvement in the long run.

- Sustained market share gains in both the U.S. and Latin America, combined with continued population growth in key geographies, set the stage for above-industry attendance growth and favorable operating leverage, positively influencing topline revenue and adjusted EBITDA.

- Company-led initiatives in operational productivity, cost management, and labor flexibility have meaningfully expanded EBITDA and net margins, and ongoing focus in these areas should continue to drive profitability as revenue scales with greater attendance.

- Highly engaged and growing loyalty program membership-Movie Club and Cinemark Rewards-creates recurring, higher-value customer relationships that increase visit frequency and F&B attachment rates, helping diversify revenue streams and improve earnings predictability.

Cinemark Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

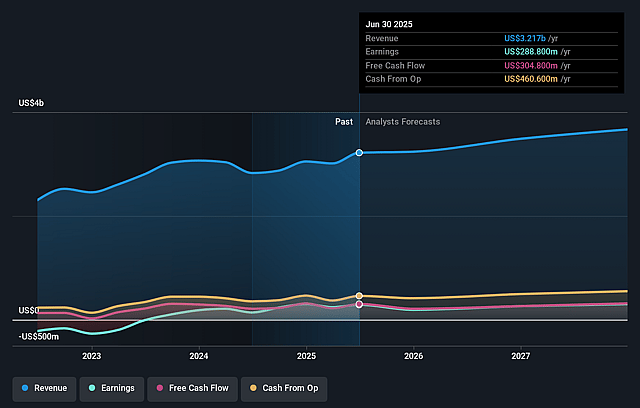

- Analysts are assuming Cinemark Holdings's revenue will grow by 5.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.2% today to 8.2% in 3 years time.

- Analysts expect earnings to reach $310.6 million (and earnings per share of $2.89) by about June 2029, up from $168.7 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $367.9 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 18.8x on those 2029 earnings, down from 23.0x today. This future PE is lower than the current PE for the US Entertainment industry at 23.0x.

- Analysts expect the number of shares outstanding to grow by 1.81% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.82%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Cinemark's strong recent revenue and margin gains are largely attributed to a particularly favorable and blockbuster-heavy film slate, but management repeatedly flagged that performance is highly dependent on the cadence and mix of major studio releases and content cycles-making revenues and earnings vulnerable to film pipeline disruptions, studio strategy shifts (e.g., direct-to-streaming), or cyclical box office downturns.

- The company's high fixed cost structure-including long-term leases, elevated facility expenses, and ongoing significant capital outlays for theater modernization-limits flexibility to reduce costs in periods of soft attendance, which could compress net margins and cash flow when box office performance normalizes or declines.

- Ongoing inflationary pressures on concessions, labor, and facility costs, along with a growing share of lower-margin merchandise in concession sales, threaten to erode profitability as cost inflation has only been partially offset by price hikes and product mix shifts, impacting future net margins and EBITDA.

- Management noted that attendance recovery and per-cap growth have been strong due to enhanced amenities and loyalty programs, but secular risks persist from shifting consumer preferences toward at-home digital entertainment and streaming, which may result in a long-term decline in foot traffic and recurring revenues as consumer behavior continues evolving.

- Box office success remains concentrated in a handful of blockbuster tentpoles, with most premium formats (like PLFs) still only representing 15% of the revenue; this reliance on a narrow set of films creates earnings volatility and leaves the company exposed to weak or disappointing film slates, as well as to rising bargaining power from consolidated studios, which can pressure film rental margins and overall profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $35.18 for Cinemark Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $23.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.8 billion, earnings will come to $310.6 million, and it would be trading on a PE ratio of 18.8x, assuming you use a discount rate of 10.8%.

- Given the current share price of $33.61, the analyst price target of $35.18 is 4.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Cinemark Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.