Key Takeaways

- Focus on premium experiences and enhanced concessions is boosting margins and per-patron earnings, while urban growth supports higher theater revenue.

- Expansion of loyalty programs and strong box office trends are driving customer retention and supporting stable, recurring revenue growth.

- Shifting consumer habits, high fixed costs, evolving release models, and elevated debt levels threaten Cinemark’s revenue stability, financial flexibility, and long-term profitability.

Catalysts

About Cinemark Holdings- Engages in the motion picture exhibition business.

- Sustained enthusiasm for communal, out-of-home entertainment—especially among younger, experience-driven consumers—is fueling record attendance and strong box office results for family and event films. This is expected to bolster revenue growth and support higher per-theater earnings as the attendance recovery accelerates with an improving film slate.

- Population growth in metropolitan areas continues to drive demand for multiplex locations, positioning Cinemark to capture outsized per-theater revenue and improved utilization, which should contribute to robust revenue and earnings growth as urbanization trends persist.

- Ongoing investment in premium cinema experiences—such as PLF screens, luxury recliners, and immersive audio—is directly supporting strategic pricing actions and driving both record average ticket prices and higher margins, with further upside as more locations are upgraded and the content slate skews towards tentpole films ideal for premium formats.

- Cinemark's differentiated focus on food and beverage innovation, including expanded menus, alcohol, and high-margin merchandising, is leading to all-time high concession revenue per patron and is expected to meaningfully expand net margins as consumer discretionary spending rises and new product categories are launched.

- Strategic expansion of loyalty and subscription programs, such as the Cinemark Movie Club, is increasing customer frequency and retention, driving predictable and recurring revenues. Combined with industry gains from theatrical exclusivity windows and an expanding pipeline of diverse content, this should result in margin expansion and stronger, more stable earnings growth over the next several years.

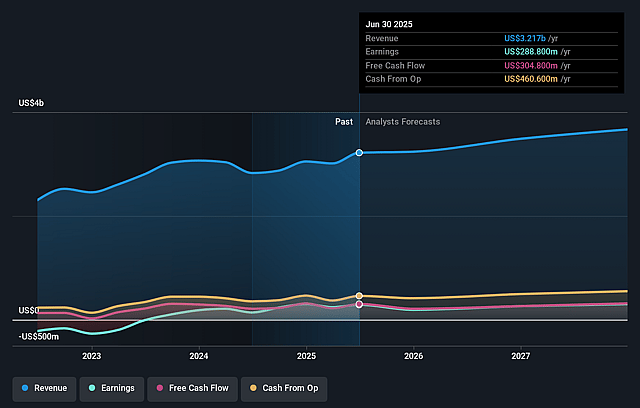

Cinemark Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Cinemark Holdings compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Cinemark Holdings's revenue will grow by 10.6% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 8.0% today to 8.8% in 3 years time.

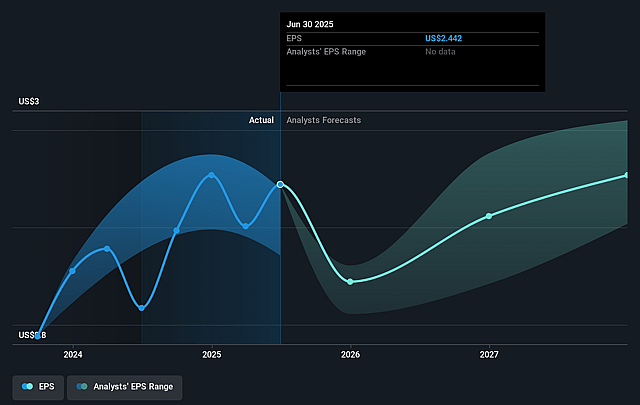

- The bullish analysts expect earnings to reach $359.2 million (and earnings per share of $3.13) by about July 2028, up from $241.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 13.6x on those 2028 earnings, down from 14.1x today. This future PE is lower than the current PE for the US Entertainment industry at 26.9x.

- Analysts expect the number of shares outstanding to decline by 5.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.6%, as per the Simply Wall St company report.

Cinemark Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing secular shift toward at-home consumption of entertainment content, driven by improved streaming platforms and home theater technology, continues to reduce theatrical attendance, which directly pressures revenue and net income for Cinemark Holdings over the long term.

- Demographic changes, with younger audiences increasingly favoring interactive and on-demand digital experiences over traditional cinema-going, may gradually shrink Cinemark’s core customer base and negatively affect future box office and concession revenue streams.

- The company’s high fixed operating costs, including lease obligations and maintenance for an extensive physical footprint, limit its ability to reduce expenses in the event of continued or worsening attendance declines, potentially resulting in margin compression and less predictable earnings.

- An ongoing compression in theatrical release windows and the risk of increased day-and-date streaming releases continue to threaten the traditional exhibitor revenue model, which could erode revenue stability and increase volatility in Cinemark’s financial results over time.

- Elevated debt levels relative to peers may restrict financial flexibility at Cinemark, particularly as it gears up for significant debt repayments and ongoing capital expenditures, potentially hampering net income growth and reducing the company’s capacity to invest in modernization amidst industry headwinds.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Cinemark Holdings is $37.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Cinemark Holdings's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $37.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $4.1 billion, earnings will come to $359.2 million, and it would be trading on a PE ratio of 13.6x, assuming you use a discount rate of 11.6%.

- Given the current share price of $30.07, the bullish analyst price target of $37.0 is 18.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Cinemark Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.