Last Update 02 Aug 26

Fair value Decreased 2.78%AGCO: North American Share Gains And Tariff Relief Will Support Recovery

AGCO's updated fair value estimate has moved from $128.57 to $125.00 as analysts factor in lower Street price targets alongside mixed views on near term agricultural markets and potential benefits from market share gains and tariff relief in the longer term.

Analyst Commentary

Recent Street research on AGCO points to a split view on the stock, with some analysts focusing on long term recovery potential and others highlighting current agricultural market headwinds and valuation constraints. For you as an investor, the key themes are how AGCO executes through softer ag conditions and how much of a future recovery is already reflected in price targets.

Bullish Takeaways

- Bullish analysts see room for AGCO to benefit if U.S. agricultural trends improve, with several reports referencing the company as well positioned for a market recovery in North America.

- Some research points to AGCO gaining share in North America, which could support earnings power if volumes stabilize or improve and help underpin the long term valuation case.

- Multiple Buy ratings and price targets above the updated fair value estimate suggest that some analysts see upside if AGCO executes on its earnings potential and longer term volume outlook.

- Citi highlights lower U.S. tariffs on agricultural equipment as an incremental positive for AGCO, with the potential to add earnings per share and support margins if the benefit flows through to the bottom line.

Bearish Takeaways

- Several bearish analysts maintain Underweight or cautious views, with price targets around US$110 that sit below the updated fair value estimate. This signals concern about downside risk if conditions stay soft.

- Research notes describe agricultural markets as challenged, particularly into and around the Q2 reporting window. This raises questions on AGCO's near term volume and pricing power.

- Price target cuts from different firms, including JPMorgan, indicate lower expectations for the sector and for AGCO's earnings setup versus earlier in the year, even where ratings remain positive.

- Some analysts flag that the more constructive views on AGCO rely on a future inflection in agricultural demand rather than current fundamentals. This can limit near term support for the stock if that inflection is delayed or weaker than hoped.

What’s in the News for AGCO

- AGCO issued 2026 earnings guidance that targets net sales of US$10.1b to US$10.2b and earnings per share of US$5.50 to US$5.75, with plans to align production with dealer demand and continue cost controls and pricing support. (Source: Company guidance)

- The Board approved amendments to AGCO's bylaws on July 8, 2026 that allow one or more stockholders holding at least 25% of voting power to call a special meeting, subject to specified notice and information requirements. (Source: Company bylaw amendments)

- AGCO highlighted fuel saving technologies across its Fendt, Massey Ferguson and Valtra brands, with independent DLG PowerMix testing cited for tractor platforms using AGCO Power engines and integrated powertrain solutions aimed at lower fuel use and stable performance. (Source: Product announcement)

- Management stated that AGCO is actively looking for acquisitions and reiterated a capital allocation approach that focuses on reinvestment, an investment grade balance sheet, targeted deals to support technology adoption and returning capital to shareholders. (Source: AGCO 2026 Q1 earnings call)

- Between January 1 and March 31, 2026, AGCO repurchased 333,755 shares for US$35.8 million, completing a total of 2,330,959 shares repurchased for US$250 million under the buyback first announced on July 9, 2025. (Source: Buyback update)

Valuation Changes for AGCO

- Fair value has moved slightly lower, from $128.57 to $125.00.

- The discount rate has risen slightly, from 8.92% to 9.14%.

- The revenue growth assumption has increased, from 5.21% to 5.96%.

- The net profit margin assumption is marginally lower, from 7.20% to 7.15%.

- The future P/E multiple has declined, from 13.0x to 11.3x.

Key Takeaways

- Investments in premium brands, precision agriculture, and digital solutions position AGCO for stronger growth, higher margins, and enhanced earnings quality.

- Structural improvements and aftermarket expansion support operational efficiency, stable earnings, and robust capital returns to shareholders.

- Prolonged weak demand, higher costs from tariffs, and elevated inventories threaten AGCO's profitability and undermine both market share gains and long-term margin targets.

Catalysts

About AGCO- Manufactures and distributes agricultural equipment and replacement parts worldwide.

- The global push for higher agricultural productivity due to population growth and rising food demand continues to drive AGCO's investments in premium brands (like Fendt) and expansion into underserved regions, positioning the company to outgrow industry demand and materially lift long-term revenue growth.

- Accelerating adoption of precision agriculture and digital solutions is expected to significantly increase demand for AGCO's retrofit technologies (e.g., Precision Planting and PTx), supporting the shift toward higher-margin software-driven revenue, which should enhance future margins and earnings quality.

- Recent structural improvements-including reduced fixed costs, lower dealer inventories, and dealer-focused initiatives like FarmerCore-are expected to deliver improved operational leverage and working capital efficiency, setting a foundation for higher free cash flow and increased net margins as demand recovers.

- AGCO's global parts and aftermarket expansion leverages both e-commerce and service innovation, capitalizing on the aging installed base and growing focus on recurring, high-margin revenues; this strategy is likely to drive more stable and resilient long-term earnings and margin expansion across cycles.

- With the resolution of the TAFE partnership, AGCO has greater capital allocation flexibility, enabling a $1 billion share buyback program; this buyback, combined with expected mid-cycle margin improvement targets, should accelerate EPS growth and return capital to shareholders.

AGCO Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming AGCO's revenue will grow by 6.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.2% today to 7.1% in 3 years time.

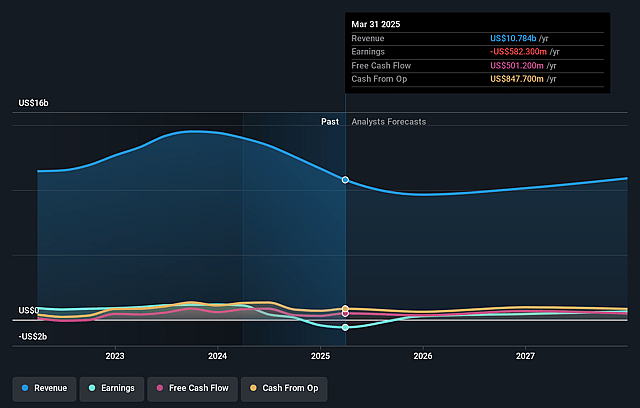

- Analysts expect earnings to reach $879.9 million (and earnings per share of $12.2) by about August 2029, up from $533.4 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.0 billion in earnings, and the most bearish expecting $658.4 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 11.4x on those 2029 earnings, down from 13.4x today. This future PE is lower than the current PE for the US Machinery industry at 27.0x.

- Analysts expect the number of shares outstanding to decline by 4.72% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.14%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Prolonged weak demand in North America and Western Europe, driven by cautious farmer sentiment, persistently high input costs, lower export demand, and ongoing policy uncertainty, risks suppressing AGCO's revenues and operating margins in its core markets over the long term.

- Tariffs and global trade conflicts-especially newly announced EU tariffs and continuing U.S. policy uncertainty-could further compress AGCO's margins by increasing costs and forcing delayed or diluted pricing actions, directly impacting net earnings and profitability.

- Elevated dealer inventories in North America and ongoing underproduction (down over 50% in Q3 and Q4) suggest a risk of continued negative operating margins in that region, which may weigh on consolidated company earnings if the inventory overhang and demand weakness persist longer than expected.

- AGCO's market share gains, particularly for premium brands like Fendt, could be undermined by increased costs relative to competitive products if tariffs lead to higher relative prices or if production footprint changes are not implemented in time, creating risk to both future revenue growth and margin expansion plans.

- Structural industry headwinds such as four consecutive years of industry decline in Europe, growing factory under-absorption costs during downturns, and potential for further cost inefficiencies from supply chain or production mismatches threaten AGCO's ability to achieve mid-cycle margin targets and sustainable cash flow growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $125.0 for AGCO based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $160.0, and the most bearish reporting a price target of just $105.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $12.3 billion, earnings will come to $879.9 million, and it would be trading on a PE ratio of 11.4x, assuming you use a discount rate of 9.1%.

- Given the current share price of $102.16, the analyst price target of $125.0 is 18.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AGCO?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.