Key Takeaways

- Shrinking demand for large-scale agricultural equipment and technological lag threaten AGCO’s long-term growth and competitive position.

- Trade tensions, supply chain disruptions, and industry overcapacity are set to compress margins and weaken AGCO’s profitability.

- Strong positioning in precision agriculture, emerging markets, and high-margin products, supported by cost efficiencies, underpins robust long-term growth and rising profitability.

Catalysts

About AGCO- Manufactures and distributes agricultural equipment and replacement parts worldwide.

- A declining global population growth rate and the aging of the farming workforce are projected to shrink the demand for agricultural equipment over time, posing a structural headwind to AGCO’s core business and threatening sustained revenue growth.

- Rapid intensification of trade barriers, tariff escalations between the US, EU, and China, and increasing geopolitical friction have already pressured AGCO's cross-border sales and are expected to further raise supply chain costs, eroding net margins and depressing profitability.

- The accelerating shift towards sustainable and alternative farming practices—including regenerative agriculture and indoor farming—which demand less large-scale machinery, is expected to diminish the long-term addressable market for AGCO, resulting in chronic weakness in equipment sales and limiting future revenue expansion.

- AGCO’s failure to consistently outpace peers in the adoption of next-generation digital and precision technologies risks permanent market share loss, especially as more technologically advanced and capitalized competitors squeeze pricing, triggering margin compression and reducing return on invested capital.

- Persistent industry overcapacity, lengthening replacement cycles due to rising machinery durability, and volatile commodity prices are expected to create inventory gluts, trigger discounting across the industry, and drive ongoing downward pressure on AGCO’s sales volumes and earnings for the foreseeable future.

AGCO Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on AGCO compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming AGCO's revenue will decrease by 0.8% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -5.4% today to 6.0% in 3 years time.

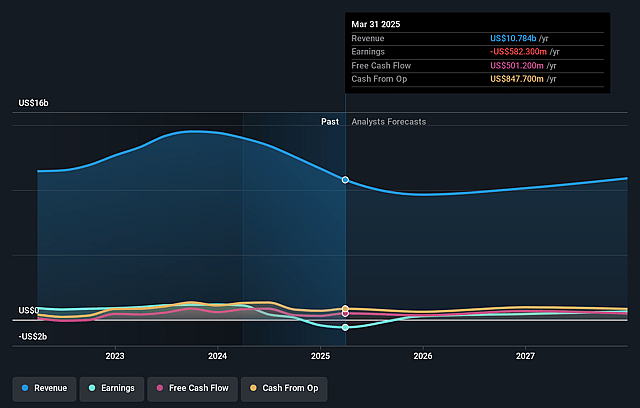

- The bearish analysts expect earnings to reach $632.6 million (and earnings per share of $8.68) by about July 2028, up from $-582.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 12.5x on those 2028 earnings, up from -14.4x today. This future PE is lower than the current PE for the US Machinery industry at 22.9x.

- Analysts expect the number of shares outstanding to decline by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.38%, as per the Simply Wall St company report.

AGCO Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The accelerating adoption of precision agriculture and smart farming technologies places AGCO in a strong position to capture growth, evidenced by rapid integration of PTx Trimble solutions, a robust cross-selling channel, and award-winning innovation, all of which are expected to drive higher revenue per unit and expanded net margins over the long term.

- Expansion in emerging markets like Brazil, which is showing early signs of demand recovery and is described as a critical growth market, positions AGCO to benefit from global agricultural expansion and higher mechanization, supporting both top-line growth and future earnings.

- The company's structural cost reduction and operational efficiency initiatives, already ahead of schedule in delivering savings, have improved profitability at the trough of the industry cycle and are expected to result in meaningfully higher incremental margins, bolstering net earnings as sales recover.

- AGCO’s product portfolio shift towards high-margin businesses—such as Fendt, global parts, and Precision Ag—is expected to raise mid-cycle operating margins toward the long-term target of 14% to 15% by 2029, which supports rising earnings potential even through soft market conditions.

- Continued global demand growth due to demographic trends (population growth, rising protein consumption, and middle-class expansion), together with the push for greater farm productivity and sustainability, creates a long-term tailwind for AGCO’s equipment and technology offerings, supporting sustained revenue and profit growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for AGCO is $84.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of AGCO's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $140.0, and the most bearish reporting a price target of just $84.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $10.5 billion, earnings will come to $632.6 million, and it would be trading on a PE ratio of 12.5x, assuming you use a discount rate of 8.4%.

- Given the current share price of $112.12, the bearish analyst price target of $84.0 is 33.5% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AGCO?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.