Last Update 08 Apr 26

GHI: Reset Price Cut And Cash Distributions Will Support Future Income

Analysts trimmed their price target on Greystone Housing Impact Investors by $7.00 to $7.00, citing updated views on fair value, discount rate, expected revenue growth of 69.47% and a profit margin of 24.82%, as reflected in recent research including a downgrade at Citizens.

Analyst Commentary

Recent research on Greystone Housing Impact Investors highlights mixed views, with the latest downgrade framed around how current expectations line up with the updated fair value estimate and risk profile.

Bullish Takeaways

- Bullish analysts point to the projected 69.47% revenue growth as support for the current business plan, arguing that this level of top line expansion can justify the revised fair value when execution is on track.

- The profit margin of 24.82% is viewed as a sign that the existing portfolio can still produce solid earnings relative to revenue, which some see as a cushion for any short term volatility in the housing and financing markets.

- Supporters highlight that, even with a trimmed price target, the updated fair value framework still reflects confidence that the company can convert its revenue base into consistent cash flows over time.

- Some bullish analysts argue that a reset price target can reduce the risk of disappointment for new investors, making future execution milestones easier to meet or exceed against more measured expectations.

Bearish Takeaways

- Bearish analysts focus on the size of the cut to the price target to US$7.00, viewing it as a sign that earlier assumptions about growth, risk, or valuation were too optimistic relative to the company’s current outlook.

- There is concern that the discount rate applied in the updated work suggests a higher perceived risk profile, which can weigh on valuation even when revenue growth and profit margins look strong on paper.

- Some cautious views emphasize that a 69.47% revenue growth expectation sets a high execution bar, and any shortfall against that figure could pressure both earnings and investor confidence.

- Bearish analysts also question the sustainability of a 24.82% profit margin if funding costs, credit conditions, or project level economics become less favorable, which would challenge the current fair value assumptions.

What's in the News

- On March 18, 2026, Greystone Housing Impact Investors LP announced that its Board of Managers declared a cash distribution of US$0.14 per Beneficial Unit Certificate to BUC holders. (Key Developments)

- The cash distribution is scheduled to be paid on April 30, 2026 to all BUC holders of record as of the close of trading on March 31, 2026. (Key Developments)

- BUCs will trade ex distribution as of March 31, 2026, which is the date used to determine which holders qualify for the US$0.14 payment. (Key Developments)

Valuation Changes

- Fair Value: Restated at $7.00, keeping the target level effectively unchanged in the latest update.

- Discount Rate: Held steady at 12.33%, indicating no revision to the assumed risk level used in the valuation work.

- Revenue Growth: Kept at 69.47%, with only a rounding level adjustment in the underlying model inputs.

- Net Profit Margin: Maintained at 24.82%, again with only minimal, non directional rounding changes.

- Future P/E: Left at 7.17x, reflecting stable expectations for the valuation multiple applied to projected earnings.

Key Takeaways

- Strong demand for affordable and multifamily housing, along with expanded capital commitments, supports revenue growth and a robust investment pipeline.

- Diversified portfolio and operational efficiencies reduce risk and enhance earnings stability, with federal support ensuring a favorable funding environment.

- Ongoing market pressures, credit risks, and reliance on government incentives threaten Greystone's revenue stability, asset values, and long-term profitability.

Catalysts

About Greystone Housing Impact Investors- Acquires, holds, sells, and deals mortgage revenue bonds that are issued to provide construction and permanent financing for multifamily, student, and senior citizen housing, skilled nursing properties, and commercial properties in the United States.

- The company is benefiting from a persistent shortage of affordable and workforce housing in the U.S., combined with strong demand for multifamily and senior housing; this supports a robust investment pipeline and suggests revenue growth opportunities as Greystone continues to fund new projects and fill market gaps left by retreating banks.

- Recently announced additional capital commitments to the BlackRock construction lending joint venture and a new institutional investor significantly increase Greystone's firepower to finance new low-income housing projects, directly supporting expansion of its income-producing asset base and expected to drive higher future revenues and earnings.

- Federal support for core affordable housing programs remains intact, with Congress showing willingness to fully fund HUD initiatives and technical improvements in the Low-Income Housing Tax Credit (LIHTC) program, ensuring continued access to subsidies and low-risk lending environments that uphold returns on investment and underpin resilient net margins.

- Portfolio diversification, evidenced by Greystone's active development and leasing in both market-rate and senior housing, in addition to affordable housing, reduces market and asset-type risk-supporting earnings stability and protecting net margins from sector-specific downturns.

- Advances in operational efficiency, including the expansion of proprietary asset management and servicing platforms, along with amendments to credit facilities that extend maturities and increase borrowing capacity, enhance operational flexibility and scalability-improving long-term margins and supporting future earnings growth.

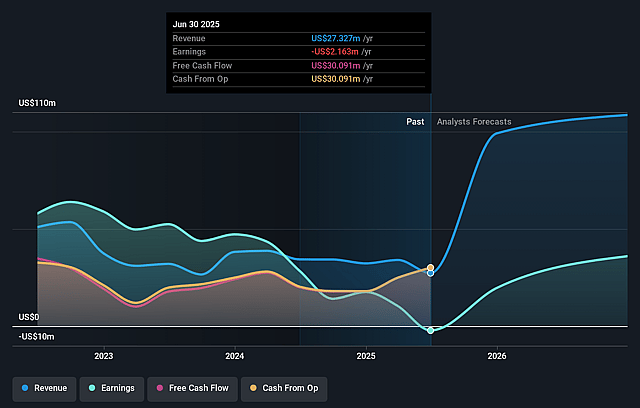

Greystone Housing Impact Investors Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Greystone Housing Impact Investors's revenue will grow by 69.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -47.8% today to 24.8% in 3 years time.

- Analysts expect earnings to reach $30.4 million (and earnings per share of $1.3) by about April 2029, up from -$12.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 7.5x on those 2029 earnings, up from -9.6x today. This future PE is lower than the current PE for the US Diversified Financial industry at 16.0x.

- Analysts expect the number of shares outstanding to decline by 0.56% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.33%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Elevated levels of new municipal bond issuance, combined with only moderate fund inflows, are pressuring yields and returns in the municipal bond market, which could further suppress Greystone's investment yields and negatively impact net interest income and overall revenue.

- Provisions for credit losses-particularly linked to underperforming affordable housing properties in certain markets (like South Carolina)-signal ongoing credit quality and collateral value risks that could result in further losses, pressuring net margins and reducing earnings reliability.

- Persistent underperformance of the U.S. municipal bond market, coupled with high-profile credit issues in the high-yield space, creates an uncertain investment climate and puts downward pressure on valuations, impairing asset values and potentially leading to additional unrealized losses and lower book value per share.

- Continued exposure and reliance on government programs, tax credits, and low-income housing incentives exposes Greystone to the risk of policy shifts or funding cuts, which could depress future investment pipelines and reduce revenue opportunities over the long term.

- The necessity to advance additional capital (e.g., for property taxes or operational shortfalls) into joint ventures and delayed project exits can tie up liquidity and reduce the return on invested capital, leading to higher operating costs and potential net margin compression.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $7.0 for Greystone Housing Impact Investors based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $122.6 million, earnings will come to $30.4 million, and it would be trading on a PE ratio of 7.5x, assuming you use a discount rate of 12.3%.

- Given the current share price of $4.97, the analyst price target of $7.0 is 29.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Greystone Housing Impact Investors?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.