Last Update 05 Jun 26

ONDS: Federal Drone Support And Defense Backlog Will Drive Future Upside

Analysts have lifted their price target on Ondas by $6, citing sector interest related to U.S. federal support for domestic drone companies and recent firm-specific research that incorporates updated growth and margin assumptions.

Analyst Commentary

Recent research around Ondas reflects a mix of optimism tied to policy headlines and price target revisions, alongside reminders that execution risks and open questions still matter for valuation.

Bullish Takeaways

- Bullish analysts highlight U.S. federal discussions about potential funding for domestic drone companies as a supportive backdrop for sector sentiment, which has included Ondas alongside several peers.

- Recent price target increases, including a US$6 lift cited earlier and an additional US$2 move from another firm, signal that some analysts are revisiting their models and are willing to assign higher value to Ondas based on updated assumptions.

- Sector interest, helped by policy headlines around federal support, is seen by bullish analysts as a potential driver of stronger investor attention to Ondas, which can influence how the stock trades relative to peers.

- Research notes referencing firm specific work on growth and margin assumptions suggest that bullish analysts see room for Ondas to improve profitability metrics over time, which feeds into higher projected valuation ranges.

Bearish Takeaways

- Some research flags that there are still several unknowns ahead for Ondas, even in the context of a strong Q4, which can limit conviction around how consistently the company can execute against expectations.

- Cautious analysts point out that policy discussions around federal funding are still only talks, not firm commitments, so reliance on potential support can introduce headline risk if outcomes differ from early reports.

- The presence of multiple publicly traded drone stocks reacting to the same policy story means competition for capital and execution success across the group, which can affect how much premium investors are willing to assign to Ondas specifically.

- Where models depend heavily on updated growth and margin assumptions, bearish analysts see risk that any shortfall versus those assumptions could pressure both earnings expectations and valuation multiples.

What's in the News

- Ondas reported Q1 2026 revenue of US$50.1 million, with very large year over year growth driven by demand for autonomous drone systems, counter drone technologies, and defense products, alongside key U.S. Department of Defense and Department of Homeland Security contracts. Source: Q1 2026 earnings coverage

- The company raised its full year 2026 revenue guidance to at least US$390 million and reported a pro forma backlog of about US$457 million, supported by orders that took Q2 to date intake beyond US$110 million and an active opportunity pipeline of about US$4.3 billion. Source: Q1 2026 earnings coverage and May 2026 order update

- Ondas completed a US$196.6 million acquisition of Omnisys, an AI defense software developer, and plans to use its Battle Resource Optimization platform as a core software layer across Ondas autonomous systems. The company expects this to contribute more than US$100 million in revenue across 2026 and 2027. Source: Omnisys acquisition announcement

- Management outlined a path to adjusted EBITDA profitability at the product level already in place and moved the adjusted EBITDA profitability target for the Ondas Autonomous Systems segment to Q1 2027. This target is supported by integration of acquisitions such as Mistral, World View Enterprises, and Omnisys. Source: Q1 2026 earnings coverage and Omnisys acquisition announcement

- Ondas entered a partnership with Palantir Technologies to combine AI driven autonomy and data analytics with Ondas multi domain unmanned systems and World View high altitude platforms, aiming to support intelligence, surveillance, and reconnaissance missions across aerial and ground systems. Source: Palantir partnership announcement

Valuation Changes

- Fair Value: Model fair value per share is unchanged at $20.13, indicating no revision to the central valuation estimate.

- Discount Rate: The discount rate has fallen slightly from 8.61% to 8.60%, a small shift that modestly affects the present value of projected cash flows.

- Revenue Growth: Revenue growth assumptions have been reduced significantly from a very large 167.05% to 119.32%. This brings the outlook closer to, but still above, typical single digit or double digit growth ranges.

- Net Profit Margin: Assumed net profit margin has risen slightly from 11.17% to 11.22%, pointing to a marginally stronger profitability profile in the model.

- Future P/E: The future P/E multiple is effectively unchanged, edging from 136.72x to 136.83x. The valuation framework continues to rely on a very high earnings multiple.

Key Takeaways

- Strategic partnerships and expanding defense contracts in various sectors are driving significant revenue growth and market diversification for Ondas Holdings.

- Advancements in autonomous systems and private network technologies are set to enhance operational efficiency, potentially improving margins and financial performance.

- High operating expenses and debt reliance are challenges, with conservative revenue expectations and volatile margins posing risks to future profitability and growth.

Catalysts

About Ondas Holdings- Provides private wireless, drone, and automated data solutions in the United States and internationally.

- Ondas anticipates record revenue growth in 2025, primarily driven by Ondas Autonomous Systems (OAS), due to significant backlog and expanding programs with Optimus and Iron Drone systems in defense and homeland security sectors. This will directly impact revenue.

- The strategic partnership with Palantir Technologies aims to leverage advanced AI capabilities to enhance operational efficiencies and scale OAS’s operations, which is expected to support the revenue ramp and broaden their customer base, influencing earnings and margins through improved operational scale.

- The expansion of OAS’s market presence, with increased customer engagement and government contracts in defense sectors in Israel and the UAE, is set to secure additional military customers, suggesting potential revenue growth and improved market diversification.

- Expected improvements in operating leverage as revenues grow, particularly at OAS, are set to recover gross margins, which could reach 50% or better in the second half of 2025, impacting net margins positively.

- Continued strategic value building at Ondas Networks and progress in private wireless network technologies for rail operations, which includes 900-megahertz network rollouts and new product opportunities, aims to unlock further revenue streams and bolster financial performance.

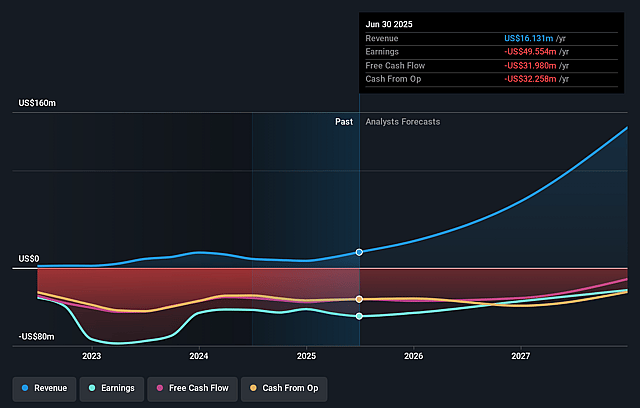

Ondas Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Ondas's revenue will grow by 119.3% annually over the next 3 years.

- Analysts are not forecasting that Ondas will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Ondas's profit margin will increase from 138.9% to the average US Communications industry of 11.2% in 3 years.

- If Ondas's profit margin were to converge on the industry average, you could expect earnings to reach $114.4 million (and earnings per share of $0.19) by about June 2029, down from $134.2 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 136.9x on those 2029 earnings, up from 44.2x today. This future PE is greater than the current PE for the US Communications industry at 32.6x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.6%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ondas Holdings faced challenges in 2024, such as extending timelines at Ondas Networks and disruptions due to military activity in Israel, which could impede future revenue growth if similar issues recur.

- The company's revenue expectations for 2025 remain conservative at $25 million, with uncertainties related to Ondas Networks affecting the potential for revenue expansion.

- Gross margins are expected to be volatile due to the early stages of platform adoption and shifts in revenue mix, which may impact net margins and profitability.

- As of 2024, Ondas Holdings reported high operating expenses and adjusted EBITDA loss, with existing revenues not covering these expenses, posing a risk to future earnings if revenue growth does not accelerate as projected.

- The $52 million in debt outstanding and reliance on raising additional funds or extending debt terms might impact the company's financial health and its ability to invest in growth initiatives.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $20.12 for Ondas based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.0 billion, earnings will come to $114.4 million, and it would be trading on a PE ratio of 136.9x, assuming you use a discount rate of 8.6%.

- Given the current share price of $11.97, the analyst price target of $20.12 is 40.5% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Ondas?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.