Last Update 27 Jul 26

Fair value Increased 27%CDNA: Final Medicare Coverage For Transplant Testing Will Shape Balanced 2026 Repricing

Analysts have raised their fair value view on CareDx stock from $27.80 to $35.40, citing higher price targets linked to what they describe as favorable final Medicare local coverage decisions for the company’s transplant testing portfolio.

Analyst Commentary

Recent analyst commentary on CareDx centers on the final Medicare local coverage decisions for solid organ transplant molecular testing and what those decisions could mean for the stock’s valuation and future execution. Price targets have been adjusted higher, but views on risk and upside are not uniform across the Street.

Bullish Takeaways

- Bullish analysts point to the final Medicare coverage decisions as more favorable than earlier draft proposals, which they see as supportive for the economic case around CareDx transplant tests.

- Some price targets on CareDx have been reset materially higher, with one moving to US$45 from US$28. This reflects a view that the updated coverage terms could justify a higher valuation range.

- Coverage across kidney, heart, and lung surveillance testing, with limits described as generous, is viewed by bullish analysts as expanding the potential testing opportunity relative to where CareDx is operating today.

- The view that previous expectations were too conservative is leading some bullish analysts to argue that financial estimates may need to be revised upward, which they see as a support for the recent re-rating in the stock.

Bearish Takeaways

- More cautious analysts, even while raising price targets, are maintaining less aggressive ratings and highlighting that execution against the updated Medicare coverage terms is still an open question.

- There is a view among bearish analysts that, after a sharp move higher in the stock on the coverage news, the risk and reward may be more balanced. This tempers enthusiasm despite the higher targets.

- Some caution that any future changes to reimbursement frameworks, or slower than expected uptake within the covered transplant testing categories, could limit how much of the perceived opportunity CareDx ultimately captures.

- Bearish analysts also flag that higher expectations embedded in new price targets increase the pressure on CareDx management to deliver on growth and margin assumptions implied by the updated Medicare decisions.

What’s in the News for CareDx

- Medicare finalized the Local Coverage Determination for CareDx solid organ transplant molecular tests, confirming reimbursement for AlloSure Kidney, AlloMap, AlloSure Heart, and AlloSure Lung across kidney, heart, and lung surveillance, with specified frequency limits, according to recent coverage decisions and company disclosures.

- The finalized Medicare policy is expected to take effect on August 30, 2026, following a draft LCD first released on July 17, 2025, and a public comment period that included a response from CareDx, according to the company.

- Coverage criteria include up to six AlloSure Kidney surveillance tests in the first year post transplant and up to four tests per year in years two and three, while maintaining coverage for for cause testing when clinically indicated, based on company information.

- For heart and lung transplant patients, Medicare coverage is maintained for AlloMap and AlloSure Heart, including combined use when appropriate, and for AlloSure Lung, with up to 12 surveillance tests in the first year and four tests in years two and three, according to the finalized LCD details.

- The confirmation of Medicare coverage has been linked in news reports to a single session stock move of up to 29% for CareDx, with sources highlighting that the decision supports reimbursement certainty for the transplant testing portfolio while analysts describe an ongoing debate over how much of the news is already reflected in the current share price.

Valuation Changes for CareDx

- Fair Value: Raised from $27.80 to $35.40, a move of roughly 27%, reflecting updated assumptions in analyst models for CareDx.

- Discount Rate: Adjusted slightly lower from 7.17% to 7.13%, indicating only a minimal change in the rate used to discount future cash flows.

- Revenue Growth: Kept effectively unchanged at around 8.31%, with the update moving from 8.31% to 8.31%, suggesting a stable outlook for top line expansion in the model.

- Net Profit Margin: Maintained at roughly 9.51%, with only a very small numerical adjustment from 9.51% to 9.51%, so margin assumptions for CareDx are essentially steady.

- Future P/E: Increased from 32.2x to 41.0x, pointing to a higher valuation multiple being applied to CareDx projected earnings in the updated analysis.

Key Takeaways

- Growing demand for core testing services and expansion into AI-driven diagnostics and digital health are driving recurring, high-margin revenue and supporting improved earnings stability.

- Enhanced payer coverage and operational efficiencies position CareDx for sustained profitability and margin expansion through diversified revenue streams and lower operating costs.

- Shifting reimbursement policies, regulatory uncertainties, and operational risks threaten revenue stability, margins, and the scalability of CareDx's core product-driven business model.

Catalysts

About CareDx- Engages in the discovery, development, and commercialization of diagnostic solutions for transplant patients and caregivers in the United States and internationally.

- The steady double-digit growth in testing volumes, particularly with the expansion of surveillance protocols for kidney, heart, and lung transplants, suggests ongoing market penetration and growing demand for CareDx's core testing services-reflecting the global rise in organ transplants and chronic disease, which is likely to drive future revenue and topline growth.

- The launch of AI-driven diagnostics like AlloSure Plus and integration into electronic health record systems (e.g., EPIC), positions CareDx to benefit from the broader adoption of precision medicine and personalized diagnostics, likely boosting adoption rates, aiding reimbursement, and ultimately supporting net margin improvements.

- Significant progress in payer coverage-including millions of new covered lives, expanded in-network status, and the implementation of a unique CPT code for AlloSure-indicates a catalyst for sustained increases in ASP (average selling price) and recurring revenue streams, which can directly enhance future profitability and margin expansion.

- Expansion of Patient & Digital Solutions and rapid growth in areas such as transplant pharmacy, remote patient monitoring, and digital health software reflects successful diversification of revenue streams tied to healthcare digitization, likely driving high-margin recurring revenues and supporting improved earnings stability.

- Ongoing improvements in operational efficiency-including advancements in revenue cycle management, enhanced claim verification processes, and reduction in claims rejection rates-are expected to further lower operating costs relative to revenue, supporting improved EBITDA, better cash flow, and ultimately, higher net margins.

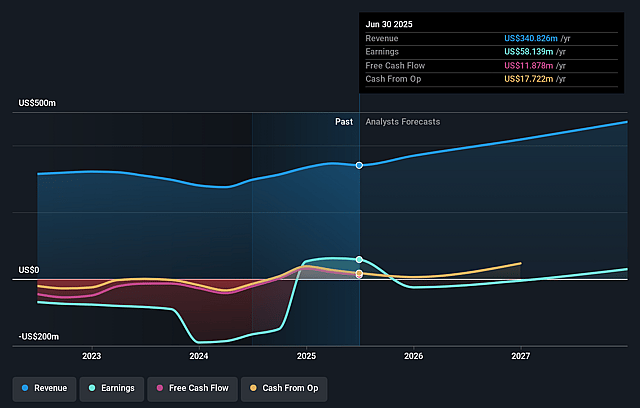

CareDx Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming CareDx's revenue will grow by 8.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -2.0% today to 9.5% in 3 years time.

- Analysts expect earnings to reach $49.9 million (and earnings per share of $0.76) by about July 2029, up from -$8.2 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 41.2x on those 2029 earnings, up from -234.2x today. This future PE is greater than the current PE for the US Biotechs industry at 16.9x.

- Analysts expect the number of shares outstanding to decline by 2.94% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.13%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Introduction of bundled payments and frequency limits for surveillance testing under the new draft LCD policy could potentially result in an annual revenue headwind of $15–30 million, directly impacting revenue growth and net margins if finalized as currently proposed.

- Heavy reliance on AlloSure and HeartCare product lines means that any decrease in reimbursement or test volumes due to regulatory or payer changes could significantly compress earnings and threaten long-term profitability.

- Continued uncertainty and potential downward adjustments in Medicare coverage and reimbursement for molecular diagnostic tests represent an enduring risk, as payers seek to control costs amidst industry-wide shifts toward bundled payments and value-based care, which may shrink the company's addressable market and revenues.

- The transition in CFO leadership and possible operational execution risks (such as delays in EPIC integration and scaling digital health rollouts) may disrupt operational momentum and adversely affect margins, cash flow, or long-term scalability if not effectively managed.

- Increased regulatory scrutiny (e.g., around billing, Medicare compliance, or LCD interpretations) and ongoing exposure to one-time revenue write-offs (such as the $3.8 million adjustment this quarter) indicate potential risks of higher SG&A costs, impacting net margins and forward earnings consistency.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $35.4 for CareDx based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $50.0, and the most bearish reporting a price target of just $21.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $524.6 million, earnings will come to $49.9 million, and it would be trading on a PE ratio of 41.2x, assuming you use a discount rate of 7.1%.

- Given the current share price of $37.14, the analyst price target of $35.4 is 4.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on CareDx?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.