Last Update 13 Jul 26

Fair value Increased 8.82%RATEGAIN: Hotel Connectivity And Payments Expansion Will Support Measured Future Upside

Analysts have revised their fair value estimate for RateGain Travel Technologies from ₹799.56 to ₹870.10. They cite updated assumptions around discount rates, revenue growth, profit margins and future P/E multiples as the basis for the higher price target.

What’s in the News for RateGain Travel Technologies

- Client partnership with Cinko, a last minute hotel booking app by Remwes, LLC, to plug Cinko into RateGain’s Enterprise Connectivity platform, broadening access to global hotel inventory and adding a new same day booking demand channel for hotel partners. (Source: Client Announcements)

- Partnership with Duetto that links RateGain’s AI powered channel manager with Duetto’s Revenue & Profit Operating System, aiming to automate real time rate updates, introduce granular restriction controls, and position RateGain as a Preferred Partner within Duetto’s ecosystem. (Source: Client Announcements)

- Connectivity tie up with ZentrumHub, combining RateGain’s Smart Distribution with ZentrumHub’s infrastructure to simplify hotel distribution, reduce repetitive one to one integrations, and support faster onboarding across the travel ecosystem. (Source: Client Announcements)

- Expansion of RG Pay via collaborations with BoxPay and Easebuzz, integrating payment orchestration, reconciliation, and local Indian payment methods such as UPI, cards, net banking, and wallets, with an aim to improve checkout experience and transaction visibility for travel brands. (Source: Client Announcements)

- Guidance issued for fiscal year 2027, with RateGain Travel Technologies projecting revenue of ₹31,000 million, described as 65% to 70% growth over the current year, alongside a series of board meetings and CFO transition events that outline upcoming financial result approvals and interim finance leadership. (Source: Corporate Guidance, Board Meeting, Executive Changes)

Valuation Changes for RateGain Travel Technologies

- Fair Value: Revised from ₹799.56 to ₹870.10, indicating a higher assessed fair value for RateGain Travel Technologies.

- Discount Rate: Adjusted slightly from 15.26% to 15.16%. This reflects a small change in the required rate of return used in the valuation model.

- Revenue Growth: Kept effectively unchanged at about 27.07%. This suggests the updated valuation uses the same revenue growth outlook as before.

- Net Profit Margin: Maintained at roughly 12.50%, indicating no practical change in assumed profitability levels.

- Future P/E: Raised from 30.88x to 33.52x, pointing to a higher valuation multiple being applied to future earnings.

Key Takeaways

- Accelerated expansion into new geographic and industry verticals, paired with robust subscription revenue, boosts growth visibility and market opportunity.

- Ongoing AI-driven product innovation and integrated analytics strengthen competitive positioning, drive customer retention, and support improved earnings quality.

- Increased reliance on lower-margin, variable revenue streams and exposure to competitive pressures risk constraining long-term growth, profitability, and predictability of earnings.

Catalysts

About RateGain Travel Technologies- A Software as a Service (SaaS) company, provides solutions for hospitality and travel industries in India, North America, the Asia-Pacific, Europe, and internationally.

- Strong growth in new contract wins and a robust pipeline, especially in APAC and North America, position RateGain to capitalize on the ongoing digitization and expansion of the global travel industry, which is likely to drive sustained revenue growth over the coming quarters and years.

- Continued strategic investment in AI-powered product innovation (e.g., UNO VIVA, RG Insights, Smart ARI) and integrated, real-time analytics aligns RateGain's offerings with industry demand for data-driven decision-making and automation, supporting higher average contract values, improved product stickiness, and potential EBITDA margin expansion.

- Expansion into high-growth ancillary verticals (beyond hotels to airlines, car rentals, etc.) and a focus on integrated suites (like UNO) significantly broaden RateGain's addressable market and wallet share within client organizations, which can accelerate revenue growth and lead to improved operating leverage and net margins.

- The shift toward recurring, subscription/hybrid revenue streams now making up nearly half of total revenue, coupled with high renewal rates north of 35% in Adara, increases visibility and predictability in future earnings, which should support higher valuation multiples as the market recognizes improved cash flow stability.

- RateGain's strengthened go-to-market (GTM) execution, particularly in APAC and Middle East where digital travel adoption is surging, enhances its ability to win new logos and cross-sell/upsell to existing customers, driving both top-line growth and higher customer lifetime value, which should positively impact earnings and margin trajectory.

RateGain Travel Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

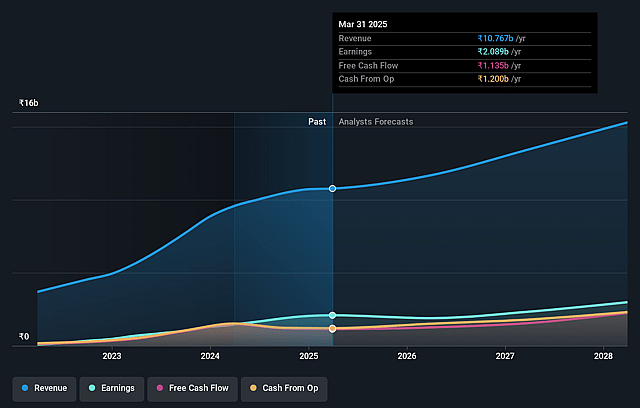

- Analysts are assuming RateGain Travel Technologies's revenue will grow by 27.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.7% today to 12.5% in 3 years time.

- Analysts expect earnings to reach ₹4.7 billion (and earnings per share of ₹43.5) by about July 2029, up from ₹1.9 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹6.0 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 33.7x on those 2029 earnings, down from 57.5x today. This future PE is greater than the current PE for the IN Software industry at 29.6x.

- Analysts expect the number of shares outstanding to grow by 0.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.16%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's Net Revenue Retention (NRR) has declined to 100%, indicating limited expansion sales to existing customers and potential stagnation in customer lifetime value, which may constrain long-term revenue and earnings growth if the trend persists.

- Over half of RateGain's revenue is now derived from transaction-based models, which tend to have lower gross margins and more variability compared to subscription revenue-this shift could compress net margins and make earnings less predictable over time.

- The organic growth in some legacy segments, particularly Adara DaaS and social media martech products, is flat or in decline, and the company remains exposed to revenue attrition as long-tail and legacy customers churn or are lost to consolidation, potentially limiting topline growth.

- The travel technology industry continues to see significant competition, as noted by management's openness to new competitors (e.g., "Guestara") and admission of 50% of new wins being displacement deals; this ongoing competitive pressure may impact pricing power and keep margins under pressure in the long term.

- A heavy focus on APAC and SMB markets may introduce execution risks around pricing sensitivity, slower customer ramp-up, and localized competition, which could impact the realization of revenue from the strong order pipeline and limit overall profitability in global expansion efforts.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹870.1 for RateGain Travel Technologies based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1100.0, and the most bearish reporting a price target of just ₹600.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹37.4 billion, earnings will come to ₹4.7 billion, and it would be trading on a PE ratio of 33.7x, assuming you use a discount rate of 15.2%.

- Given the current share price of ₹946.7, the analyst price target of ₹870.1 is 8.8% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on RateGain Travel Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.