Last Update 17 Jun 26

Fair value Decreased 0.40%HUN: Olin Merger And Portfolio Mix Will Shape Future Stock Returns

Analysts have raised the Huntsman price target by $0.06 to $14.25, citing updated views on the merger of equals with Olin, closer alignment of Huntsman stock with Olin stock, and differing strengths across chlorine, caustic, ethylene, polyurethane, and epoxy exposures.

Analyst Commentary

Recent research on Huntsman centers on the proposed merger with Olin, how Huntsman stock might track Olin stock, and how different parts of the chemicals portfolio could affect valuation and execution risk.

Bullish Takeaways

- Bullish analysts point to the merger of equals with Olin as a key reason for shifting to more neutral or balanced ratings on Huntsman. They suggest the combined structure could help support the stock relative to its prior standalone profile.

- Some see the closer alignment of Huntsman stock with Olin stock as a positive. They view Huntsman as now tied to a peer where they already hold a neutral stance, which reduces perceived company specific risk.

- Huntsman exposure to downstream polyurethane and epoxy is described as more differentiated. Bullish analysts view this as an offset to commodity heavy areas, which could support earnings quality and valuation multiples.

- Target prices cited in recent research, such as US$14 and US$15, frame a valuation range that bullish analysts view as reasonable given current information on the merger and industry conditions mentioned, including the methylene diphenyl diisocyanate market.

Bearish Takeaways

- Even as ratings move to Neutral, bearish analysts still highlight that Huntsman does not yet warrant a more positive stance. They indicate ongoing caution around execution on the Olin merger and integration of the different business lines.

- The reference to Olin having more of a cost advantage in U.S. gas advantaged chlorine, caustic and ethylene suggests that Huntsman may be at a relative disadvantage on the commodity side. This could weigh on margins if conditions become less favorable.

- Hold level ratings and modest price targets such as US$14 to US$15 imply that, for cautious analysts, upside appears limited relative to the risks around the merger and chemicals cycle exposure. This keeps them reluctant to move beyond a neutral stance.

- The reliance on linkage to Olin stock within the rating rationale signals that some bearish analysts see Huntsman valuation as heavily dependent on peer performance rather than company specific growth drivers alone, which can cap enthusiasm.

What’s in the News for Huntsman

- Olin Corporation and Huntsman agreed to an all stock merger to create OlinHuntsman Corporation, a North American chemicals company with over US$12.5b in annual revenue. Huntsman shareholders are set to receive 0.5476 Olin shares for each Huntsman share and hold 45.5% of the combined company. (Source: company announcement, multiple news reports)

- The combined OlinHuntsman is planned to be headquartered in The Woodlands, Texas. Olin CEO Ken Lane is expected to become CEO and Huntsman CEO Peter Huntsman would serve as non executive Chairman, supported by a 10 member board split evenly between Olin and Huntsman representatives. (Source: company announcement, multiple news reports)

- The merger agreement targets more than US$400m in annual cost synergies and integration benefits. This includes US$300m within three years and a further US$100m from 2031 onwards, subject to regulatory and shareholder approvals and an expected closing in the first half of 2027. (Source: company announcement, multiple news reports)

- Huntsman sold Huntsman Gomet, its Italian automotive aftermarket components business within the Polyurethanes division, to Trelleborg Group. The company stated that proceeds will be used to reduce outstanding borrowings. (Source: company announcement)

- Proxy advisory firms ISS and Glass Lewis recommended that Huntsman shareholders vote against the re election of director José Antonio Muñoz Barcelo due to attendance issues. Huntsman’s Board has urged investors to vote for all director nominees at the April 29, 2026 Annual Meeting. (Source: company announcement)

Valuation Changes for Huntsman Stock

- Fair Value: updated slightly lower from $14.31 to $14.25 per share, a change of about 0.4%.

- Discount Rate: reduced from 8.87% to 8.74%, indicating a modest adjustment to the required return used in the Huntsman valuation work.

- Revenue Growth: held effectively stable at 5.17%, with only a very small model refinement.

- Net Profit Margin: adjusted marginally higher from 9.04% to 9.10%, suggesting a slightly stronger earnings outlook within the existing Huntsman framework.

- Future P/E: moved from 5.55x to 5.47x, reflecting a small reduction in the earnings multiple applied to Huntsman stock.

Key Takeaways

- Shift toward specialty chemicals and eco-friendly products is expected to improve margins, strengthen market position, and reduce earnings volatility.

- Efficiency measures and strategic asset closures are aimed at boosting free cash flow and enhancing profitability as markets recover.

- Sustained overcapacity, high European costs, weak end-markets, volatile input prices, and economic uncertainty are driving margin compression and persistent earnings instability.

Catalysts

About Huntsman- Manufactures and sells diversified organic chemical products worldwide.

- Demand for Huntsman's advanced materials and polyurethane-based products is expected to benefit from accelerating global trends in sustainability, energy efficiency, and lightweighting-especially as infrastructure and construction activity resumes, and the EV/clean tech markets expand. This supports potential for higher long-term revenue growth and greater market share.

- The company is actively transforming its portfolio away from lower-margin, commodity chemicals toward specialty chemicals (e.g., adhesives, elastomers, aerospace composites), aiming to further improve EBITDA margins and overall profitability in future cycles.

- Cost optimization, working capital discipline, and strategic asset closures (e.g., the maleic anhydride facility in Europe) are expected to enhance free cash flow generation and support improved net margins and earnings resilience during the next macro upturn.

- Resumption of aerospace build rates and normalization in downstream end markets such as electronics and automotive are positioned to drive earnings recovery as macro conditions improve, providing upside to mid-cycle EBITDA levels.

- Ongoing tightening of environmental regulations and heightened customer demand for sustainable, eco-friendly solutions is likely to reinforce Huntsman's pricing power and reduce cyclicality-positively impacting revenues and supporting long-term margin expansion.

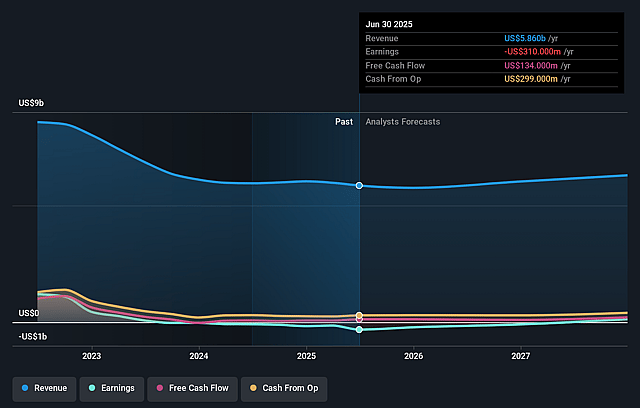

Huntsman Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Huntsman's revenue will grow by 5.2% annually over the next 3 years.

- Analysts are not forecasting that Huntsman will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Huntsman's profit margin will increase from -5.7% to the average US Chemicals industry of 9.1% in 3 years.

- If Huntsman's profit margin were to converge on the industry average, you could expect earnings to reach $602.8 million (and earnings per share of $3.34) by about June 2029, up from -$323.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 5.5x on those 2029 earnings, up from -7.2x today. This future PE is lower than the current PE for the US Chemicals industry at 27.5x.

- Analysts expect the number of shares outstanding to grow by 0.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.74%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Prolonged overcapacity in the global MDI/polyurethanes market, particularly from new or existing Chinese and European production, could keep utilization rates depressed (in the 80% range), resulting in persistent pricing pressure and limiting Huntsman's ability to expand revenue and restore net margins to historical levels.

- Intensified competition in Europe, where competitors are pursuing a volume-over-value strategy, is creating the company's highest production costs and lowest product values worldwide, risking further margin compression and sustained EBITDA weakness.

- Weakness in construction and housing end-markets, especially in North America and Europe, compounded by high interest rates and consumer uncertainty, is resulting in low volumes and an anemic sales environment, hampering revenue growth and prolonging earnings stagnation.

- Exposure to high, volatile raw material and energy costs in Europe, as demonstrated by the closure of energy-intensive facilities and persistent viability challenges for Huntsman's Rotterdam operations, puts further downward pressure on operating margins and threatens the profitability of the European footprint.

- Limited visibility on recovery timing, continued trade uncertainty (including tariffs and shifting import patterns), and muted customer confidence across end markets all create prolonged revenue instability and earnings volatility, making it difficult for Huntsman to deliver consistent financial improvements over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $14.25 for Huntsman based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $18.0, and the most bearish reporting a price target of just $10.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $6.6 billion, earnings will come to $602.8 million, and it would be trading on a PE ratio of 5.5x, assuming you use a discount rate of 8.7%.

- Given the current share price of $13.18, the analyst price target of $14.25 is 7.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Huntsman?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.