Key Takeaways

- Intensifying regulation, sustainability pressures, and competition from bio-based alternatives threaten core revenue streams and erode profitability across key end markets.

- Rising input costs, regional overcapacity, and global supply chain shifts constrain earnings growth and force strategic repositioning to preserve long-term viability.

- Structural cost reductions, focus on high-growth markets, and new product initiatives position Huntsman for enhanced margins and earnings as demand and macro conditions improve.

Catalysts

About Huntsman- Manufactures and sells diversified organic chemical products worldwide.

- Heightened global environmental regulation and anti-petrochemical sentiment are expected to result in steadily increasing compliance costs and potentially restricted market access for key Huntsman product lines, eroding net margins and limiting international revenue growth, particularly as regulators and consumers further penalize non-green materials.

- Accelerated adoption of sustainable and bio-based alternatives in major end markets, including automotive, construction, and consumer durables, threatens to displace legacy chemical products, creating structural headwinds for Huntsman's traditional revenue streams and forcing the company to cannibalize its own sales or lose market share.

- Ongoing geopolitical fragmentation, global supply chain reshoring, and persistent tariff volatility will likely increase the company's input costs and operational complexity, constraining both earnings growth and Huntsman's ability to benefit from emerging market expansion.

- The European market, which is already Huntsman's highest cost region and lowest value producer for MDI, faces continued overcapacity, rising energy costs, and a lack of sustainable demand recovery; these industry dynamics are likely to force further asset closures or impairments in coming years, weighing significantly on EBITDA and overall return on capital.

- Increasing competition from low-cost Asian and Middle Eastern producers, combined with both volatile raw material prices and rapid innovation from bio-based entrants, will continue to compress Huntsman's pricing power, depress profitability, and undermine the long-term stability of earnings and cash flows.

Huntsman Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Huntsman compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

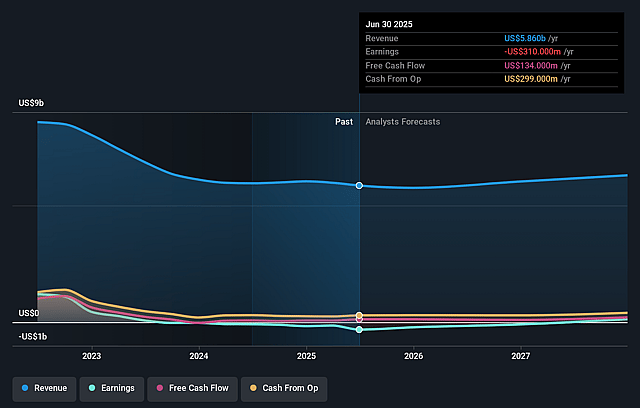

- The bearish analysts are assuming Huntsman's revenue will grow by 1.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -5.3% today to 2.0% in 3 years time.

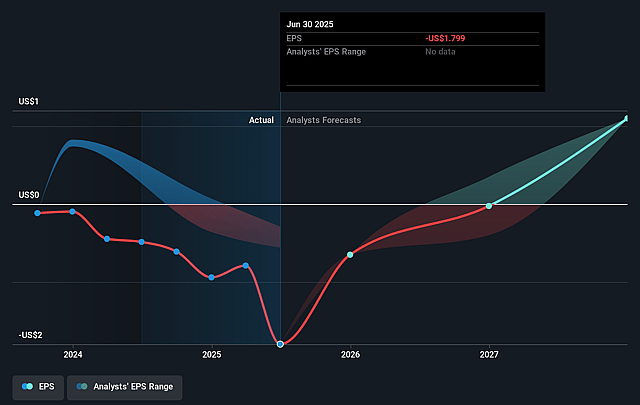

- The bearish analysts expect earnings to reach $121.5 million (and earnings per share of $1.85) by about September 2028, up from $-310.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 17.3x on those 2028 earnings, up from -6.1x today. This future PE is lower than the current PE for the US Chemicals industry at 25.8x.

- Analysts expect the number of shares outstanding to grow by 0.44% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.84%, as per the Simply Wall St company report.

Huntsman Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Management emphasizes that Huntsman has reduced its cost base and improved working capital discipline during the downturn, so as end markets recover, margins and net earnings are likely to structurally benefit from this leaner operating model.

- The company is focusing future bolt-on acquisitions and organic investments on Advanced Materials, adhesives, lightweighting, aerospace, and energy conservation markets-all supported by long-term secular trends toward sustainability and electrification, which should support top-line revenue growth and future cash flow.

- Executives highlighted that normalized demand in construction and automotive-sectors currently depressed by high interest rates and uncertain macro conditions-will likely return with macro improvement (such as lower interest rates), providing significant upside for revenue recovery and EBITDA margin expansion.

- Management expects China and the US to outperform Europe in the next cycle due to more competitive energy, labor, and raw material markets; strength in the Chinese automotive market and rising Chinese consumer demand offer long-term opportunities for volume and earnings growth.

- Huntsman indicated new downstream product introductions, upgraded facilities (such as Geismar catalysts and chip cleaning technology), and continued cost-out actions will position the company to capture disproportionate incremental earnings as global demand recovers and the cyclical trough passes, supporting future profitability and return on capital.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Huntsman is $9.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Huntsman's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $9.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $6.1 billion, earnings will come to $121.5 million, and it would be trading on a PE ratio of 17.3x, assuming you use a discount rate of 9.8%.

- Given the current share price of $10.82, the bearish analyst price target of $9.0 is 20.2% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.