Key Takeaways

- Structural cost reductions and streamlined operations position Huntsman for lasting cash generation and resilient margins through economic cycles.

- Growth in energy-efficient construction and advanced materials, alongside innovation in Asian markets, supports revenue expansion and improved earnings quality.

- Structural industry risks, environmental regulation, and high financial obligations threaten Huntsman's profitability, growth prospects, and ability to adapt to sustainability-driven market shifts.

Catalysts

About Huntsman- Manufactures and sells diversified organic chemical products worldwide.

- Analyst consensus expects improved MDI pricing and domestic volume due to tariffs and stabilizing costs, but given that U.S. and China MDI demand is currently running well below historical averages with exceptionally lean supply chains, any rebound in construction and auto demand could create a snap-back in pricing and margins far more pronounced than current forecasts suggest, resulting in outsized earnings and EBITDA recovery.

- While the consensus discusses incremental net margin improvement from cost cutting, Huntsman's demonstrated discipline in operating with lower inventory, structural cost reductions, and strategic portfolio streamlining positions the company not just for margin recovery but for a permanent step-change in cash generation and resilient net margin even amidst future cycles.

- Ongoing global urbanization and the accelerating shift to energy-efficient construction are likely to drive multi-year volume growth in high-margin polyurethane insulation and specialty building products, fueling sustained revenue growth as construction rebounds and retrofits intensify worldwide.

- Huntsman's specialty Advanced Materials and composites businesses are ideally placed to capture the surge in automotive lightweighting and electrification, as OEM demand for advanced adhesives, carbon fiber, and electronics materials outpaces GDP growth and supports sustained margin expansion.

- The company's active focus on serving growing Asian markets, coupled with a strong innovation pipeline and downstream product capabilities in catalysts and chip cleaning tech, can unlock outsized top-line growth and improve the earnings mix well beyond commodity MDI, potentially accelerating both revenue and net margin above peer averages.

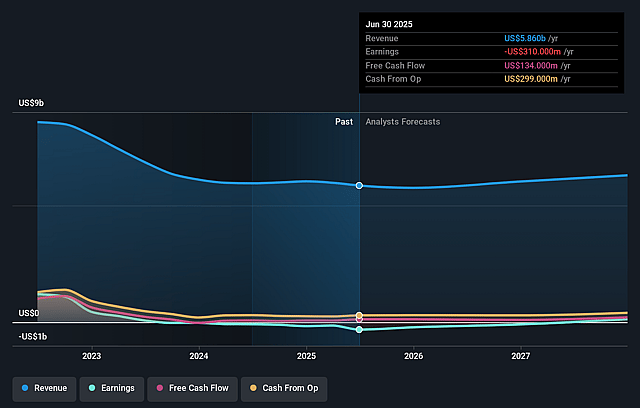

Huntsman Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Huntsman compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Huntsman's revenue will grow by 5.1% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -5.3% today to 4.3% in 3 years time.

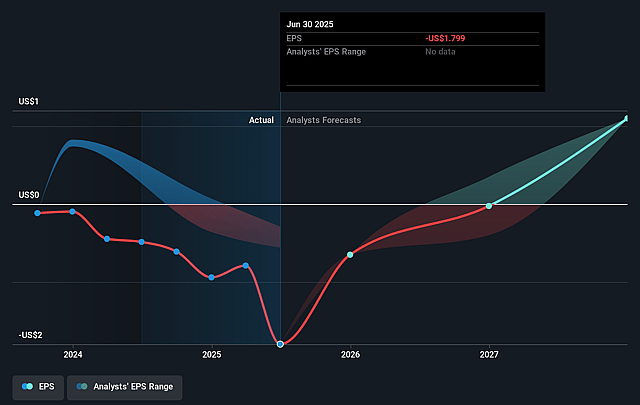

- The bullish analysts expect earnings to reach $293.7 million (and earnings per share of $1.88) by about September 2028, up from $-310.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 13.6x on those 2028 earnings, up from -6.3x today. This future PE is lower than the current PE for the US Chemicals industry at 25.9x.

- Analysts expect the number of shares outstanding to grow by 0.44% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.86%, as per the Simply Wall St company report.

Huntsman Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Huntsman's heavy reliance on cyclical, commoditized chemicals such as polyurethanes exposes the company to persistent price volatility and ongoing margin compression, which could negatively impact revenue stability and net earnings over the long term.

- Heightened global momentum toward decarbonization, net-zero emissions, and stricter environmental regulations is likely to increase compliance and operating costs for Huntsman, potentially weighing down future margins and earnings.

- The persistent global oversupply of commodity chemicals, particularly the continued capacity build-out in China as well as in the Middle East and Asia, is expected to exert sustained downward pressure on prices for Huntsman's core products, undermining profitability and revenue growth.

- Sustainability demands and regulatory pressure are accelerating a shift away from petrochemical-based products toward more recyclable, bio-based, or alternative materials, which may result in structural declines in long-term demand for Huntsman's offerings and eventually suppress future revenues.

- Elevated legacy debt, significant pension obligations, and the high capital intensity of the industry may constrain Huntsman's financial flexibility, limiting its ability to invest in innovation, R&D, or strategic acquisitions that are needed to adapt to industry transformation, thus putting future free cash flow and earnings growth at risk.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Huntsman is $17.16, which represents two standard deviations above the consensus price target of $11.23. This valuation is based on what can be assumed as the expectations of Huntsman's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $9.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $6.8 billion, earnings will come to $293.7 million, and it would be trading on a PE ratio of 13.6x, assuming you use a discount rate of 9.9%.

- Given the current share price of $11.23, the bullish analyst price target of $17.16 is 34.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.