Last Update 30 Apr 26

UMAC: Index Inclusion And Recent Equity Raise Will Support Future Upside

Analysts are maintaining their $20.00 price target for Unusual Machines, citing updated assumptions that now reflect slightly higher projected revenue growth, a modestly lower profit margin, and a higher future P/E of 169.50x, which together keep their fair value view broadly unchanged.

What's in the News

- Unusual Machines completed a follow on equity offering of approximately $150.0m, issuing 8,823,529 common shares at $17 per share with a $1.19 discount per security (company event filing).

- The company previously filed for this follow on equity offering of common stock, signaling plans to raise additional capital through the public markets (company event filing).

- Executive officers, directors, and certain other holders agreed to a lock up on specified stock options from 23 March 2026 to 23 May 2026, limiting their ability to sell or transfer those securities during that 61 day window (lock up agreement).

- Separate from the options, 38,961,019 common shares are also under a lock up from 23 March 2026 to 23 May 2026, with similar restrictions on sales, transfers, and related transactions during that period (lock up agreement).

- Unusual Machines was added to the S&P Technology Hardware Select Industry Index, which may affect how certain index linked funds and benchmarks gain exposure to the stock (index provider notice).

Valuation Changes

- Fair Value: The $20.00 per share fair value is unchanged, indicating no adjustment to the overall price estimate.

- Discount Rate: The discount rate has edged lower from 8.38% to 8.38%, reflecting a very small technical adjustment in the model.

- Revenue Growth: Revenue growth assumptions have risen slightly from 101.11% to 102.29%, implying a marginally higher top line outlook in the forecast period.

- Net Profit Margin: The assumed net profit margin has been trimmed from 8.08% to 7.62%, pointing to a modestly less profitable earnings profile in the projections.

- Future P/E: The future P/E multiple has been raised from 162.54x to 169.50x, indicating that more of the $20.00 valuation is now attributed to a higher expected earnings multiple.

Key Takeaways

- Rapid scaling and reliance on government contracts expose the company to operational, supply chain, and forecasting risks, potentially delaying growth and pressuring margins.

- High expenses and limited brand recognition may hinder profitability and market share gains if revenue or innovation does not outpace established competitors.

- Heavy reliance on U.S. government contracts and domestic market advantages heightens vulnerability to regulatory shifts, execution challenges, and intense competition, risking growth and profitability.

Catalysts

About Unusual Machines- Engages in the commercial drone industry.

- Although Unusual Machines benefits from the rapid growth in automation, robotics, and government investment in drone technology, significant operational risks remain as the company attempts to scale production and workforce rapidly; any execution missteps in scaling manufacturing or unexpected supply chain disruptions could delay anticipated revenue growth and threaten future gross margins.

- Despite strong top-line momentum, with record revenues and gross margin improvements, the company still faces cash burn and losses from high operating expenses and substantial stock-based compensation; if revenue scale does not materialize as quickly as expected or if sustained gross margin expansion proves challenging, this could delay the timeline to achieving positive earnings or cash flow.

- While Unusual Machines is well capitalized and expects to benefit from regulatory and policy tailwinds, its heavy dependence on a timely and robust ramp in U.S. government orders introduces material forecasting uncertainty; bureaucratic delays or changes in government procurement priorities could leave the company with excess capacity, resulting in lower than expected revenues.

- Although the underlying trend of increased digitization, proliferation of IoT devices, and the shift to domestic/U.S.-based drone production plays to the firm's strengths, persistent risks of component shortages (e.g., magnets for motors) or sudden shifts in technology standards could force ongoing reinvestment, impacting EBITDA margins and necessitating more working capital.

- While Unusual Machines' expansion into new manufacturing lines and acquisitions positions it to address new verticals and higher-margin proprietary products, the company still lacks longstanding brand recognition and must compete against better-resourced incumbents; if its R&D spending fails to translate quickly into differentiated offerings or if vertical integration efforts stall, future market share expansion and sustainable margin gains could fall short of projections.

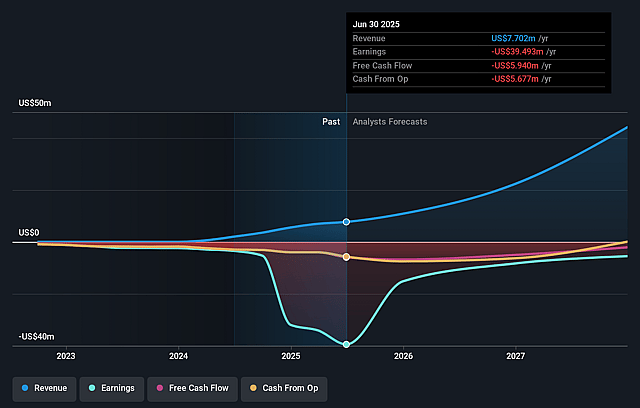

Unusual Machines Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Unusual Machines compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Unusual Machines's revenue will grow by 102.3% annually over the next 3 years.

- The bearish analysts are not forecasting that Unusual Machines will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Unusual Machines's profit margin will increase from -171.4% to the average US Electronic industry of 7.6% in 3 years.

- If Unusual Machines's profit margin were to converge on the industry average, you could expect earnings to reach $7.1 million (and earnings per share of $0.15) by about April 2029, up from -$19.2 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $30.7 million in earnings, and the most bearish expecting $-2.6 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 171.8x on those 2029 earnings, up from -34.2x today. This future PE is greater than the current PE for the US Electronic industry at 26.8x.

- The bearish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.38%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- A significant portion of Unusual Machines' near-term growth is predicated on pending U.S. government orders and mechanisms like the PBAS program; any delay, reduction, or failure in such contract awards would directly hurt revenues, cash flow, and growth expectations.

- Execution risk associated with scaling manufacturing-even with capital in hand-remains high, and setbacks in ramping up new facilities or integrating acquisitions like Rotor Lab could drive up operating expenses and delay path to positive net margins.

- The company's ability to maintain or improve gross margins depends on successfully passing through tariff and production cost increases to customers and achieving rapid learning curves for new product lines; a misstep here could compress margins and delay profitability.

- Intense competition both from larger incumbents as well as lower-cost international manufacturers, especially in an industry facing rapid technological change, could make it difficult for Unusual Machines to win and retain share, potentially flattening revenues and reducing pricing power.

- The company's current focus on the domestic market and reliance on U.S.-centric regulatory or geopolitical tailwinds may backfire if there is a shift in trade or drone regulations, reduced government spending, or slowing demand from U.S. enterprise and government channels, adversely affecting top-line growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Unusual Machines is $20.0, which represents up to two standard deviations below the consensus price target of $24.2. This valuation is based on what can be assumed as the expectations of Unusual Machines's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $30.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $92.7 million, earnings will come to $7.1 million, and it would be trading on a PE ratio of 171.8x, assuming you use a discount rate of 8.4%.

- Given the current share price of $13.74, the analyst price target of $20.0 is 31.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Unusual Machines?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.