Last Update 27 May 26

QLYS: Sector Pullback And Execution Concerns Will Pressure Future Remediation Upside

Analysts have reduced their blended price target on Qualys by adjusting revenue growth expectations and P/E assumptions. This has led to an updated target that is $26 lower than before, with analysts citing recent sector pullbacks and company specific concerns in their rationale.

Analyst Commentary

Recent Street research on Qualys shows a cluster of reduced price targets across several firms, with only one instance of a modest price target increase. Bearish analysts are generally aligning around lower revenue assumptions and more conservative P/E multiples, reflecting heightened scrutiny on execution and growth visibility.

In addition to multiple price target cuts, one firm has downgraded the stock, signalling that some coverage has shifted from more optimistic views to a clearly cautious stance. Against this backdrop, the lone price target increase appears to be an outlier rather than a broad change in sentiment.

JPMorgan and other bearish analysts have cited sector wide pullbacks alongside company specific issues in their recent updates. These moves collectively point to a recalibration of expectations rather than short term volatility alone.

Bearish Takeaways

- Clusters of price target reductions, including cuts of US$21 to US$55 in several reports, suggest bearish analysts are rethinking what they are willing to pay for Qualys based on current growth and profitability assumptions.

- The downgrade at William Blair alongside repeated target resets indicates concern that execution and growth consistency may not fully support previous valuation levels.

- Larger target cuts, such as those around US$35 to US$55, highlight perceived downside risks if revenue trends or margin performance do not match earlier expectations.

- Even where one firm raised its price target by US$5, this sits against a broader backdrop of reductions and reinforces a cautious overall tone on valuation and the balance of risk versus reward.

What's in the News

- The White House held a briefing on a planned executive order that would let U.S. agencies review advanced AI models before release, with cybersecurity companies including Qualys mentioned among sector peers that could be affected by evolving oversight of large language models (The Information).

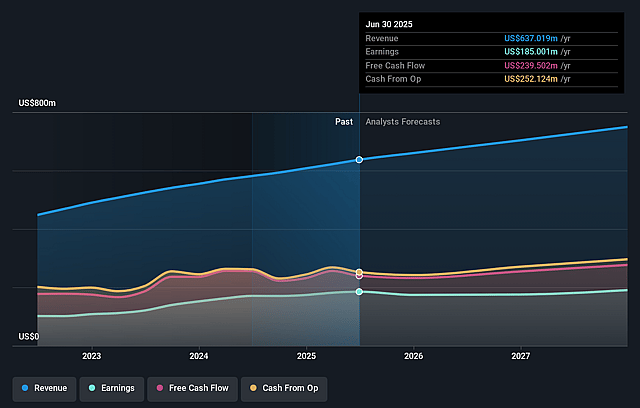

- Qualys updated full-year 2026 guidance, now expecting revenues of US$721.0 million to US$727.0 million and GAAP net income per diluted share of US$5.40 to US$5.61, based on an assumed 21% tax rate and about 34.5 million diluted shares outstanding.

- The company issued guidance for the second quarter of 2026, targeting revenues of US$177.5 million to US$179.5 million and GAAP net income per diluted share of US$1.24 to US$1.31, assuming a 21% tax rate and about 35.0 million diluted shares outstanding.

- Qualys reported an unaudited impairment charge on property and equipment of US$624,000 for the first quarter of 2026.

- Qualys announced a joint offering with Converge that uses the Qualys Converge Connect Insurance Report within Enterprise TruRisk Management to help customers present real-time security data to cyber insurers, potentially supporting more tailored premium decisions.

- The company introduced Agent Val within Enterprise TruRisk Management, an agent-led exploit validation and risk remediation capability that uses TruConfirm to test exploitability in live environments and feed confirmed results back into the platform for prioritized remediation.

Valuation Changes

- Fair Value remained steady at $85.0 per share, indicating no change in the central valuation estimate.

- Discount Rate increased slightly from 8.51% to 8.51%, representing a very small adjustment to the required rate of return used in the model.

- Revenue Growth was reduced from 7.00% to 6.43%, reflecting a more conservative assumption for future top-line expansion.

- Net Profit Margin increased from 24.83% to 25.40%, implying a slightly stronger long-term earnings profile on each dollar of revenue.

- Future P/E was lowered from 17.61x to 16.57x, indicating a more cautious stance on how much investors may be willing to pay for forecast earnings.

Key Takeaways

- Embedded security features in major cloud platforms threaten to reduce demand for Qualys’ tools as customers consolidate spending with larger providers.

- Shifts toward integrated security, regulatory hurdles, and aggressive competition could compress margins, slow growth, and erode Qualys’ market share.

- Strong industry demand, innovative platform expansion, and effective partner strategies position Qualys for resilient recurring revenue, improved margins, and competitive advantage amid rising cybersecurity needs.

Catalysts

About Qualys- Provides cloud-based platform delivering information technology (IT), security, and compliance solutions in the United States and internationally.

- The ongoing rise of cloud infrastructure managed by hyperscale providers such as AWS and Azure is likely to result in significant security capabilities being embedded natively in cloud offerings, which could substantially erode demand for Qualys’ third-party security tools and negatively impact future revenue growth as customers consolidate spend within the hyperscaler ecosystem.

- Increasing regulatory scrutiny around data privacy and cross-border data flows is expected to create additional compliance costs or impede Qualys’ ability to scale internationally, leading to margin compression and slower expansion of overall earnings power.

- The rapid shift towards integrated, all-in-one security platforms by larger enterprises may favor more diversified or horizontally integrated cybersecurity companies, leaving Qualys, with its reliance on vulnerability management and slower entry into adjacent markets, at risk of declining customer retention and weaker top-line growth.

- Intense competition and the accelerating pace of AI-driven security innovation among peers could expose Qualys’ slower innovation cycles, resulting in long-term erosion of market share and stagnation in revenue from its core product offerings.

- Growing industry consolidation may lead to dominant players bundling security solutions at aggressive price points, thereby elevating customer acquisition costs for Qualys and ultimately exerting sustained downward pressure on both net margins and earnings growth over the long run.

Qualys Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Qualys compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Qualys's revenue will grow by 6.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 29.4% today to 25.4% in 3 years time.

- The bearish analysts expect earnings to reach $209.7 million (and earnings per share of $5.76) by about May 2029, up from $201.4 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $238.8 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 16.9x on those 2029 earnings, down from 17.9x today. This future PE is lower than the current PE for the US Software industry at 30.0x.

- The bearish analysts expect the number of shares outstanding to decline by 2.43% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.51%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The acceleration of digital transformation and the proliferation of cloud adoption are greatly expanding organizations’ cybersecurity needs, fueling persistent demand for unified cloud-native solutions like Qualys, which could drive sustained revenue growth and help maintain strong earnings.

- Intensifying regulation worldwide around cybersecurity and audit readiness is proving to be a strong secular tailwind, as organizations must invest in automated risk management, compliance, and evidence collection solutions—an area where Qualys is innovating and gaining customer traction, which could help stabilize and grow net margins.

- Qualys’ expansion and rapid innovation of its unified cloud platform—including new products like the Enterprise TruRisk Management (ETM) and TotalAI—are driving greater customer stickiness, furthering upsell opportunities, and increasing average revenue per user, which in turn supports predictable recurring revenues and long-term profitability.

- The company’s partner-first strategy is accelerating, with nearly half of revenue now coming through partners, international growth outpacing domestic, and partner-led bookings increasing, all of which could lower customer acquisition costs and expand revenue opportunities, thus improving earnings and operating leverage over time.

- As cyber threats escalate and enterprise customers seek to consolidate fragmented security tooling onto integrated platforms, Qualys’ ability to ingest and orchestrate data across its own and third-party solutions sets it up to benefit from industry consolidation, allowing continued margin expansion and top-line growth even as competitors enter the space.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Qualys is $85.0, which represents up to two standard deviations below the consensus price target of $107.39. This valuation is based on what can be assumed as the expectations of Qualys's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $161.0, and the most bearish reporting a price target of just $85.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $825.8 million, earnings will come to $209.7 million, and it would be trading on a PE ratio of 16.9x, assuming you use a discount rate of 8.5%.

- Given the current share price of $102.31, the analyst price target of $85.0 is 20.4% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Qualys?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.