Last Update 08 May 26

Fair value Decreased 21%QLYS: AI Resilient Remediation Focus Will Support Future EPS Durability

Qualys' updated fair value estimate has shifted from about $136 to $107, as analysts recalibrated price targets in light of recent sectorwide target cuts and slightly lower assumptions for long term margins and P/E multiples, even as some still highlight the stock's focus on remediation and patching as a relative strength within cybersecurity.

Analyst Commentary

Recent research on Qualys reflects a mix of caution and selective optimism, with multiple firms revisiting price targets and ratings as they reassess both sector risks and the company’s positioning in cybersecurity and AI related headlines.

Bullish Takeaways

- Bullish analysts highlight Qualys’ focus on remediation and patching as a potential differentiator within vulnerability and virtual machine security, which they see as relatively insulated compared with some peers as AI tools evolve.

- Some research points to AI coding assistants, such as Claude Code Security, as tools that support developer productivity without replacing security platforms, which analysts say helps preserve structural demand for established cybersecurity vendors, including Qualys.

- Despite sectorwide pressure after recent AI related news, bullish analysts frame the reaction as more headline driven than fundamental for leading platforms, which supports maintaining or modestly increasing fair value estimates for companies seen as better positioned.

- A limited price target increase from RBC Capital, alongside more constructive commentary from a few firms, indicates that not all research views the recent sector pullback as purely negative for Qualys’ long term execution and valuation framework.

Bearish Takeaways

- Bearish analysts have cut Qualys price targets by a wide range, including reductions of $55, $49, $35, $35, $26, $25, $21, and $1, which collectively signal more cautious assumptions for valuation multiples and possibly execution risk versus prior expectations.

- A recent downgrade at William Blair adds to the cautious tone, with investors being reminded that even with perceived product strengths, the stock may face higher scrutiny on growth consistency and competitive positioning.

- Some research flags that as large language model providers expand security related offerings, competition for cyber related budgets could intensify, which bearish analysts see as a risk for premium P/E assumptions across the group, including Qualys.

- Commentary around headline headwinds from AI tools suggests that sentiment on cybersecurity stocks may remain pressured until there is more clarity on how AI related security spending trends translate into measurable growth for established vendors.

What's in the News

- Qualys updated full year 2026 guidance, now expecting revenues of US$721.0 million to US$727.0 million and GAAP net income per diluted share of US$5.40 to US$5.61, assuming a 21% effective tax rate and about 34.5 million diluted shares (company guidance).

- The company issued earnings guidance for the second quarter of 2026, targeting revenues of US$177.5 million to US$179.5 million and GAAP net income per diluted share of US$1.24 to US$1.31, based on a 21% effective tax rate and about 35.0 million diluted shares (company guidance).

- Qualys reported an unaudited impairment of property and equipment of US$624,000 for the first quarter ended March 31, 2026 (company filing).

- Qualys and Converge announced a joint offering that uses the Qualys Enterprise TruRisk Management platform to generate a Qualys Converge Connect Insurance Report. Cyber insurers can use this report to help assess security posture and price cyber insurance premiums. The report is now available in ETM (company announcement).

- Qualys launched Agent Val within Enterprise TruRisk Management as an agent led exploit validation and autonomous risk remediation capability. It is described as an AI orchestration layer that tests exploitability, feeds confirmed issues into ETM, and is included as part of ETM. This capability is now generally available (company announcement).

Valuation Changes

- Fair Value: recalibrated from about $135.91 to about $107.39, representing a sizable downward move in the updated model.

- Discount Rate: increased from 8.45% to about 8.55%, implying a slightly higher required return for the stock.

- Revenue Growth: adjusted from about 7.22% to about 7.12%, reflecting a modestly more conservative topline outlook in the forecast.

- Net Profit Margin: revised from about 27.19% to about 26.38%, indicating a slightly lower expected level of profitability in future years.

- Future P/E: reduced from roughly 25.51x to about 19.79x, pointing to a lower valuation multiple applied in the updated fair value framework.

Key Takeaways

- Cloud-native platforms, AI innovation, and flexible pricing drive expansion, retention, and strong margins through unified cybersecurity and broadening market opportunities.

- Strategic partner ecosystem and government wins accelerate growth, international reach, and integrate regulatory compliance, bolstering Qualys' leadership in proactive risk management.

- Rapid AI security evolution, shifting customer preferences, pricing model uncertainty, macroeconomic challenges, and costly growth investments threaten Qualys' revenue visibility, margins, and long-term growth.

Catalysts

About Qualys- Provides cloud-based platform delivering information technology (IT), security, and compliance solutions in the United States and internationally.

- Adoption of Qualys' new cloud-native risk operations center (ROC) and Agentic AI platform positions the company as a leading pre-breach risk management provider, offering unified orchestration, automation, and remediation across both Qualys and non-Qualys data; this opens incremental greenfield opportunities and should support higher ARPU and expanded TAM, leading to durable revenue and earnings growth.

- Persistent digital transformation, cloud adoption, and increased regulatory scrutiny (such as GDPR and FedRAMP High compliance) are driving organizations globally to invest in proactive, unified cybersecurity solutions; Qualys' platform-first approach and recent government sector wins (aided by exclusive FedRAMP High authorization) are expected to drive faster land-and-expand cycles and incremental long-term revenues.

- Flex (QLU) pricing and expanded module integration reduce adoption friction and incentivize larger initial commitments as well as multi-module expansion within existing accounts, directly supporting higher net retention and improving margins by leveraging the SaaS delivery model's operating leverage.

- Strategic investments in partner ecosystems (reseller channels, mROC, and technical alliances) have increased channel contribution to nearly half of total revenues, which is scaling faster than direct sales; this should accelerate new logo acquisition, international reach, and upsell activity, thus supporting both revenue growth and healthy margin expansion.

- Rapid, continuous innovation-embedding AI-driven automation into remediation workloads and launching identity security posture management (ISPM)-is tightly aligned with industry shifts toward integrated, cloud-based, and continuous security, which strengthens Qualys' competitive position and increases the potential for higher customer retention, elevated margins, and sustained multi-year revenue growth.

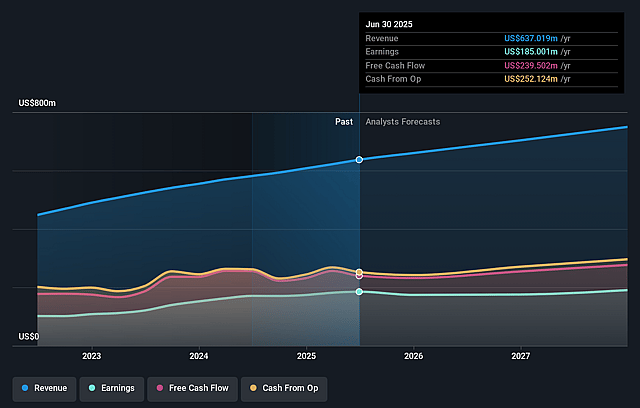

Qualys Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Qualys's revenue will grow by 7.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 29.4% today to 26.4% in 3 years time.

- Analysts expect earnings to reach $222.1 million (and earnings per share of $6.21) by about May 2029, up from $201.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.8x on those 2029 earnings, up from 16.6x today. This future PE is lower than the current PE for the US Software industry at 29.3x.

- Analysts expect the number of shares outstanding to decline by 3.05% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.55%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The pace of innovation in AI security is described as "rapid" and "dynamic," raising the risk that Qualys' internally developed AI agents and platform could quickly fall behind competitors or more agile upstarts, potentially resulting in increased R&D expense, product obsolescence, or customer attrition that would negatively affect revenue growth and net margins.

- Qualys acknowledges that customers increasingly prefer to consolidate certain security tools but often retain other vendors for key functions like identity or endpoint security, suggesting that vendor consolidation (especially with large platforms or hyperscalers) could eventually squeeze Qualys out of "all-in-one" enterprise deals, leading to slower revenue expansion or market share erosion.

- The newly introduced Flex pricing and QLU model, while designed to drive upsell and larger initial commitments, introduces uncertainty around usage patterns and may result in customers optimizing spend and using fewer Qualys units than anticipated, potentially impacting average revenue per customer and revenue visibility.

- Despite strong margins, the financial guidance and management's comments highlight continued macroeconomic uncertainty and "challenging environment for new business growth," indicating persistent headwinds that could prolong slower bookings, limit billings/revenue acceleration, and constrain near-term and potentially long-term earnings growth.

- The company's significant recent investments in go-to-market, public sector, and sales and marketing initiatives (including new executive hires) are intended to drive future growth, but if these investments do not lead to expected pipeline conversion, increased competition and operating expense growth could put pressure on free cash flow and EBITDA margins over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $107.39 for Qualys based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $161.0, and the most bearish reporting a price target of just $85.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $841.9 million, earnings will come to $222.1 million, and it would be trading on a PE ratio of 19.8x, assuming you use a discount rate of 8.5%.

- Given the current share price of $94.93, the analyst price target of $107.39 is 11.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Qualys?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.