Last Update 07 Apr 26

Fair value Increased 14%PDN: Langer Heinrich Cost Reset And Share Pullback Will Support Future Upside

Narrative Update: Paladin Energy Analyst Price Target Shift

The analyst price target for Paladin Energy has moved from A$11.11 to A$12.72. Analysts point to recent share price weakness and revised cost forecasts at Langer Heinrich as key factors supporting perceived value at current levels.

Analyst Commentary

Bullish analysts are framing the recent move in the price target as a valuation call, with the share price pullback and updated cost assumptions at Langer Heinrich both feeding into their revised view.

Bullish Takeaways

- Recent share price weakness is seen as creating a more appealing entry point relative to updated estimates, which supports the higher A$13.50 price target.

- The upward revision to cost forecasts at Langer Heinrich is viewed as a more realistic reflection of mining phase costs. This may reduce the risk of future negative surprises in models.

- Reaffirming an Outperform stance suggests confidence that execution at Langer Heinrich, even with higher cost assumptions, can still support the current valuation framework.

- Analysts appear comfortable that the combination of revised costs and the current share price already captures a fair amount of operational risk.

Bearish Takeaways

- Higher cost forecasts at Langer Heinrich point to less margin headroom if uranium prices or volumes do not evolve in the company’s favor.

- The reliance on recent share price weakness as a key support for the thesis leaves the case more vulnerable if the stock re-rates without matching fundamental progress.

- Mining phase costs can be volatile. Even updated assumptions may still be tested if operational performance or conditions at Langer Heinrich shift.

- Any further revisions to project costs would likely force analysts to reassess valuation frameworks, which could affect future price targets.

What's in the News

- Paladin Energy received ministerial approval for its Environmental Impact Statement under The Environmental Assessment Act in Saskatchewan for the Patterson Lake South project in the Athabasca Basin, Canada (Key Developments).

- The Saskatchewan Minister of Environment formally approved the Environmental Impact Statement for the shallow, high grade Patterson Lake South project, following earlier technical acceptance in June 2025 (Key Developments).

- The Environmental Impact Statement approval followed a public review period from July to September 2025, which was part of the regulatory process for the Patterson Lake South project (Key Developments).

- This Environmental Assessment approval is described as an important regulatory milestone for Patterson Lake South and is a prerequisite for future permits and licences required for construction and operation (Key Developments).

Valuation Changes

- Fair Value: A$11.11 to A$12.72, a moderate uplift in the analyst assessment of underlying value.

- Discount Rate: Steady at 6.854%, indicating no change in the risk rate applied to cash flows.

- Revenue Growth: Revenue growth assumption adjusted from 46.06% to 32.67%, a sizeable reduction in the projected growth rate.

- Net Profit Margin: Net profit margin assumption refined from 30.63% to 33.39%, a modest improvement in expected profitability per dollar of revenue.

- Future P/E: Forward P/E multiple nudged from 31.29x to 31.72x, a slight increase in the earnings valuation multiple used in the model.

Key Takeaways

- Growing Western demand, successful asset acquisitions, and operational ramp-up position Paladin for higher sales, improved margins, and expansion in revenue and cash flow.

- Strategic new projects and exploration activities support long-term production growth, increased asset value, and stronger shareholder returns.

- Regulatory delays, rising project costs, operational risks, and uncertain funding could significantly constrain Paladin Energy's long-term profitability and shareholder value.

Catalysts

About Paladin Energy- Engages in the development, exploration, evaluation, and operation of uranium mines in Australia, Canada, and Namibia.

- Paladin is set to benefit from sustained, increasing global demand for non-Russian, non-Chinese uranium supply, as evidenced by utility contracting trends, growing Western interest, and the company's advances in securing agreements and permits for Canadian assets; this should improve future sales volumes and pricing power, positively impacting revenue growth and gross margins.

- Completion of the ramp-up at the Langer Heinrich mine and transition to full operational capacity by FY 2027, combined with the asset's low cost structure, positions Paladin for significant production and cash flow growth, increasing EBITDA and net margin expansion.

- The addition of the high-quality Patterson Lake South (PLS) project-targeted for first production in 2031 and benefiting from compelling project economics and a globally strategic location-provides Paladin with a clear pathway to long-term production growth, contributing to both asset value and future top-line expansion.

- Ongoing and planned exploration drilling at Saloon East and PLS is expected to unlock further resource upside, providing optionality for reserve and production growth and creating potential for future strategic partnerships, thereby supporting long-term shareholder returns and balance sheet strength.

- Tightening global uranium supplies-highlighted by recent announcements of production shortfalls by major producers and visible near-term utility procurement needs-suggest that spot and contract prices will remain elevated or increase, enhancing the company's future realized prices and free cash flow.

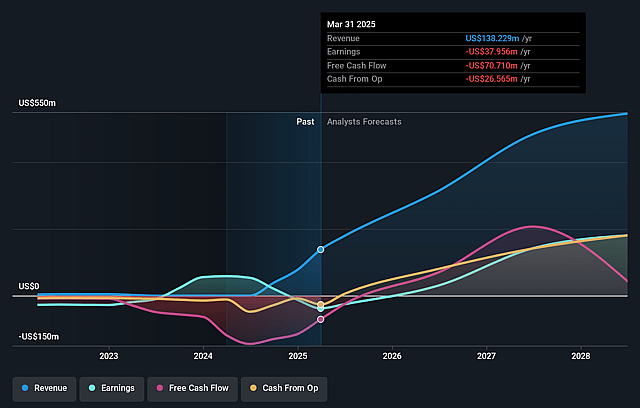

Paladin Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Paladin Energy's revenue will grow by 32.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from -16.4% today to 33.4% in 3 years time.

- Analysts expect earnings to reach $186.2 million (and earnings per share of $0.33) by about April 2029, up from -$39.2 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $210.2 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 31.7x on those 2029 earnings, up from -90.3x today. This future PE is greater than the current PE for the AU Oil and Gas industry at 16.9x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.85%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The PLS project has a lengthy development timeline, with first production not expected until 2031 due largely to a rigorous and potentially unpredictable Canadian regulatory process; delays or permitting challenges would postpone future revenue streams and impact long-term earnings projections.

- Recent increases in capital expenditures for PLS-driven by rising construction, labor, and infrastructure costs-raise the risk of further cost overruns, which could adversely impact Paladin's net margins and put pressure on future free cash flow, especially if uranium price assumptions prove optimistic.

- Paladin's future production and earnings are highly leveraged to the successful ramp-up and continued operation of the Langer Heinrich mine; any operational disruptions, reserve downgrades from declining ore grades, or lower-than-expected recovery could sharply reduce revenues and margins.

- Paladin's funding strategy for major developments like PLS remains uncertain, potentially requiring debt, equity issuance, or the sale of strategic project interests; reliance on capital markets or dilution from equity raises could negatively impact long-term earnings per share and shareholder value.

- Industry-wide risks-including the possibility of renewed uranium oversupply from ramped-up global projects or lower-than-expected utility contracting volumes-could limit uranium price growth, constraining Paladin's top-line potential and pressuring long-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of A$12.72 for Paladin Energy based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$17.75, and the most bearish reporting a price target of just A$7.17.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $557.6 million, earnings will come to $186.2 million, and it would be trading on a PE ratio of 31.7x, assuming you use a discount rate of 6.9%.

- Given the current share price of A$11.38, the analyst price target of A$12.72 is 10.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Paladin Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.