Key Takeaways

- Vistra's acquisition of Energy Harbor and plant license renewal is set to boost revenue and expand their customer base sustainably.

- Secured power purchase agreements and capacity expansions in renewables and gas build profitability and investor confidence amidst market volatility.

- Regulatory and operational challenges in key markets and projects could impact future revenues, earnings, and net margins due to uncertainties and potential delays.

Catalysts

About Vistra- Operates as an integrated retail electricity and power generation company in the United States.

- Vistra's acquisition of Energy Harbor, including new nuclear sites and 1 million retail customers, combined with the renewal of the Comanche Peak nuclear power plant's 20-year license, provides a catalyst for increased revenue and earnings, as it expands their asset base and customer reach sustainably.

- The company's secured power purchase agreements for its renewable pipeline, along with plans for significant capacity additions through the conversion and extension of existing plants and new gas builds, are expected to drive revenue growth as they meet increasing demand in their key markets.

- Vistra's strong financial performance, reflected in adjusted EBITDA that significantly exceeded guidance, underpins the potential for robust earnings growth driven by their diversified portfolio, even in volatile power markets, enhancing investor confidence.

- The anticipated 10% capacity uprate across their nuclear fleet by the early 2030s, alongside solar and battery storage projects tied to contracts with major firms such as Amazon and Microsoft, enhances long-term revenue streams and operational efficiency.

- Vistra's disciplined capital allocation, including planned share repurchases of at least $2 billion through 2025 and 2026 and maintaining a low net debt to EBITDA ratio, is poised to enhance shareholder value and improve earnings per share, supporting further bullish forecasts.

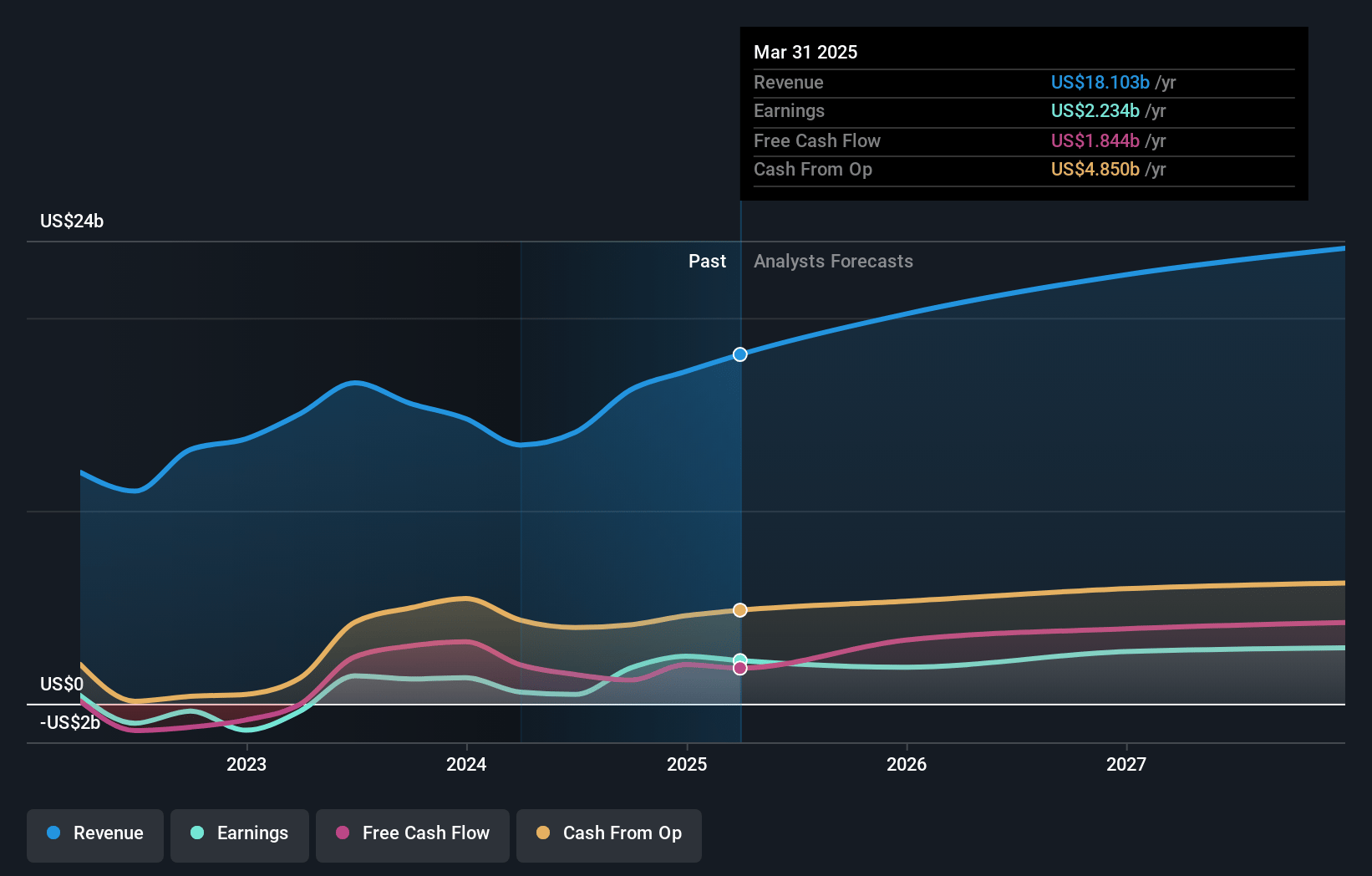

Vistra Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Vistra compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Vistra's revenue will grow by 16.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 14.3% today to 11.9% in 3 years time.

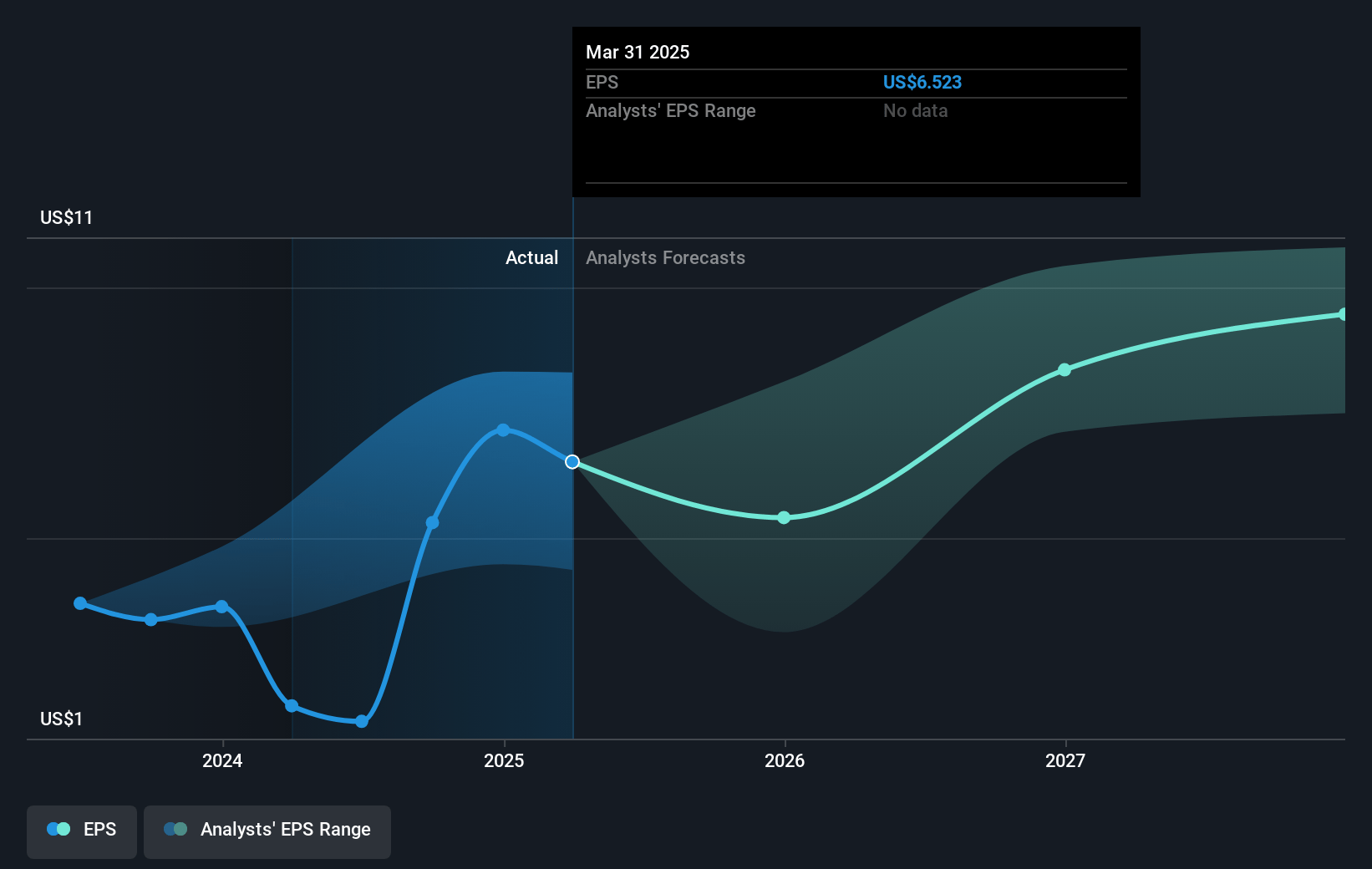

- The bullish analysts expect earnings to reach $3.3 billion (and earnings per share of $10.31) by about April 2028, up from $2.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 24.2x on those 2028 earnings, up from 15.5x today. This future PE is lower than the current PE for the US Renewable Energy industry at 32.3x.

- Analysts expect the number of shares outstanding to decline by 2.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.57%, as per the Simply Wall St company report.

Vistra Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Regulatory uncertainty in PJM and ERCOT markets, such as final approval of the 2026-2027 PJM auction parameters and ongoing changes in market design, could impact future revenues and earnings.

- Delays or complications in securing necessary permits and regulatory clarity for colocation data center deals, especially under scrutiny at state and federal levels, might impact revenue from expected growth and partnerships.

- Rising interest and potential legislative barriers in Texas related to grid reliability and market reforms might impede load growth projections, affecting revenues and net margins.

- Potential risks related to the Moss Landing battery storage facility incident and the time required for insurance recoveries, which could result in unexpected costs impacting net margins.

- Challenges in managing power purchase agreements and execution risk associated with development and conversion projects like the Coleto Creek plant, which might affect future revenue streams and operational costs.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Vistra is $207.52, which represents one standard deviation above the consensus price target of $167.89. This valuation is based on what can be assumed as the expectations of Vistra's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $232.0, and the most bearish reporting a price target of just $56.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $27.4 billion, earnings will come to $3.3 billion, and it would be trading on a PE ratio of 24.2x, assuming you use a discount rate of 6.6%.

- Given the current share price of $112.69, the bullish analyst price target of $207.52 is 45.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NYSE:VST. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.