Last Update 29 Jul 26

Fair value Increased 2.53%FDX: Freight Spin And Calendar Shift Will Obscure Network 2.0 Progress

The updated analyst price target for FedEx now reflects a fair value estimate of $227.22 per share versus $221.61 previously, as analysts point to expectations for stronger revenue growth, a slightly higher profit margin, and a lower future P/E multiple in light of recent research commentary on earnings recovery, cost savings, and the Network 2.0 transition.

Analyst Commentary

Recent Street research on FedEx has been active, with a wide range of price targets and views on how the freight spin off, new reporting structure, and Network 2.0 program might affect earnings quality and valuation. For you as an investor, the key themes are how cleanly FedEx can execute through this transition and how much of that potential is already reflected in the share price.

Bullish analysts highlight the earnings recovery thesis in transportation and logistics through 2027 and point to FedEx as one of the preferred large cap stocks in that group. Several firms maintain Buy or Overweight views while adjusting models for the freight separation and the move to calendar year reporting. Many of these reports describe FedEx as working through a multi lever transformation, with attention on cost savings, margins, and capital returns.

There is also a consistent focus on the Network 2.0 integration of Express and Ground, as well as the DRIVE cost program and tighter capex oversight. Supportive commentary often links these efforts to expectations for better asset utilization, potential margin improvement, and stronger free cash flow once the new structure is fully in place. Some analysts frame near term share price weakness around earnings events as a chance to gain exposure to FedEx while these changes are still being absorbed.

On the more cautious side, several price targets have been revised and models updated to reflect the separation of FedEx Freight, calendar year guidance, and shifting segment disclosures. These reports tend to stress that the next few quarters could be complex to interpret, with moving parts in guidance, incentive compensation, seasonality, and the timing of earnings contribution from different periods.

Major firms such as JPMorgan have expressed confidence in FedEx and point to structural improvements at the core parcel business, along with what they view as attractive risk or reward into and after the freight separation. At the same time, other large houses like Morgan Stanley flag that the concurrent spin, fiscal year change, and evolving disclosures may keep long term debates about margins and growth in focus for some time.

For you as a FedEx shareholder or prospective investor, this mix of optimism and caution translates into a few practical questions. How quickly can FedEx prove out its Network 2.0 and DRIVE targets in the reported numbers? How easily can the market track earnings trends through the shift to calendar reporting and new segment structure? And how much room is left between current pricing and the wide spread of Street targets that run from around US$160 to the mid US$400s?

Bearish Takeaways

- Bearish analysts have cut FedEx price targets in several cases, in some instances from levels above US$400 down toward the low US$300s, which signals concern that prior valuation assumptions may have been too optimistic relative to execution risk.

- The freight spin off and shift to a calendar year make comparisons more complex for the next few quarters. Cautious research notes flag that this added noise can make it harder to assess underlying earnings trends and may justify lower valuation multiples until the picture is clearer.

- Some bearish analysts highlight ongoing margin pressure and cost headwinds, and they expect earnings in upcoming quarters to line up closer to or below prior consensus. That view points to risk that profit improvement could take longer to show through than more optimistic forecasts suggest.

- Where models are being reset for the standalone parcel business, a few analysts describe the transition period as having many moving parts. That adds uncertainty around the growth profile FedEx can deliver post spin, which can weigh on how much investors are willing to pay for the stock today.

What’s in the News for FedEx

- FedEx announced 2026 peak season surcharges that are higher for several services, with the largest fee changes focused on Ground Residential and Ground Economy. These adjustments are intended to manage holiday volume and operating costs. Source: recent news reports.

- FedEx completed the spin off of FedEx Freight on June 1, 2026, creating two independent publicly traded companies that focus on different transportation markets. FedEx Freight began trading separately and was added to the S&P 500, while the remaining FedEx operations now center on parcel delivery, express logistics, and ground services that account for over 95% of revenue. Source: recent news reports.

- In its Q4 2026 period, the newly independent FedEx Freight reported operating income that was down 66.9% due to US$205 million in spin off related charges, volume declines, higher labor expenses, and weaker shipment volumes. Revenue was US$2.4b, supported by heavier shipments and fuel surcharges. Source: recent news reports.

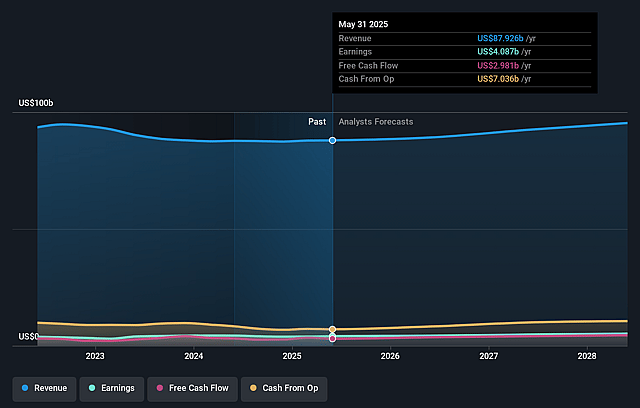

- FedEx issued 2026 guidance that calls for revenue growth of about 11% year on year and diluted EPS from continuing operations of US$16.55 to US$17.75 per share, with additional accounting adjustments related to retirement plans and the FedEx Freight spin off dividend. Source: company guidance.

- The FedEx board declared a quarterly dividend of US$1.22 per share, payable July 7, 2026, and approved a 5% increase in the annual dividend rate after a one time adjustment tied to the Freight spin off. The stated annualized dividend rate for the transition period from June 1, 2026 to December 31, 2026 is US$4.88. Source: company dividend announcement.

Valuation Changes for FedEx

- The fair value estimate has risen modestly, moving from $221.61 to $227.22 per share.

- The discount rate is slightly higher at 8.88% compared with 8.81% previously, reflecting a small change in the assumed cost of capital for FedEx.

- The revenue growth assumption now uses an updated long-term rate of 31.36% versus 27.33% in the prior model.

- The net profit margin has edged up from 5.38% to 5.40%, indicating a very small change in expected profitability on revenue.

- The future P/E has been reduced from 14.21x to 13.51x, pointing to a slightly lower valuation multiple applied to FedEx earnings in the updated framework.

Key Takeaways

- Structural declines in parcel volumes, rising labor and environmental costs, and intensifying price competition threaten long-term revenue growth and margin sustainability.

- Underperformance in international markets and challenges from e-commerce giants could significantly limit global expansion and erode pricing power.

- Structural cost reductions, e-commerce parcel growth, market share gains, and disciplined capital allocation position FedEx for stronger margins, earnings, and shareholder value.

Catalysts

About FedEx- Provides transportation, e-commerce, and business services in the United States and internationally.

- The rapid acceleration of digitalization and automation across key industries is likely to reduce the overall need for physical shipments, as virtual goods and services increasingly replace physical ones. This structural change could lead to steadily declining parcel volumes over time, putting sustained pressure on FedEx's long-term revenue growth.

- Mounting regulatory pressure related to decarbonization-including stricter environmental standards and emissions targets-is expected to drive a substantial increase in operational costs and capital expenditures for FedEx. Investments required to upgrade fleets, implement carbon-efficient logistics, and comply with global regulations threaten to erode net margins and depress future earnings.

- Persistent labor cost inflation, ongoing unionization risks, and associated wage pressures-highlighted by the company's own acknowledgment that wage inflation is not going away-are likely to further compress net margins. FedEx's heavy reliance on a large, distributed workforce makes it especially vulnerable to these long-term cost increases.

- FedEx continues to underperform international competitors in critical overseas markets, with ongoing challenges in Asia and Europe. This trend, combined with the onshoring and reshoring of supply chains that cut into lucrative international long-haul business, is poised to limit future global revenue growth and overall margin expansion even as domestic diversification efforts face intensifying cost headwinds.

- The ongoing rise of integrated e-commerce giants like Amazon, low-cost regional carriers, and disintermediation by shippers building their own logistics networks will likely intensify price competition and reduce industry-wide yields. This will structurally challenge both FedEx's pricing power and its ability to sustain volume growth, putting further downward pressure on future earnings and returns.

FedEx Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on FedEx compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming FedEx's revenue will remain fairly flat over the next 3 years.

- The bearish analysts assume that profit margins will increase from 4.7% today to 5.4% in 3 years time.

- The bearish analysts expect earnings to reach $5.2 billion (and earnings per share of $23.13) by about July 2029, up from $4.4 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $5.8 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 13.5x on those 2029 earnings, down from 16.7x today. This future PE is lower than the current PE for the US Logistics industry at 16.7x.

- The bearish analysts expect the number of shares outstanding to grow by 0.27% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.88%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- FedEx's ongoing DRIVE initiative and network transformation projects such as Network 2.0 and Tricolor are systematically reducing its structural costs, which can lead to higher operating margins and improved earnings even in a challenging demand environment.

- The company is experiencing steady parcel volume growth driven by e-commerce and deferred services, with initiatives like expanded Sunday residential coverage and wins in high-margin verticals (e.g., health care), supporting potential long-term revenue growth.

- FedEx is gaining market share in both U.S. and international parcel and airfreight segments, aided by strong service levels, productive sales strategies targeting small, medium, and bundled customers, and share gains in Europe despite a weak economic climate; these trends can lead to higher revenues and robust earnings once the macro environment improves.

- The modernization and optimization of FedEx's air fleet, including the acquisition of fuel-efficient Boeing 777s and retirement of older MD-11s, are expected to improve asset utilization and manage capital expenditures efficiently, supporting free cash flow and return on invested capital.

- Strategic capital allocation, disciplined cost management, and substantial share repurchases-alongside the anticipated benefits of the tax-efficient Freight spin-off-are likely to increase shareholder value through enhanced earnings per share and higher returns, even amid flat or moderate revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for FedEx is $227.22, which represents up to two standard deviations below the consensus price target of $351.83. This valuation is based on what can be assumed as the expectations of FedEx's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $479.0, and the most bearish reporting a price target of just $160.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $95.6 billion, earnings will come to $5.2 billion, and it would be trading on a PE ratio of 13.5x, assuming you use a discount rate of 8.9%.

- Given the current share price of $312.64, the analyst price target of $227.22 is 37.6% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on FedEx?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.