Last Update 16 Apr 26

Fair value Increased 31%FDX: Freight Spin Off And Cost Actions Will Support Long Term Earnings

FedEx's analyst fair value estimate has been revised to $479 from $365. Analysts point to updated assumptions for revenue growth, profit margins, and future P/E as key drivers behind the higher price target range seen across recent research.

Analyst Commentary

Recent Street research on FedEx shows a cluster of higher price targets and upgrades, alongside a few valuation driven downgrades. For you as an investor, the key theme is that many bullish analysts are revisiting their models around revenue, margins, and the freight spin off, and using those assumptions to justify higher fair value estimates.

Several banks with broad followings, including JPMorgan, Goldman Sachs, Barclays and UBS, have issued research that lifts their FedEx price targets or moves ratings higher. At the same time, some firms are flagging valuation as a constraint, especially after a run of earnings growth and ahead of expected earnings pressure in specific quarters.

Overall, the Street debate today is less about whether FedEx can execute on its plan and more about what investors should pay for that execution through the cycle.

Bullish Takeaways

- Bullish analysts are pushing price targets higher, in some cases by double digit dollar amounts, as they update models for FedEx's freight spin off, cost actions and a refreshed earnings outlook, which feeds directly into higher valuation ranges.

- Research that labels FedEx as a "core HALO exposure" highlights the value of its physical transportation network. Its long lived infrastructure is described as hard to replicate, which some investors may view as support for premium P/E assumptions versus more asset light peers.

- Several bullish reports frame FedEx as having clearer medium term visibility on revenue and profitability. They point to Investor Day targets and updated EPS estimates as evidence that the company is executing against a defined plan rather than relying solely on macro conditions.

- Upgrades and higher targets from major firms such as JPMorgan, UBS and others indicate that a meaningful portion of the Street is comfortable underwriting FedEx's multi year roadmap. That roadmap includes expectations for revenue growth and margin improvement that underpin higher fair value estimates.

What's in the News

- FedEx filed a lawsuit in the U.S. Court of International Trade seeking refunds of duties tied to former U.S. tariffs after a Supreme Court ruling found the levies illegal, putting potential tariff recoveries in focus for the company (Reuters).

- L'Oreal, Bausch + Lomb and Dyson filed suits seeking refunds of tariffs that were ruled unlawful, and FedEx also submitted a complaint, tying the company into a broader wave of importers pursuing duty refunds (Reuters).

- FedEx plans to return its MD 11 jets to service by May 31, which keeps its wide body air capacity in play for global express and freight customers (Reuters).

- Amazon plans to use the U.S. Postal Service for more than 1b packages per year, which could influence longer term parcel volume mix among UPS, FedEx and USPS for certain delivery lanes (Reuters).

- The U.S. Postal Service is imposing an 8% fuel surcharge on packages, a move that could shift relative price competitiveness across major parcel carriers as shippers reassess all in delivery costs (WSJ).

Valuation Changes

- Fair Value: Raised from $365.00 to $479.00, a step up of about 31%, reflecting updated modeling inputs.

- Discount Rate: Trimmed slightly from 8.82% to 8.66%, which modestly lifts the present value of projected cash flows.

- Revenue Growth: Assumed long term rate adjusted from 5.72% to 6.01%, a small increase in expected top line expansion.

- Net Profit Margin: Assumption increased from 5.25% to 6.40%, indicating a higher modeled share of $ revenue dropping to the bottom line.

- Future P/E: Target multiple moved from 18.69x to 20.60x, indicating a higher valuation placed on FedEx's modeled earnings stream.

Key Takeaways

- Operational cost optimization initiatives and technology-driven efficiencies are expected to structurally improve margins and earnings leverage as demand rebounds.

- Strong positioning in healthcare logistics and global e-commerce enhances revenue growth potential and pricing power amid evolving cross-border trade dynamics.

- Structural cost pressures, changing customer preferences, and macroeconomic headwinds threaten FedEx's revenue quality, operating margins, and future growth prospects.

Catalysts

About FedEx- Provides transportation, e-commerce, and business services in the United States and internationally.

- While analysts broadly agree that the DRIVE initiative will deliver $4 billion in cost savings and materially improve net margins, the rapid institutionalization of DRIVE as a permanent operational discipline could unlock cost efficiencies well beyond targets, structurally lowering FedEx's cost base and enabling significantly higher margin expansion and earnings leverage once volume rebounds.

- Analyst consensus appreciates Network 2.0's projected 12 percent optimized volume flow in FY '25, but with 40 percent of global daily volume targeted for optimized facilities by the end of FY '26 and continuous process learning, the resulting productivity gains and asset utilization efficiencies could support sustained double-digit operating income growth as volumes recover, far exceeding consensus estimates.

- FedEx's surging momentum in high-margin healthcare logistics-demonstrated by the onboarding of nearly $400 million in new annualized revenue and deployment of proprietary AI-driven visibility solutions-positions the company to capitalize on secular growth in healthcare and life sciences shipping, offering robust incremental revenue and margin upside.

- The expansion of flexible, technology-enabled global infrastructure, together with Sunday residential delivery now reaching two-thirds of the U.S. population, places FedEx in an unrivaled position to capture disproportionate share from accelerating e-commerce and urban middle-class growth internationally, driving long-term volume and pricing power.

- FedEx's real-time, proprietary global data infrastructure and automated customs capabilities uniquely equip it to navigate increasingly complex cross-border trade environments and regulatory shifts, making it the partner of choice as new trade corridors and e-commerce flows emerge-supporting both customer retention and premium yield expansion.

FedEx Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on FedEx compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

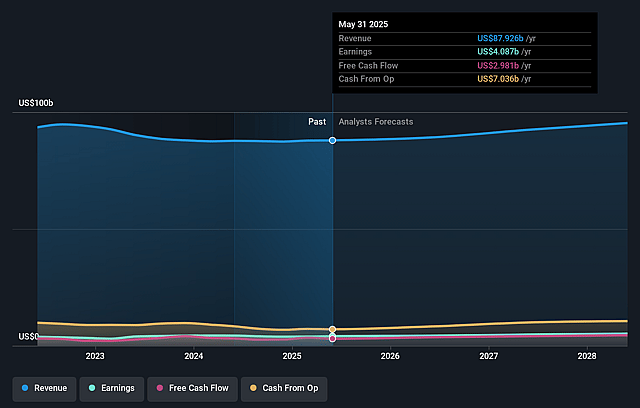

- The bullish analysts are assuming FedEx's revenue will grow by 6.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 4.9% today to 6.4% in 3 years time.

- The bullish analysts expect earnings to reach $7.0 billion (and earnings per share of $29.71) by about April 2029, up from $4.5 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $5.9 billion.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 20.7x on those 2029 earnings, up from 19.4x today. This future PE is greater than the current PE for the US Logistics industry at 15.7x.

- The bullish analysts expect the number of shares outstanding to decline by 0.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.66%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent weakness and uncertainty in the industrial economy, particularly in B2B segments, is weighing on FedEx's higher-margin freight volumes and resulting in flat to declining revenue guidance for fiscal year 2025, which could further compress operating income if global industrial activity does not recover.

- Ongoing and higher-than-expected inflationary pressures, especially in labor and operational costs, are proving difficult to fully offset and are a structural challenge; this risk could continue to erode net margins and limit future earnings growth even as cost-cutting programs like DRIVE progress.

- The shift in customer demand to lower-yielding, deferred service offerings and volume growth in lower-margin products is placing downward pressure on average yields and increasing the risk that overall revenue quality is diluted, potentially impacting both revenue and earnings.

- The acceleration of digitalization and customer adoption of remote work may limit the long-term growth of commercial shipping volumes, eroding a core revenue base and putting future top-line growth at risk if e-commerce and new verticals do not fully compensate.

- Global trade uncertainty, supply chain re-localization, and impending regulatory changes such as those related to de minimis shipments and environmental sustainability could increase compliance costs and reduce cross-border shipping activity, leading to lower international revenue and higher expenses.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for FedEx is $479.0, which represents up to two standard deviations above the consensus price target of $403.07. This valuation is based on what can be assumed as the expectations of FedEx's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $479.0, and the most bearish reporting a price target of just $230.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $109.5 billion, earnings will come to $7.0 billion, and it would be trading on a PE ratio of 20.7x, assuming you use a discount rate of 8.7%.

- Given the current share price of $364.92, the analyst price target of $479.0 is 23.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on FedEx?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.