Key Takeaways

- Focus on AI networking and proprietary EOS software is expected to drive revenue and enhance margins.

- Global expansion and subscription services are likely to diversify revenue and stabilize earnings.

- Dependency on major clients like Microsoft and Meta, alongside reliance on NVIDIA GPUs, raises significant revenue stability and growth risks due to potential purchasing reductions and deployment delays.

Catalysts

About Arista Networks- Engages in the development, marketing, and sale of data-driven, client to cloud networking solutions for AI, data center, campus, and routing environments in the Americas, Europe, the Middle East, Africa, and the Asia-Pacific.

- Arista's future growth is expected to be fueled by their expanded focus on AI networking, particularly targeting $1.5 billion in AI revenue by 2025, which is expected to positively impact their total revenue growth.

- The company is leveraging its proprietary EOS software on both cloud and AI applications, enhancing differentiation and possibly increasing net margins due to the value-added capabilities of the software.

- Arista's continued global expansion and investment in emerging markets like AI centers are expected to contribute to revenue growth, with a greater international revenue contribution and a goal of reaching $10 billion in revenue.

- The increased adoption of subscription-based network services like CloudVision is diversifying revenue streams and could lead to stability in earnings and increased profit margins over time.

- Arista is actively pursuing strategic buybacks with significant remaining authorization, which could lead to an increased earnings per share and thus enhancing shareholder value.

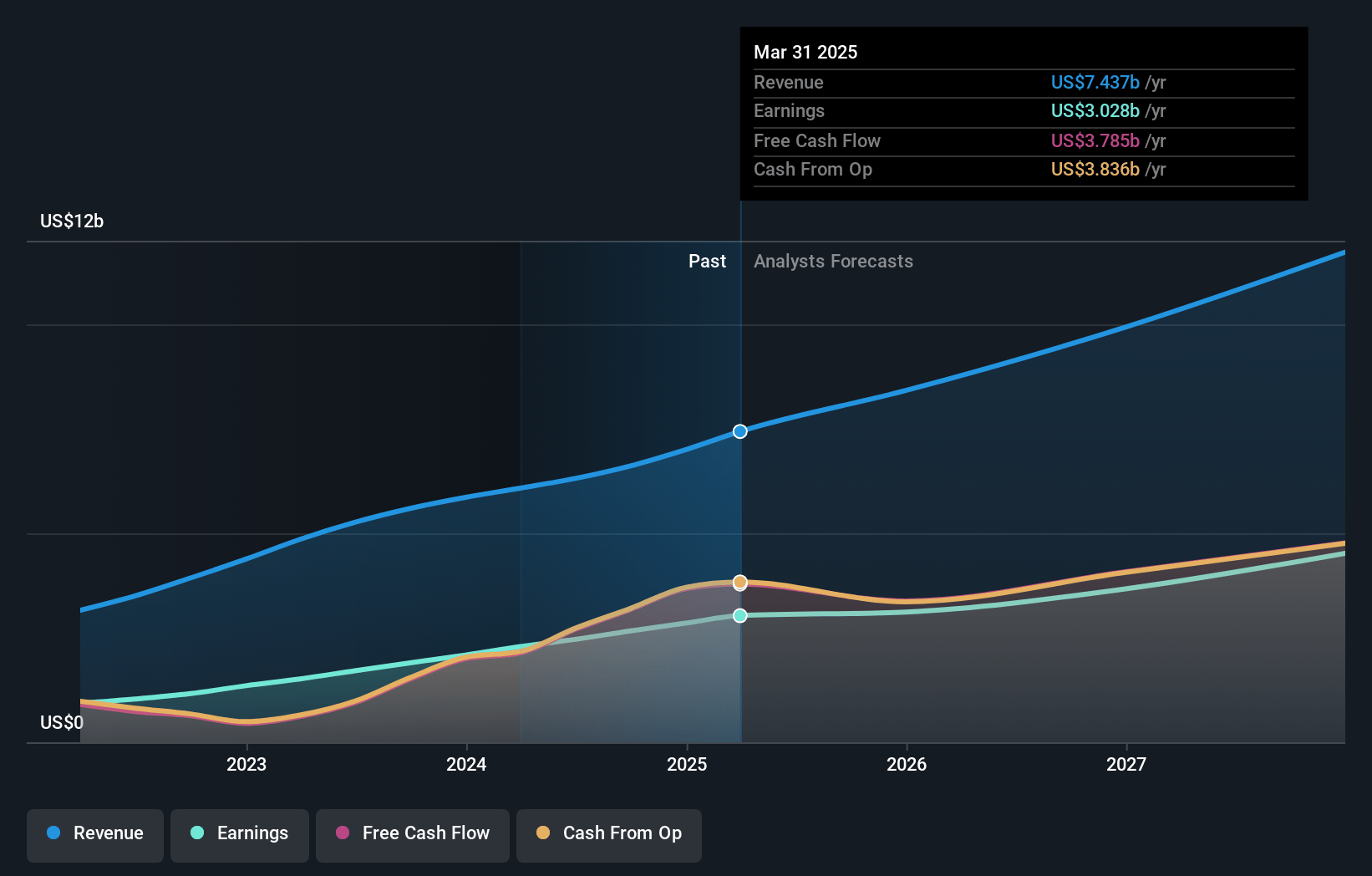

Arista Networks Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Arista Networks compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Arista Networks's revenue will grow by 26.9% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 40.7% today to 38.5% in 3 years time.

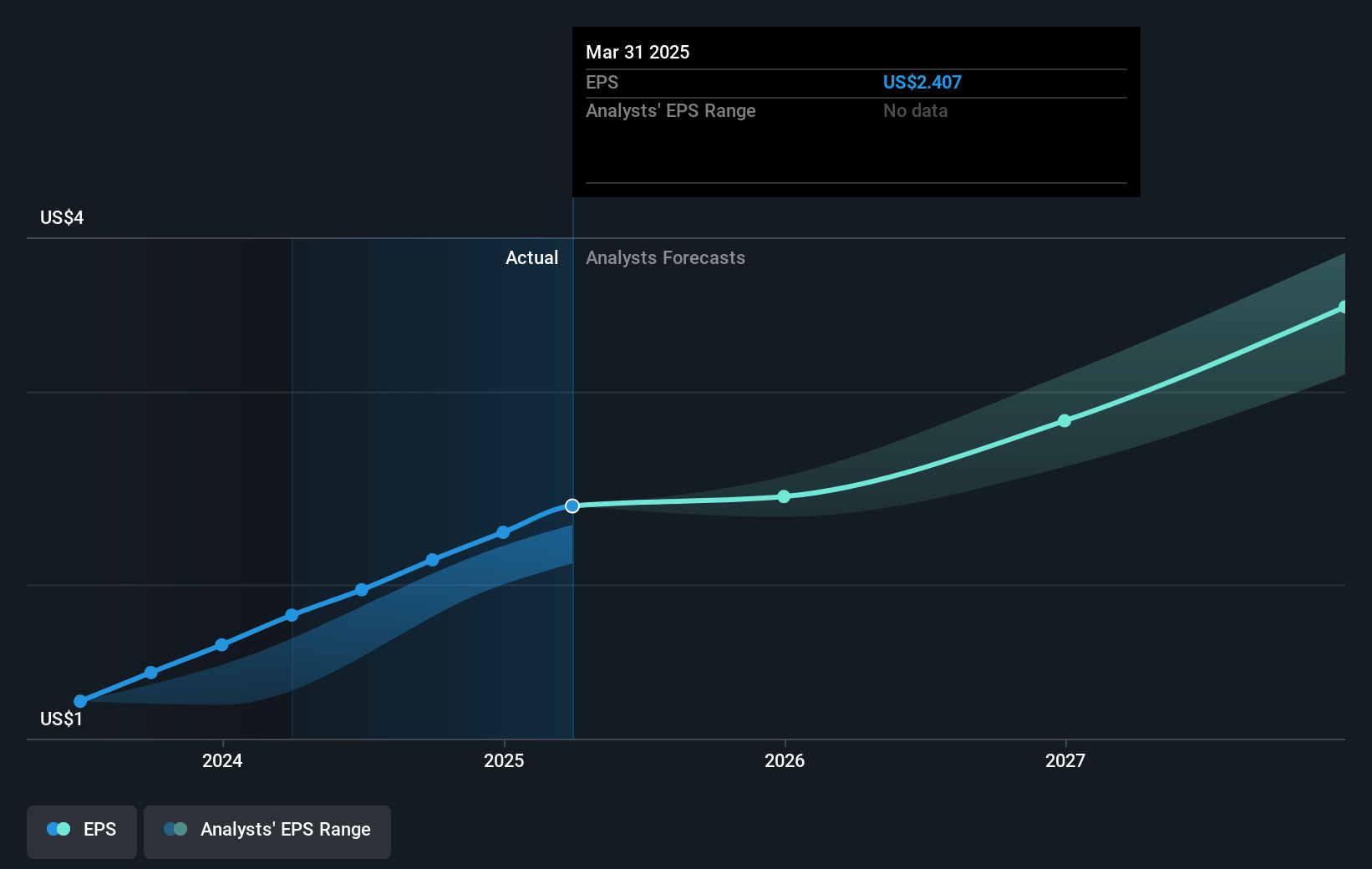

- The bullish analysts expect earnings to reach $5.5 billion (and earnings per share of $4.05) by about April 2028, up from $2.9 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 36.9x on those 2028 earnings, up from 32.4x today. This future PE is greater than the current PE for the US Communications industry at 24.8x.

- Analysts expect the number of shares outstanding to grow by 0.61% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.9%, as per the Simply Wall St company report.

Arista Networks Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Concerns are raised regarding the dependency on a few major customers like Microsoft and Meta, as they account for a significant portion of the revenue, which could pose risks to revenue stability if these clients reduce their purchasing.

- A portion of the company’s competitive advantage is reliant on continued product innovation and maintaining a differentiated network software and services offering, which if competitors catch up, could pressure future earnings.

- The evolving regulatory and tariff situation, particularly related to China, is a source of potential cost increase, which might adversely impact gross margins.

- The dependency on NVIDIA GPUs and potential delays or changes in GPU deliveries could impact the timely deployment of AI clusters, thereby affecting revenue projections from the AI segment.

- The impact of foreign currency fluctuations and limited international revenue growth, as indicated by a decrease in international revenue contributions, could affect net margins and overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Arista Networks is $129.49, which represents one standard deviation above the consensus price target of $108.0. This valuation is based on what can be assumed as the expectations of Arista Networks's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $145.0, and the most bearish reporting a price target of just $73.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $14.3 billion, earnings will come to $5.5 billion, and it would be trading on a PE ratio of 36.9x, assuming you use a discount rate of 6.9%.

- Given the current share price of $73.2, the bullish analyst price target of $129.49 is 43.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NYSE:ANET. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives