Key Takeaways

- Strategic AI partnerships and innovative products are driving revenue growth and strengthening net margins through operational efficiencies and market expansion.

- Emphasis on subscription services and improved supply chain management enhances earnings predictability and boosts operating margins.

- Supply chain issues, risky expansion, customer concentration, tariffs, and rising expenses pose challenges to Arista Networks' revenue growth and profit margins.

Catalysts

About Arista Networks- Engages in the development, marketing, and sale of data-driven, client to cloud networking solutions for AI, data center, campus, and routing environments in the Americas, Europe, the Middle East, Africa, and the Asia-Pacific.

- Arista Networks is successfully leveraging the momentum of generative AI, contributing nearly 20% annual revenue growth in 2024, surpassing their initial guidance. This AI-driven acceleration is expected to continue, positively impacting future revenue, aiming for $1.5 billion in AI centers in 2025.

- Arista is broadening its product innovation, emphasizing its extensible OS stack and enhanced Ethernet speeds, which garnered them over 40% market share in high-performance switching deployments. This expansion into advanced products is likely to influence net margins positively due to increased operational efficiencies.

- The company's strategic partnerships with large cloud and AI titans, such as Microsoft and Meta, continue to drive significant portions of revenue. With these partners driving demand for data-centric networking solutions, Arista anticipates substantial earnings growth from these high-volume customers.

- Arista's growth in subscription-based services and network software, such as CloudVision and Arista A-Care, is crucial as it enhances recurring revenue streams. With a robust push towards building network as a service offerings, this focus is likely to boost overall earnings predictability and stability.

- Investment in next-generation networking solutions and expanding customer reach through improved supply chain and inventory management indicates better working capital optimization. These operational improvements are expected to foster increased operating margins as the company scales its business in 2025.

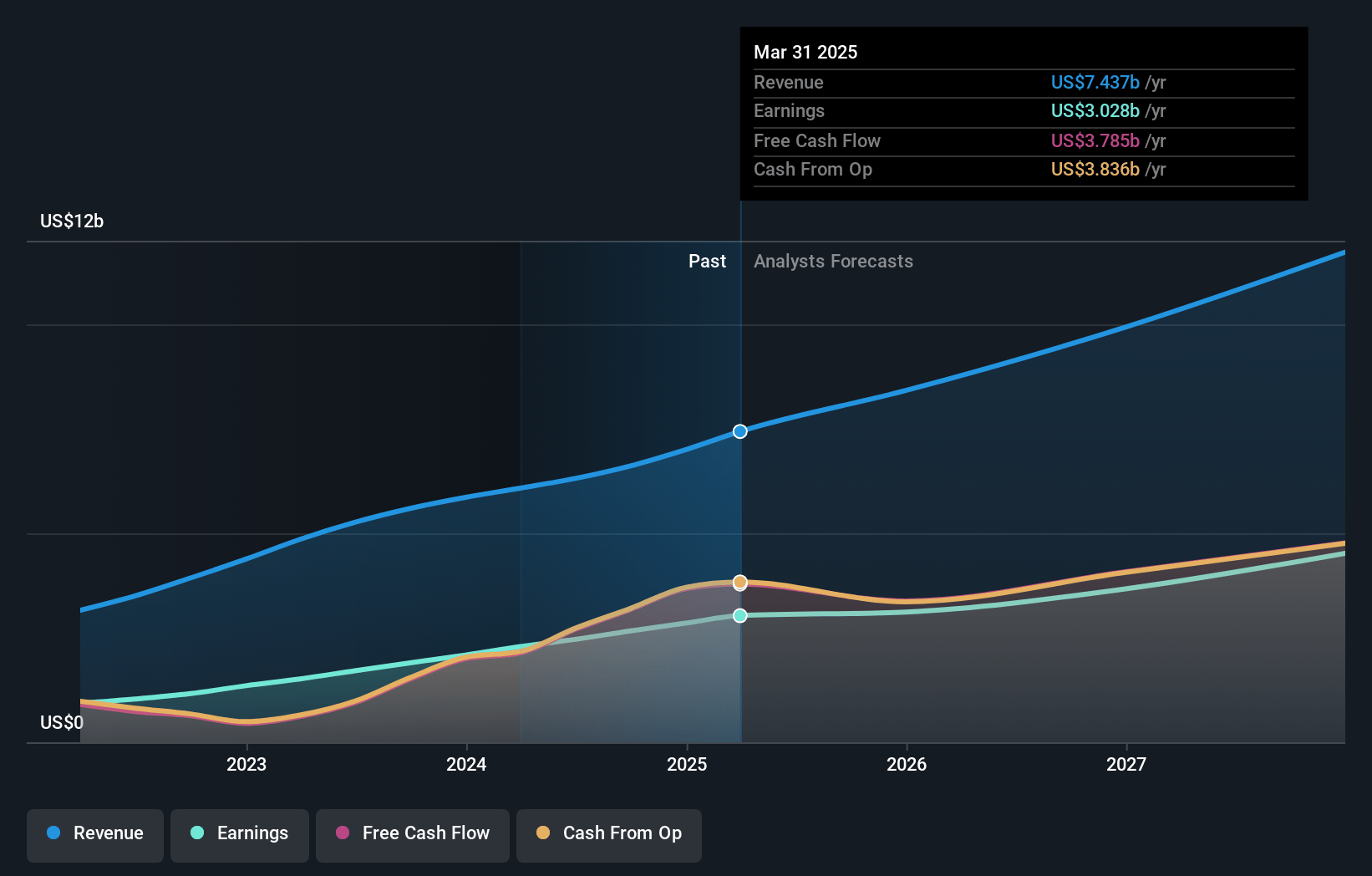

Arista Networks Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Arista Networks's revenue will grow by 19.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 40.7% today to 38.7% in 3 years time.

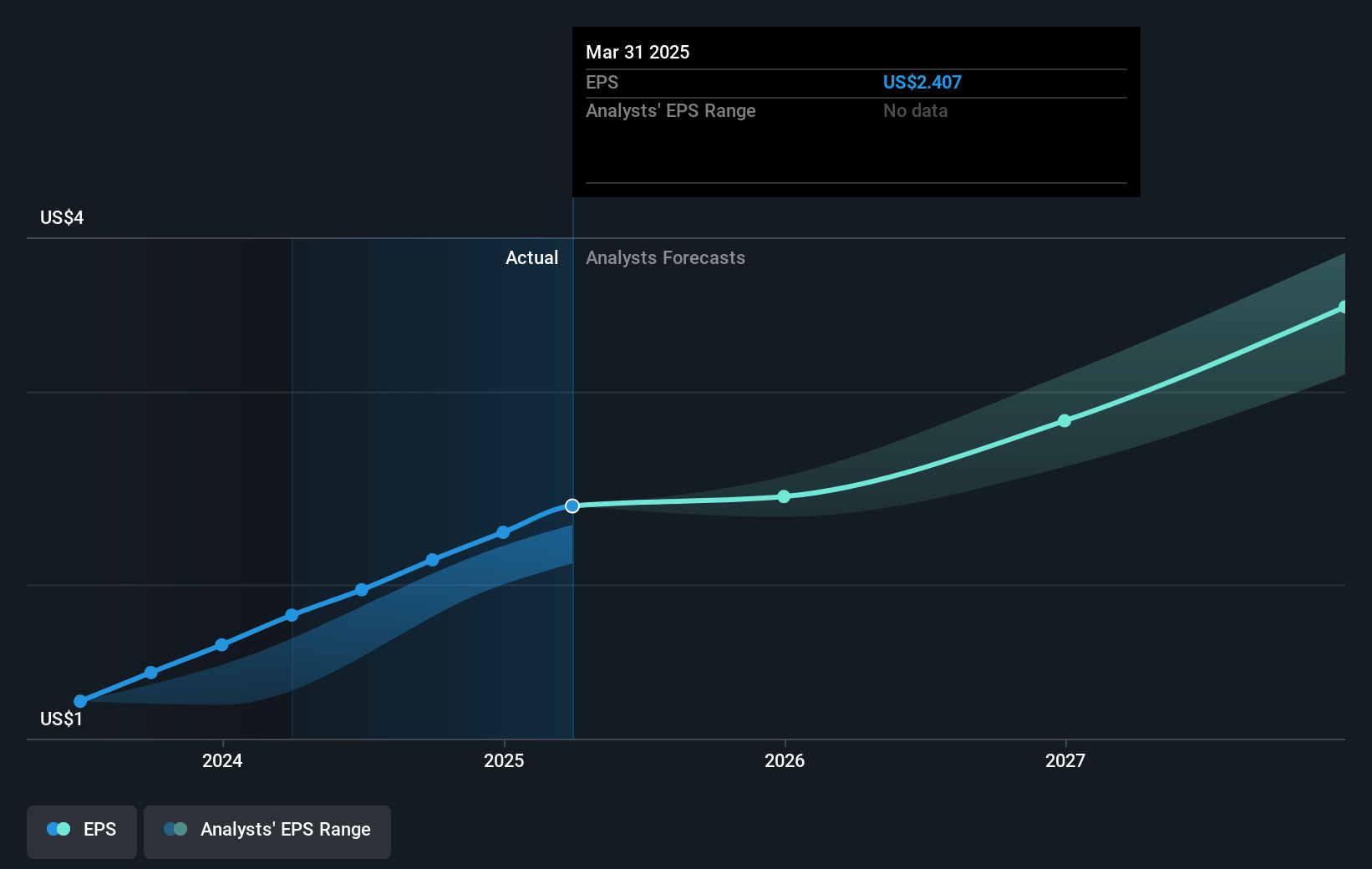

- Analysts expect earnings to reach $4.6 billion (and earnings per share of $3.46) by about March 2028, up from $2.9 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $5.5 billion in earnings, and the most bearish expecting $3.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.3x on those 2028 earnings, up from 38.4x today. This future PE is greater than the current PE for the US Communications industry at 26.4x.

- Analysts expect the number of shares outstanding to grow by 0.61% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.7%, as per the Simply Wall St company report.

Arista Networks Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Supply chain constraints and component costs remain a concern, potentially impacting Arista Networks' ability to meet customer demands and thereby affecting revenue growth and profit margins.

- Arista's expansion plans are risky due to the dynamic market environment, which could lead to execution challenges in achieving its projected revenue and earnings.

- The reliance on a few major customers like Microsoft and Meta represents a concentration risk. Any changes in these customers' capital expenditure plans could directly impact Arista's revenues.

- The pressure from tariffs on Chinese imports might affect the company's gross margins, given that some costs are being absorbed to maintain customer relationships.

- Increased R&D spending and other operational expenses could pressure net margins if they do not translate into proportionate revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $116.172 for Arista Networks based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $145.0, and the most bearish reporting a price target of just $80.75.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $11.9 billion, earnings will come to $4.6 billion, and it would be trading on a PE ratio of 39.3x, assuming you use a discount rate of 6.7%.

- Given the current share price of $86.94, the analyst price target of $116.17 is 25.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives