Key Takeaways

- Arista's growth strategy focuses on AI, cloud partnerships, and cognitive enterprise networking, enhancing revenue via high-margin solutions and market share expansion.

- Shifting to subscription-based services like CloudVision boosts recurring revenue, stabilizing earnings and reducing dependency on hardware sales.

- Arista Networks faces risks from supply chain constraints, customer concentration, competition, product mix shifts, and ambitious growth targets impacting revenue and profitability.

Catalysts

About Arista Networks- Engages in the development, marketing, and sale of data-driven, client to cloud networking solutions for AI, data center, campus, and routing environments in the Americas, Europe, the Middle East, Africa, and the Asia-Pacific.

- Arista Networks anticipates growth in AI network infrastructure, particularly with the emergence of 800-gigabit Ethernet for AI back-end clusters, projected to significantly contribute to their AI revenue goal of $1.5 billion in 2025. This impacts future revenue growth as new technology adoption drives increased sales.

- The company plans to leverage its strong position in AI and data centers by increasing market share in the AI and cloud sectors through engineered collaborations with partners like Microsoft and Meta. This strategic focus could enhance operating margins by capitalizing on high-margin partnerships and innovative engineering solutions.

- Arista is expanding its cognitive enterprise networking, including routing and SD-WAN, indicating an expected significant increase in revenue from these adjacencies, estimated to exceed $1 billion in 2025. Successful execution in these areas is likely to improve net margins by capturing a larger share of the Global 2000 market.

- The shift toward subscription-based network software and services, such as CloudVision, is anticipated to provide a steady growth in recurring revenue, representing 17% of total revenue in 2024. This shift could stabilize earnings by reducing dependency on hardware sales and increasing the predictability of future cash flows.

- Arista's strategic investment in hybrid cloud networking and sovereign AI opportunities indicates potential growth areas where specialized cloud providers and AI services could expand Arista's addressable market. This expansion is poised to impact revenue positively by diversifying and broadening Arista's customer base in 2025 and beyond.

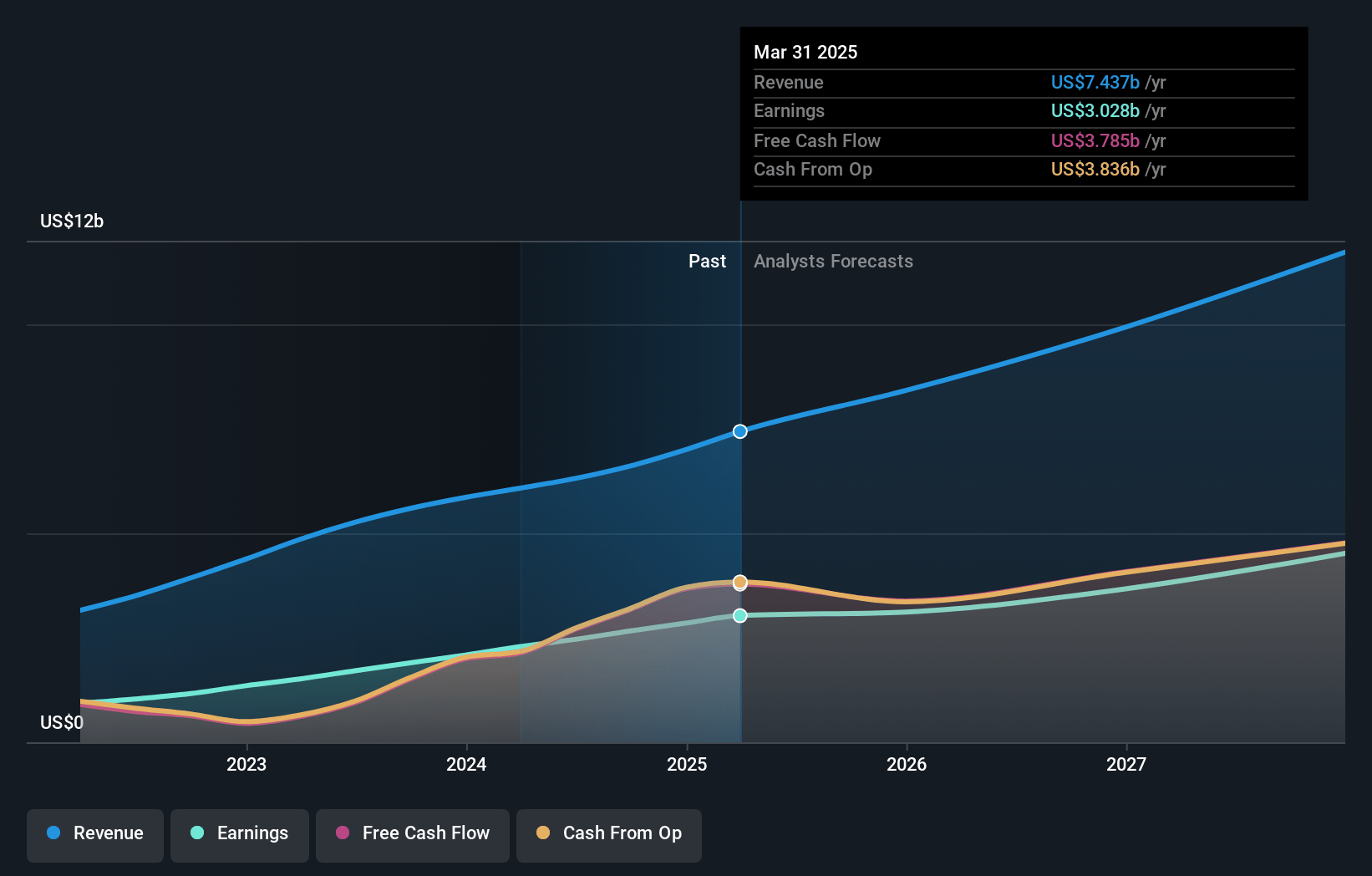

Arista Networks Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Arista Networks compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Arista Networks's revenue will grow by 13.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 40.7% today to 37.2% in 3 years time.

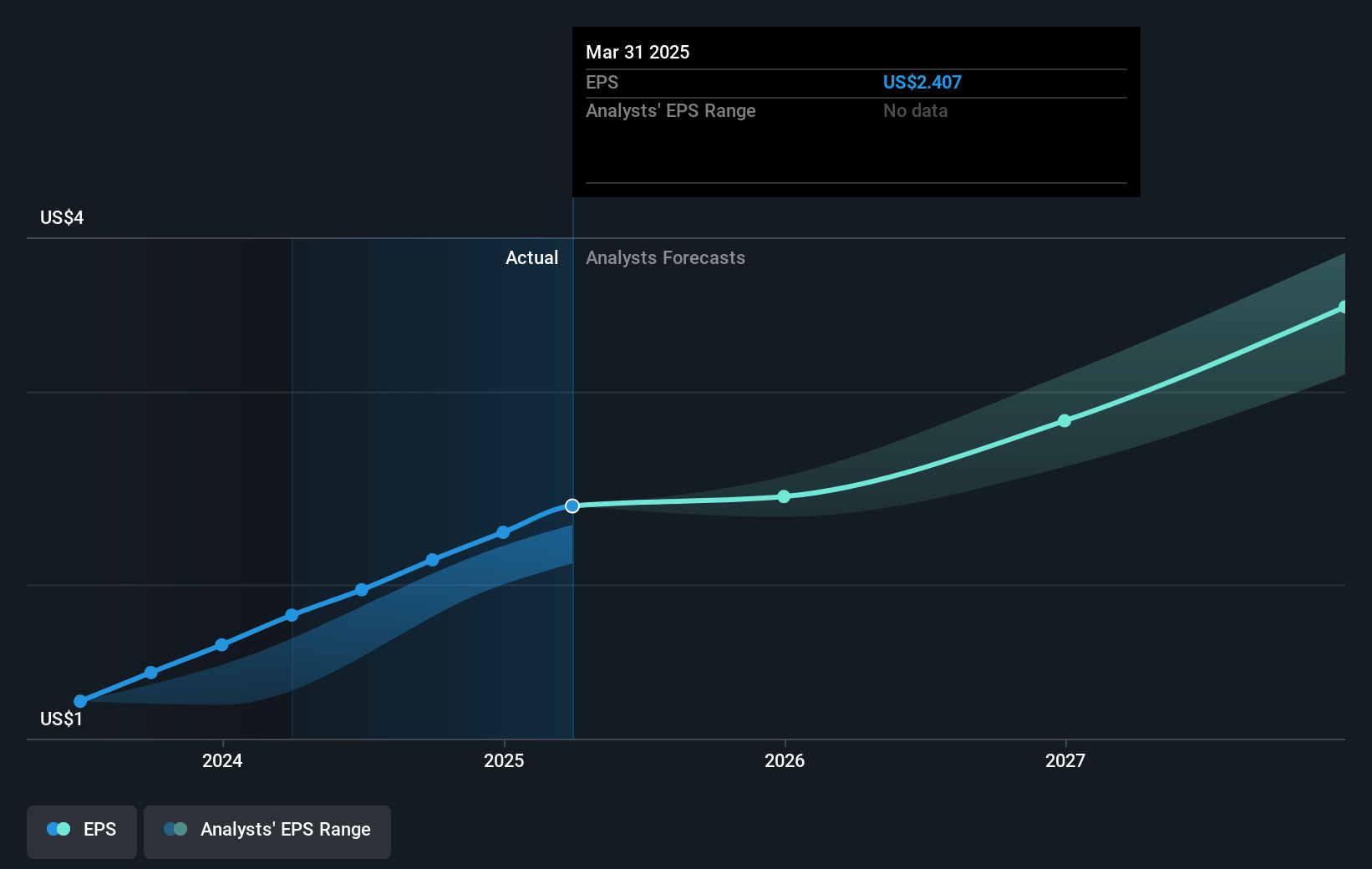

- The bearish analysts expect earnings to reach $3.9 billion (and earnings per share of $2.98) by about April 2028, up from $2.9 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 36.4x on those 2028 earnings, up from 33.6x today. This future PE is greater than the current PE for the US Communications industry at 23.0x.

- Analysts expect the number of shares outstanding to grow by 0.61% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.89%, as per the Simply Wall St company report.

Arista Networks Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Supply chain constraints and component costs, as highlighted in the earnings conference call, pose risks to future revenue and profitability due to potential disruptions or increased expenses.

- The company's reliance on a few concentrated customers, such as Microsoft and Meta, who represent significant portions of revenue, could impact earnings if these relationships are weakened or if their spending priorities change.

- Increased competition from white box vendors and other OEMs, particularly in AI networking, might pressure revenue growth and market share in both the front-end and back-end network solutions.

- Arista's gross margins could be affected by a shift in product mix, including a higher concentration of sales to Cloud Titans, and tariffs on China that the company is currently absorbing on behalf of customers.

- The company's aggressive growth targets, while ambitious, carry execution risks and uncertainties regarding AI cluster rollouts and customer adoption of new technologies, potentially impacting future revenue and earnings growth rates.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Arista Networks is $89.39, which represents one standard deviation below the consensus price target of $111.26. This valuation is based on what can be assumed as the expectations of Arista Networks's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $145.0, and the most bearish reporting a price target of just $73.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $10.4 billion, earnings will come to $3.9 billion, and it would be trading on a PE ratio of 36.4x, assuming you use a discount rate of 6.9%.

- Given the current share price of $76.0, the bearish analyst price target of $89.39 is 15.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NYSE:ANET. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.