Last Update 15 Jun 26

ZBRA: Raised Guidance And Short Cycle Demand Inflection Should Drive Future Upside

Analyst Commentary

Bullish analysts have been responding to Zebra Technologies' Q1 update and guidance changes with a series of target revisions and rating moves that point to improving confidence in the company's execution.

Several firms have refreshed their models around the stock, citing better than feared memory trends, an improving short cycle demand backdrop, and management guidance that came in ahead of prior expectations despite ongoing cost headwinds.

Recent research also reflects a shift in tone compared with earlier periods when some targets were being revised lower, suggesting that the latest quarter and outlook have addressed key concerns for a portion of the Street.

Bullish Takeaways

- Bullish analysts have raised price targets into a US$284 to US$345 range, tying the changes to updated models after Q1 results and a view that the stock better reflects the company's current execution and demand backdrop.

- One group of bullish analysts views the Q1 print and guidance raise as evidence of improving demand and better execution, with management updates giving them more confidence in how Zebra is running the business.

- Another bullish research view is that Zebra cleared a major hurdle with Q2 guidance coming in above prior Street expectations, even while memory costs remain a headwind, which they see as supportive for valuation.

- Upgrades to Overweight from prior neutral stances are being framed around early signs of an inflection in short-cycle industrial demand, improving cost execution, and a track record of conservative guidance that some analysts believe could set up room for consensus estimate and multiple expansion if current trends hold.

What's in the News

- Zebra launched the Zebra Nucleus platform and new Workcloud AI-powered software solutions at its ZONE 2026 customer conference in Nashville, aiming to simplify device management, unify its software ecosystem, and give IT leaders and frontline workers real-time insights to improve operational efficiency. (Source: ZONE 2026 announcements)

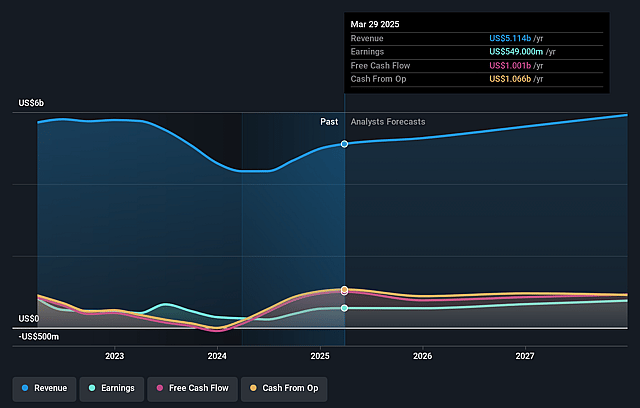

- The company reported Q1 2026 earnings and sales that were above analyst estimates and issued full year 2026 adjusted EPS guidance of US$18.30 to US$18.70, with expected net sales growth of 10% to 14%, and Q2 net sales growth guidance of 14% to 17%. (Source: Q1 2026 results and guidance)

- Zebra is emphasizing a shift in mix toward higher value software, analytics, and service offerings with the launch of Zebra Nucleus and Workcloud Business Intelligence dashboards, while still retaining exposure to hardware driven revenue. (Source: ZONE 2026 announcements)

- Nucleus Research named Zebra Workcloud Task Management a Leader in its Task Management Value Matrix, and previously recognized Zebra Workcloud Scheduling and Timekeeping as a Leader in its Workforce Management Value Matrix, highlighting third party validation of the Workcloud suite. (Source: Nucleus Research reports)

- Zebra has been active on capital returns, repurchasing 1,083,222 shares for US$241.84m under a buyback announced in February 2026, and 3,780,315 shares for US$1.0b under a separate buyback announced in May 2022. (Source: buyback tranche updates)

Valuation Changes

- Fair Value: Modelled fair value is unchanged at $393.84.

- Discount Rate: The discount rate has risen slightly from 9.51% to 9.59%.

- Revenue Growth: The revenue growth assumption has risen slightly from 8.95% to 9.04%.

- Net Profit Margin: The net profit margin assumption has risen slightly from 14.09% to 14.14%.

- Future P/E: The future P/E multiple has edged down from 19.84x to 19.75x.

Key Takeaways

- Broad adoption of automation, real-time tracking, and workflow digitization is fueling sustained growth, improved margins, and industry outperformance as customers modernize operations.

- Regulatory pressures and workforce shortages are expanding Zebra’s market and driving demand for recurring revenue software, margin expansion, and greater operating leverage.

- Reliance on hardware amid rising automation, trade barriers, and sustainability demands threatens Zebra’s margins, recurring revenue growth, and long-term market relevance.

Catalysts

About Zebra Technologies- Provides enterprise asset intelligence solutions in the automatic identification and data capture solutions industry worldwide.

- Strong, sustained demand from the rapid growth of e-commerce and the transition to omnichannel retail is driving robust, broad-based top line growth across key verticals—including retail, logistics, and even healthcare—with Zebra’s data capture and automation offerings (barcode, mobile, RFID) positioned for further revenue acceleration as these markets continue modernizing.

- Fast-expanding needs for real-time asset tracking and supply chain visibility, amplified by the proliferation of IoT devices, are leading customers to adopt more of Zebra’s core solutions and recurring software/services, supporting higher long-term recurring revenue streams and structurally improving gross margins and earnings predictability.

- Zebra’s continuous investment in workflow digitization, AI-enabled mobile solutions, and next-generation automation (like the AI suite for mobile computing and new 3D machine vision solutions through the Photoneo acquisition) is enabling cross-selling and greater wallet share, setting the stage for revenue growth outpacing the overall industry as customers modernize their logistics and manufacturing operations.

- Secular workforce shortages and labor cost pressures are catalyzing further adoption of Zebra’s workflow optimization hardware and software, accelerating deployments in logistics, healthcare, and manufacturing, which is likely to drive margin expansion and support higher operating leverage as demand for automation and efficiency tools grows.

- Regulatory and customer-driven mandates for end-to-end supply chain transparency and traceability in industries such as food, pharmaceuticals, and global logistics are expanding the company’s total addressable market and creating additional tailwinds for recurring revenues from Zebra’s track and trace technologies—directly supporting long-term revenue growth and improved free cash flow conversion.

Zebra Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Zebra Technologies compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Zebra Technologies's revenue will grow by 9.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 7.5% today to 14.1% in 3 years time.

- The bullish analysts expect earnings to reach $1.0 billion (and earnings per share of $21.75) by about June 2029, up from $418.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $691.1 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 19.8x on those 2029 earnings, down from 26.0x today. This future PE is lower than the current PE for the US Electronic industry at 32.9x.

- The bullish analysts expect the number of shares outstanding to decline by 6.32% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.59%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The accelerating shift towards automation and AI-based tracking systems threatens the long-term relevance of Zebra’s core barcode and mobile computing solutions, which could diminish its addressable market and reduce future revenue growth.

- Ongoing and heightened global trade restrictions and tariff uncertainties have already caused increased direct costs, as indicated by the $70 million gross profit impact modeled for 2025, and could further disrupt international sales and squeeze net margins if export markets become more restricted.

- Zebra continues to derive the majority of its revenue from hardware rather than software or recurring services, making the company especially vulnerable to hardware commoditization and intensifying price competition, likely eroding gross margins and EBITDA over time.

- The slow growth in recurring software and services—evident from only slight increases in that segment this quarter—limits Zebra’s ability to transition to higher-margin, subscription-based revenue streams, putting long-term earnings per share potential at risk if this trend continues.

- New and impending e-waste regulations and sustainability mandates could lead to rising compliance and operational costs for Zebra’s hardware-centric business, potentially discouraging frequent hardware refresh cycles and negatively affecting both gross margin and top-line revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Zebra Technologies is $393.84, which represents up to two standard deviations above the consensus price target of $328.88. This valuation is based on what can be assumed as the expectations of Zebra Technologies's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $400.0, and the most bearish reporting a price target of just $267.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $7.2 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 19.8x, assuming you use a discount rate of 9.6%.

- Given the current share price of $228.42, the analyst price target of $393.84 is 42.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Zebra Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.