Last Update 29 Jun 26

Fair value Decreased 2.55%ZBRA: Automation And AI Execution Will Test Fairly Balanced Risk Reward

Zebra Technologies' analyst fair value estimate has been trimmed by $7 to $267 as analysts factor in a higher discount rate and slightly softer revenue growth assumptions. At the same time, they highlight stronger execution, improving short-cycle demand trends, and higher Street price targets following recent Q1 and Q2 updates.

Analyst Commentary

Recent Street research on Zebra Technologies shows a mixed backdrop, with some firms lifting price targets and turning more constructive on the stock following Q1 results and updated guidance. Several reports point to improving short cycle demand trends, better cost execution, and what they view as conservative management guidance as key supports for their updated models.

Some bullish analysts highlight higher price targets in the low to mid US$300s after revisiting assumptions as Q2 progresses and as memory trends are assessed. They point to Q2 guidance that came in above prior expectations despite higher memory costs, and see this as an indication of stronger execution and an ability to manage cost headwinds.

Other research notes emphasize that Zebra Technologies' Q1 quarter and guidance raise indicate an improving demand backdrop and more consistent delivery against expectations. These analysts see the company as having cleared a major hurdle with its near term outlook and, in their view, they now have more confidence in management's ability to handle anticipated memory cost pressures.

At the same time, there are signs of more cautious positioning in parts of the Street, particularly around longer term cost visibility and the durability of any pickup in short cycle industrial demand. This has led to some trims in fair value estimates and lingering questions about how much upside is already reflected in higher price targets.

Bearish Takeaways

- Bearish analysts have adjusted fair value and price targets lower in some cases, flagging uncertainty around longer term memory cost trends and the risk that these pressures could weigh on Zebra Technologies' margins if not fully offset.

- Some research commentary stresses limited visibility into future cost dynamics, suggesting that part of the potential pressure is already reflected in the stock and creating a risk that expectations move ahead of what the company can deliver.

- Where targets have been trimmed, bearish analysts are effectively signaling concern that current valuation may leave less room for execution missteps or slower than expected improvement in short cycle industrial demand.

- Cautious views also point to the possibility that consensus growth and margin assumptions could prove optimistic, which would raise the risk of estimate cuts if demand or cost control does not track as currently modeled.

What’s in the News for Zebra Technologies

- Zebra Technologies reported Q1 2026 adjusted earnings of about US$4.75 per share, with net sales above analyst estimates, and raised full year 2026 adjusted earnings guidance to US$18.30 to US$18.70 per share, alongside a 10 to 14% net sales growth forecast. (Source: recent earnings coverage)

- The company issued Q2 2026 guidance that points to net sales growth of 14 to 17% and adjusted earnings per share of US$4.20 to US$4.50, with an outlook for an improved adjusted EBITDA margin. (Source: recent earnings coverage)

- At its ZONE 2026 customer conference, Zebra Technologies expanded its software offering with new AI powered platforms, Zebra Nucleus and Workcloud Business Intelligence dashboards, focusing on device management and real time operational insights. (Source: ZONE 2026 news)

- Zebra Technologies is showcasing an expanded machine vision and automation ecosystem at Automate 2026, including the debut of the CV70 CXP high performance machine vision camera for high speed, high resolution manufacturing applications. (Source: Automate 2026 announcements)

- Despite these product launches, software investments and guidance updates, Zebra Technologies’ stock has lagged the Nasdaq Composite and has traded below its 50 day moving average since August last year. (Source: recent earnings coverage)

Valuation Changes for Zebra Technologies

- Fair Value: Trimmed slightly from $274.00 to $267.00, reflecting updated assumptions in the model.

- Discount Rate: Risen slightly from 9.04% to 9.50%, indicating a modestly higher hurdle rate applied to Zebra Technologies' cash flows.

- Revenue Growth: The assumed long term growth rate has been reduced from 6.89% to 6.34%, signaling a more cautious revenue trajectory in the forecasts.

- Net Profit Margin: Margins are now modeled a bit higher, moving from 10.09% to 10.36%, suggesting incrementally stronger profitability assumptions.

- Future P/E: The target future P/E multiple has been lowered from 23.50x to 19.65x, implying a more conservative valuation multiple for the stock.

Key Takeaways

- U.S. import tariffs and geopolitical uncertainties threaten gross profits and revenue predictability by increasing costs and compressing margins.

- Slowing manufacturing growth and competitive pressures could hinder revenue growth, particularly if planned pricing increases aren't fully realized.

- Strong sales growth and operational efficiency, alongside innovation through R&D and strategic acquisitions, position Zebra Technologies for sustainable growth despite supply chain and tariff challenges.

Catalysts

About Zebra Technologies- Provides enterprise asset intelligence solutions in the automatic identification and data capture solutions industry worldwide.

- The company is experiencing challenges from U.S. import tariffs, which are expected to have a significant negative impact on gross profits. These tariffs could reduce gross profit by $70 million for 2025, potentially compressing net margins and limiting earnings growth.

- The geopolitical landscape and trade uncertainties could lead to shifts in manufacturing locations and potentially higher costs. This shifting could impact revenue predictability and lead to reduced net profits if costs are not efficiently managed.

- There is a concern about slowing growth in manufacturing, which could lag behind other verticals. This slower growth in a key segment may lead to revenue growth below consensus expectations.

- The company has planned increased pricing to offset tariff impacts, but there is uncertainty about the full realization of these price increases due to competitive pressures. Failure to realize these increases could result in lower revenue and compressed margins.

- A potential economic downturn and changes in customer sentiment due to global trade uncertainties could lead to reduced demand and pullbacks in projects, which would negatively impact both revenue and earnings growth.

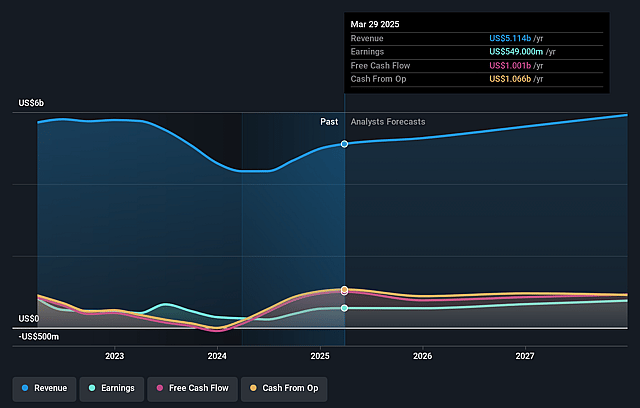

Zebra Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Zebra Technologies compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Zebra Technologies's revenue will grow by 6.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 7.5% today to 10.4% in 3 years time.

- The bearish analysts expect earnings to reach $695.7 million (and earnings per share of $14.32) by about June 2029, up from $418.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $1.0 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 19.7x on those 2029 earnings, down from 28.7x today. This future PE is lower than the current PE for the US Electronic industry at 31.2x.

- The bearish analysts expect the number of shares outstanding to decline by 6.32% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.5%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Zebra Technologies reported a strong performance in the first quarter, with sales exceeding $1.3 billion, a 12% increase compared to the prior year, which suggests robust demand across its product categories and regions, potentially driving revenue growth.

- The company achieved an adjusted EBITDA margin of 22.3%, a 240 basis point increase, indicating effective cost management and operational efficiency that could positively affect net margins.

- Zebra's ongoing efforts to diversify its supply chain outside China and its capital-light business model could help mitigate risks related to tariffs, preserving profitability and protecting earnings.

- The company's strategic focus on innovation, including significant reinvestment into research and development and strategic acquisitions like Photoneo, positions Zebra to capitalize on the trend towards digitization and automation, potentially contributing to long-term revenue and earnings growth.

- Despite tariffs, Zebra's ability to adjust pricing and its strong free cash flow generation of over $1 billion over the trailing four quarters provides flexibility to navigate uncertainties, potentially safeguarding profit margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Zebra Technologies is $267.0, which represents up to two standard deviations below the consensus price target of $328.94. This valuation is based on what can be assumed as the expectations of Zebra Technologies's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $400.0, and the most bearish reporting a price target of just $267.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $6.7 billion, earnings will come to $695.7 million, and it would be trading on a PE ratio of 19.7x, assuming you use a discount rate of 9.5%.

- Given the current share price of $251.53, the analyst price target of $267.0 is 5.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Zebra Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.