Last Update 06 Jul 26

Fair value Increased 4.45%PLXS: Secular Growth Exposure And Macro Uncertainty Will Likely Cap Further Upside

The Plexus analyst price target has been adjusted from $280.75 to $293.25. Analysts cite reaffirmed long-term growth and margin potential following recent management meetings as the key rationale for the update.

Analyst Commentary

Recent research on Plexus highlights a cluster of upward price target revisions following investor meetings with the company, with commentary focused on long term growth potential, margin prospects, and positioning in key end markets.

Bullish Takeaways

- Bullish analysts point to reaffirmed long term growth and margin goals from Plexus management as support for higher valuation ranges, reflected in multiple price target increases across recent research.

- Meetings with the CFO and COO are described as reinforcing the existing investment thesis, with analysts highlighting management confidence in execution on current plans.

- Some research notes cite Plexus positioning in end markets such as aerospace and defense, semiconductor capital equipment, and emerging data center applications as a key part of the growth story.

- Rising price targets, including levels cited at US$310 and US$330, are tied to analyst views that Plexus is well placed to pursue opportunities in several identified growth markets.

Bearish Takeaways

- Even within largely positive commentary, macro visibility is flagged as the main area of uncertainty, with analysts acknowledging that broader demand trends remain a potential constraint on Plexus execution.

- Dependence on high growth end markets such as semiconductor capital equipment and data center applications could expose Plexus to cyclical swings if customer spending slows.

- The concentration of recent research around a similar positive thesis suggests limited differentiated caution in published views, which may reduce the margin of safety if company performance or external conditions differ from expectations.

What’s in the News for Plexus

- Plexus is featured alongside Flex Ltd. in a comparison of electronics manufacturing stocks, with the article highlighting Plexus program wins across automation, advanced electronics, and AI infrastructure as key areas of focus. Source: "FLEX vs. PLXS: Which Electronics Manufacturing Stock is the Better Buy?"

- A recent analysis describes Plexus as having shifted its business model toward high complexity, regulated sectors such as aerospace, defense, and medical devices, supported by a record US$4b manufacturing funnel and 30 new programs, with Q2 revenue reported at 19% year over year growth. Source: "Plexus: A Flawless Strategic Pivot, But Priced In (NASDAQ:PLXS) | Seeking Alpha"

- Plexus and Riverside Research announced a partnership to develop reusable modular hardware and software for intelligence and defense markets, including the Aegis R52L Enhanced Retransmission Device, with the first project moving from concept to manufacturing planning in under nine months.

- Plexus reported share repurchases between January 4, 2026 and April 4, 2026, buying back 109,105 shares for US$20.64 million, and completing a total of 374,693 shares for US$58.01 million under a buyback first announced on May 14, 2025.

- The company outlined a planned CFO transition, with long time CFO Patrick Jermain set to retire and David Abuhl, currently Senior Vice President of Finance, scheduled to assume the Chief Financial Officer role on May 11, 2026, following a defined handover period.

Valuation Changes for Plexus

- Fair Value: updated from $280.75 to $293.25, a modest uplift in the modeled central value for Plexus shares.

- Discount Rate: adjusted slightly from 8.91% to 8.80%, reflecting a small change in the required return used in the valuation framework.

- Revenue Growth: held broadly stable at about 11.83%, indicating no material change in the long term top line growth assumptions for Plexus.

- Net Profit Margin: kept effectively unchanged at around 4.62%, with only a minimal numerical adjustment in the model.

- Future P/E: increased from 33.87x to 35.27x, implying a somewhat higher valuation multiple applied to Plexus forward earnings in the updated analysis.

Key Takeaways

- Focus on high-growth, complex sectors and value-added services is driving a shift toward higher-margin, long-term contracts and stronger revenue consistency.

- Global facility expansion and strong cash flow position Plexus to capitalize on sector trends, supporting sustained revenue growth and enhanced shareholder returns.

- Plexus faces revenue and margin volatility due to demand uncertainties, sector cyclicality, customer concentration, rising costs, and intensifying industry competition.

Catalysts

About Plexus- Provides electronic manufacturing services in the United States and internationally.

- Plexus is capitalizing on the growing demand for advanced electronics manufacturing fueled by digital transformation, IoT expansion, and emerging technologies like AI and connected vehicles, as reflected in a robust pipeline of new program wins across high-growth sectors-this is likely to drive sustained multi-year revenue growth and larger addressable markets.

- Strategic expansion and high utilization of global facilities, particularly the new Malaysia site (with initial focus on semicap and planned healthcare ramp), positions the company to meet increased demand both from reshoring/regionalization trends and sector-specific growth, which should support ongoing revenue gains and improved asset turnover.

- The company's increasing success in winning programs in high-margin, complex sectors such as healthcare/life sciences, aerospace, and defense (including strong defense pipeline in Europe and record sector wins), is shifting the revenue mix toward segments with higher pricing power and more stable, long-term contracts-this should positively impact both revenue consistency and net margin expansion.

- Continued investment and strong performance in high-value engineering and design services (now exceeding $100 million, growing, and diversified across more sectors), is allowing Plexus to move up the value chain, resulting in larger contract sizes, enhanced customer stickiness, and higher gross margins.

- Robust free cash flow generation and improved working capital efficiency have enabled greater returns to shareholders and provide Plexus with flexibility for further growth investments, supporting long-term earnings expansion.

Plexus Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

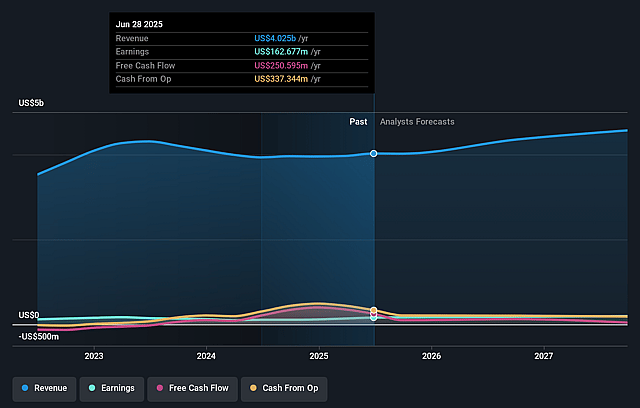

- Analysts are assuming Plexus's revenue will grow by 11.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.4% today to 4.6% in 3 years time.

- Analysts expect earnings to reach $278.4 million (and earnings per share of $10.32) by about July 2029, up from $187.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 35.4x on those 2029 earnings, down from 39.3x today. This future PE is greater than the current PE for the US Electronic industry at 31.9x.

- Analysts expect the number of shares outstanding to decline by 0.85% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.8%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing tariff-related uncertainties and rising protectionism lead customers to remain in a wait-and-see mode, which could dampen order activity and create unpredictability in revenue growth for Plexus over the long term (impact: revenue volatility and slower top-line growth).

- Customer-specific demand pushouts in high-growth verticals like semicap (now forecasting low double-digit growth instead of mid-teens), as well as flat outlooks in Aerospace, highlight Plexus's vulnerability to cyclical and program-driven fluctuations in its key sectors (impact: revenue instability and potential earnings variability).

- High customer concentration and a heavy reliance on large contract ramp-ups (notably in sectors such as healthcare and aerospace/defense) as well as the need for continuous new customer onboarding increase the risk that order reductions or delays from a few key customers could destabilize results (impact: revenue concentration risk and potential margin pressure).

- The anticipated margin drag from startup facilities (e.g., new Malaysian plant) and ongoing integration costs, combined with the long-term threat of margin compression from global competition and potential cost inflation in materials and labor, may erode profitability and limit sustained operating margin expansion (impact: net margin compression and lower earnings growth).

- The commoditization trend in the electronics manufacturing services industry, coupled with potential further consolidation among large OEMs, could increase price-based competition and bargaining power against mid-sized providers like Plexus, putting sustained pressure on both revenue and margins (impact: industry margin erosion and profit pressure).

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $293.25 for Plexus based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $330.0, and the most bearish reporting a price target of just $258.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $6.0 billion, earnings will come to $278.4 million, and it would be trading on a PE ratio of 35.4x, assuming you use a discount rate of 8.8%.

- Given the current share price of $275.11, the analyst price target of $293.25 is 6.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Plexus?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.