Last Update07 May 25Fair value Decreased 0.10%

Key Takeaways

- Integrated web platforms and large cloud providers are eroding GoDaddy’s core business, driving price wars and curbing growth in key offerings.

- Reliance on small businesses and changing digital presence trends create revenue volatility, while rising compliance costs pressure margins and sustainability.

- Effective pricing, innovative product adoption, and international growth are driving sustainable revenue, margin expansion, and increased shareholder value through disciplined operations and strategic investments.

Catalysts

About GoDaddy- Engages in the design and development of cloud-based products in the United States and internationally.

- The accelerating adoption of unified website and e-commerce platforms such as Shopify, Wix, and Squarespace threatens to significantly erode GoDaddy's core business of standalone domain registration and basic hosting, undermining both pricing power and growth in its addressable market and resulting in muted long-term revenue expansion and potential margin deterioration.

- A sustained shift by small businesses toward large-scale public cloud providers including AWS, Google Cloud, and Microsoft Azure is likely to marginalize GoDaddy's value-added offerings, leading to further commoditization, intensifying competitive pricing pressure, and curbing future net margin growth despite ongoing platform improvements.

- The company’s heavy reliance on structurally riskier small business customers leaves it highly exposed to economic cyclicality and higher churn, creating enduring volatility in customer cohorts and constraining stable recurring revenue and long-term earnings visibility.

- Persistent regulatory scrutiny and the rising cost of compliance with global data privacy regimes will force GoDaddy to allocate more resources to legal and operational safeguards, increasing operating expenses and compressing net margins, especially as it tries to expand internationally.

- The proliferation of alternative digital presences—such as direct engagement on social platforms, the emergence of decentralized web protocols, and growing mobile-first business adoption—will steadily lower demand for traditional web domains, causing gradual contraction in the company’s fundamental revenue base and impairing the sustainability of long-term free cash flow growth.

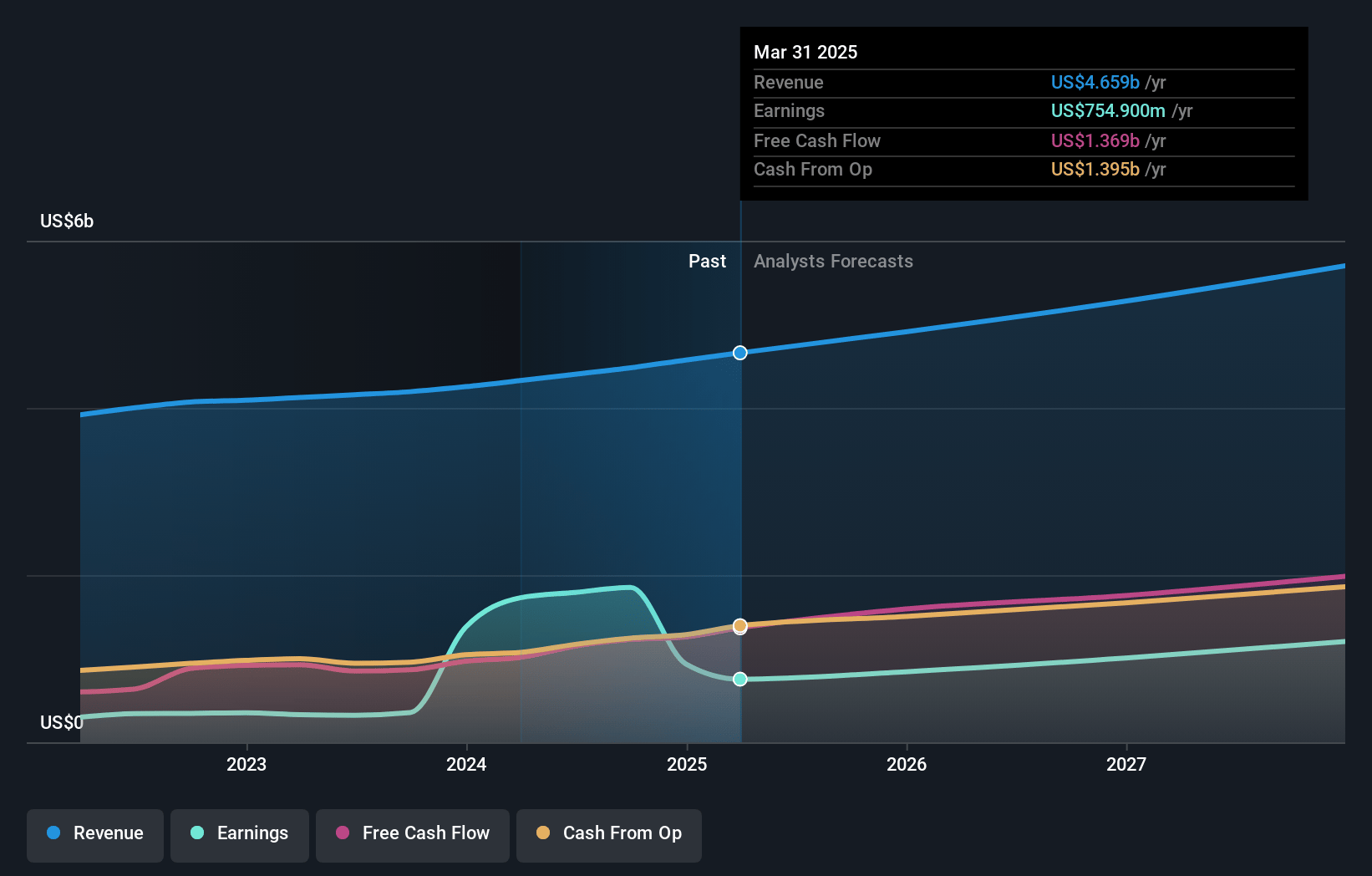

GoDaddy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on GoDaddy compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming GoDaddy's revenue will grow by 6.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 16.2% today to 18.8% in 3 years time.

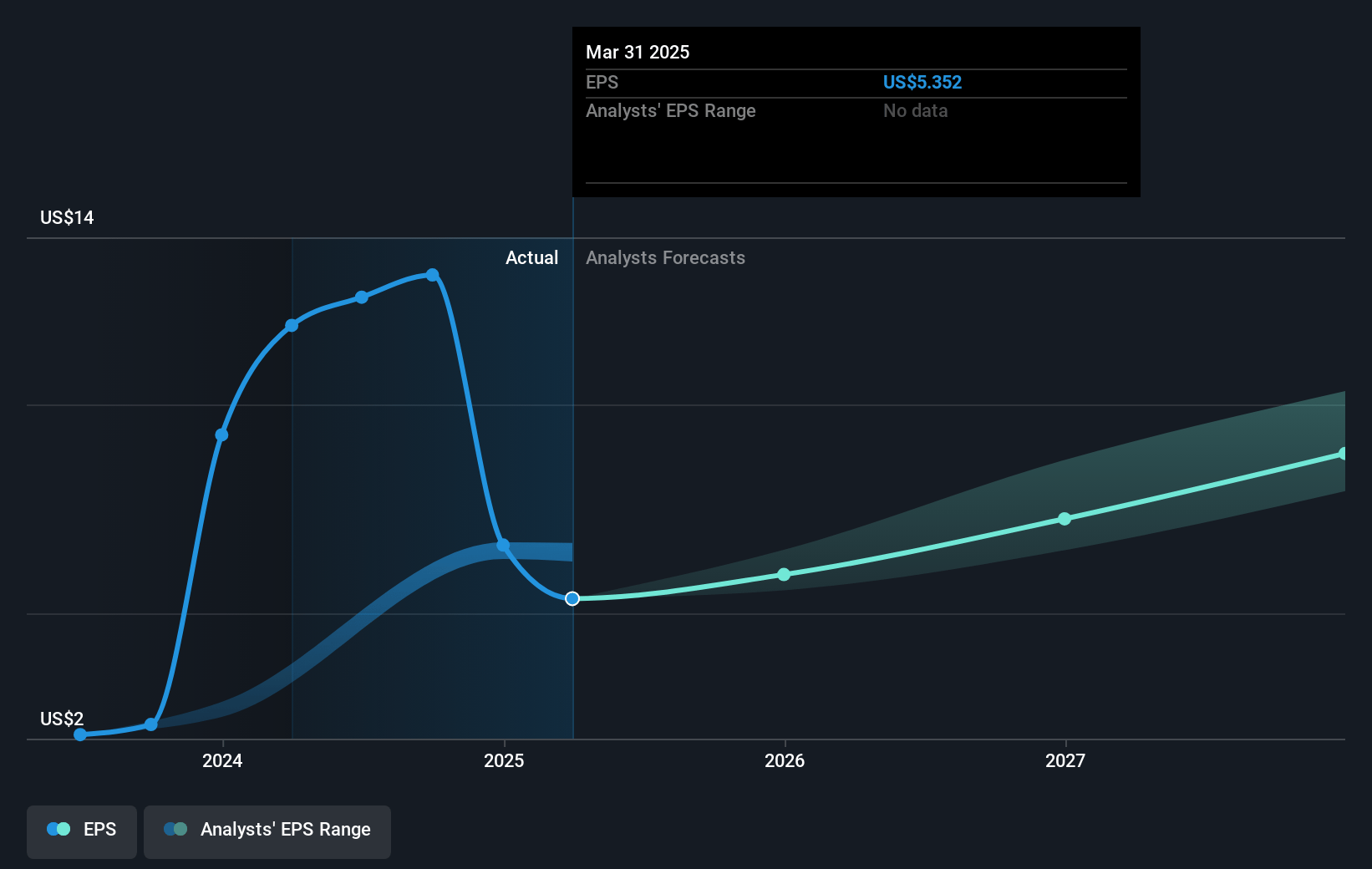

- The bearish analysts expect earnings to reach $1.0 billion (and earnings per share of $8.12) by about May 2028, up from $754.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 27.5x on those 2028 earnings, down from 34.6x today. This future PE is lower than the current PE for the US IT industry at 31.8x.

- Analysts expect the number of shares outstanding to grow by 1.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.16%, as per the Simply Wall St company report.

GoDaddy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing success of GoDaddy’s pricing and bundling strategies, which are exceeding internal expectations and driving higher average revenue per user and stronger customer retention, suggests sustainable top-line growth and expanded margin potential over time, supporting higher revenue and net earnings.

- Accelerating adoption and monetization of GoDaddy Airo and Airo Plus, with positive early signals around customer attach rates, increased product engagement, and upselling into higher-value SKUs, indicate the potential for increased customer lifetime value and recurring revenue.

- Consistent expansion in the high-margin Applications & Commerce (A&C) segment, which posted 17% revenue growth and 200 basis points margin expansion in the quarter, points to a successful shift toward premium business solutions that drive both revenue and net margin improvement.

- Strong international growth, particularly from aftermarket domain sales exceeding expectations, reflects durable demand and an expanding addressable market, which is likely to bolster revenue growth and support long-term earnings.

- Ongoing operational discipline, platform automation, and favorable product mix are yielding normalized EBITDA margin expansion and robust free cash flow growth, positioning GoDaddy to both invest in innovation and return capital to shareholders, thus improving overall earnings and shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for GoDaddy is $154.09, which represents two standard deviations below the consensus price target of $210.75. This valuation is based on what can be assumed as the expectations of GoDaddy's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $250.0, and the most bearish reporting a price target of just $150.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $5.6 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 27.5x, assuming you use a discount rate of 8.2%.

- Given the current share price of $183.11, the bearish analyst price target of $154.09 is 18.8% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.