Last Update 15 Apr 26

Fair value Increased 40%FSLY: Future Returns Will Depend On Executing Guidance Under Divided Street Views

Analysts have adjusted the Fastly fair value estimate from $13.71 to $19.17, reflecting updated views on revenue growth, profitability, and future P/E assumptions following a mix of recent target changes and ratings across the Street.

Analyst Commentary

Recent research on Fastly highlights a split view, with some analysts leaning more constructive on execution and valuation, while others are dialing back expectations for the coming year.

Bullish Takeaways

- Bullish analysts point to improving execution, citing recent investor meetings with management as a reason to be more comfortable with how the business is being run and how that could support the current P/E assumptions embedded in fair value work.

- Several price target increases, including moves to around the low to mid US$20 range, reflect a view that the current share price does not fully reflect potential revenue growth and room for multiple expansion if execution remains on track.

- Initiation with a bullish view suggests confidence that Fastly's positioning in its market can support longer term growth, which these analysts see as important in justifying higher valuation multiples.

- Upgrades and higher targets earlier in the period show that some analysts are willing to give Fastly credit for progress on profitability efforts, especially as management messaging becomes more consistent with market expectations.

Bearish Takeaways

- Bearish analysts have moved to more cautious stances, including downgrades to Hold, as several factors weigh on their outlook for the forward year, which in turn tempers how much upside they see in the shares relative to current valuation.

- Recent target cuts from certain firms suggest concern that earlier expectations for revenue growth or profitability may have been too optimistic, leading them to reset their P/E and revenue multiple assumptions.

- The clustering of both target raises and target reductions in a relatively short time frame signals that visibility into Fastly's execution and growth trajectory is mixed, which can make some analysts more conservative on fair value.

- Where ratings stay neutral despite management engagement, cautious analysts appear focused on execution risk and the possibility that Fastly may need more time to translate its plans into consistent financial performance that would support higher multiples.

What's in the News

- Fastly and LALIGA, Spain’s professional football association, are working together on technical solutions aimed at reducing illegal streaming of live sports. They are using AI driven detection tools to identify unauthorized streams in real time and help rights holders protect their content (Key Developments).

- The collaboration with LALIGA includes a joint anti piracy project intended to help platforms remove illegal content more precisely. Fastly, LALIGA, other technology firms, publishers, and regulators are working on software and best practices to disable unauthorized streaming without affecting legitimate traffic (Key Developments).

- Fastly’s Audit Committee approved the appointment of KPMG LLP as the independent registered public accounting firm for the fiscal year ending December 31, 2026, and dismissed Deloitte & Touche LLP from that role. Both decisions were made on March 4, 2026 (Key Developments).

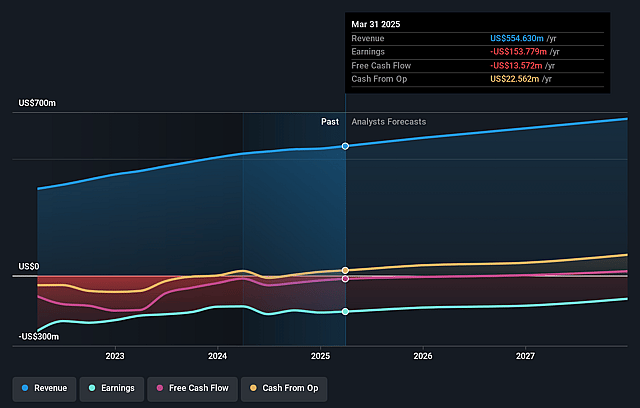

- For the first quarter of 2026, Fastly issued revenue guidance in a range of US$168.0 million to US$174.0 million. For the full year 2026, the company issued revenue guidance in a range of US$700.0 million to US$720.0 million (Key Developments).

Valuation Changes

- Fair Value: Updated estimate increased from $13.71 to $19.17 per share, a rise of roughly 40% based on revised inputs.

- Discount Rate: Adjusted slightly lower from 9.46% to 9.24%, indicating a modest change in the required rate of return used in the model.

- Revenue Growth: Assumed long term revenue growth moved from 11.08% to 11.56%, a small upward adjustment to the forecast.

- Net Profit Margin: Long term profit margin assumption shifted from 7.86% to 7.79%, a minor reduction in expected profitability levels.

- Future P/E: Future P/E multiple moved from 46.55x to 64.42x, reflecting a higher valuation multiple being applied in the updated work.

Key Takeaways

- Growth in advanced security and edge computing solutions, along with cross-selling strategy, drives higher-margin revenue and increases customer retention.

- Expanded enterprise focus, international investment, and operating efficiency boost diversified recurring revenue and support continued margin improvement.

- Intensifying competition, revenue concentration risks, and escalating costs threaten Fastly's pricing power, margins, and ability to achieve sustained, profitable growth.

Catalysts

About Fastly- Operates an edge cloud platform for processing, serving, and securing its customer’s applications in the United States, the Asia Pacific, Europe, and internationally.

- Ongoing adoption of advanced security solutions-including next-generation WAF, DDoS, and bot mitigation-positions Fastly to capitalize on rising enterprise demand for resilient edge security as cyber threats escalate, supporting future revenue growth and higher-margin service lines.

- The acceleration of cloud migration and edge computing, combined with Fastly's increased product velocity (especially in Compute and adaptive observability analytics at the edge), expands the company's addressable market and underpins durable multi-year revenue growth.

- Successful execution of a platform-based cross-sell and upsell strategy (with nearly 50% of customers now using 2+ products and these generating over 75% of revenue) boosts wallet share, increases net retention rates, and supports higher revenue per customer.

- Improved go-to-market alignment and expanded leadership, including segmented sales targeting enterprise clients beyond digital-native firms and investments in international expansion (particularly in APJ and Europe), diversifies and expands recurring revenue streams, reducing customer concentration risk and supporting top-line growth.

- Sustained focus on operating efficiency-with slower OpEx growth relative to revenue, disciplined cost controls, and improved cash collection-is driving operating leverage, setting the stage for continued margin improvement, a path to non-GAAP operating profitability, and stronger free cash flow.

Fastly Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Fastly's revenue will grow by 11.6% annually over the next 3 years.

- Analysts are not forecasting that Fastly will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Fastly's profit margin will increase from -19.5% to the average US IT industry of 7.8% in 3 years.

- If Fastly's profit margin were to converge on the industry average, you could expect earnings to reach $67.5 million (and earnings per share of $0.39) by about April 2029, up from -$121.7 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 64.8x on those 2029 earnings, up from -26.1x today. This future PE is greater than the current PE for the US IT industry at 20.8x.

- Analysts expect the number of shares outstanding to grow by 4.83% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.24%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Fastly's core content delivery network (CDN) market is commoditizing and facing increasing competitive pressure from hyperscalers (Amazon, Google, Microsoft) that can bundle CDN, security, and compute into integrated solutions, which may compress Fastly's pricing power and negatively impact revenue and net margins over time.

- The company has a history of volatile security revenue growth and remains dependent on a concentrated set of large customers (top 10 still represent 31% of revenue), leading to continued risk around revenue stability and susceptibility to customer churn or declining usage, potentially resulting in revenue volatility and difficulty sustaining long-term earnings growth.

- Ongoing industry consolidation and the exit of smaller players like Edgio may be a short-term boost, but larger industry players could eventually erode Fastly's market share given their broader offerings and scale, impacting Fastly's long-term revenue and competitive positioning.

- Fastly's need for continual investment in R&D, network infrastructure, and expansion into new security and compute products could keep operating margins depressed; if revenue growth does not consistently outpace these costs, the company may continue to experience prolonged negative net margins and delayed profitability.

- Increasing regulatory scrutiny on data privacy, cross-border data flows, and compliance (especially in regions like the EU and APJ) could raise Fastly's operational complexity and costs, limiting international expansion and potentially constraining future revenue and margin improvement.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $19.17 for Fastly based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $32.0, and the most bearish reporting a price target of just $7.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $866.5 million, earnings will come to $67.5 million, and it would be trading on a PE ratio of 64.8x, assuming you use a discount rate of 9.2%.

- Given the current share price of $20.95, the analyst price target of $19.17 is 9.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Fastly?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.