Last Update 09 Dec 25

WULF: Expanding High Performance Computing Contracts Will Drive Long-Term AI Infrastructure Leadership

Analysts have nudged their average price target for TeraWulf higher to about $21.50, reflecting growing confidence in the company’s expanding high performance computing contracts, strengthened power portfolio, and improving financing profile.

Analyst Commentary

Recent Street research has been overwhelmingly constructive on TeraWulf, with multiple bullish analysts lifting price targets into the high teens and low twenties as they recalibrate models for the company’s transition toward high performance computing and AI infrastructure.

Bullish analysts highlight that the business is evolving from a traditional bitcoin mining profile toward a more durable, contract-backed, AI-focused data center platform, which they see supporting higher, more resilient cash flows and a re-rating in valuation multiples.

Bullish Takeaways

- Bullish analysts see the ramp in high performance computing and AI colocation contracts, including large, long-dated hosting commitments, as significantly enhancing revenue visibility and supporting higher price targets.

- Expanded JV and colocation agreements, along with the ability to secure 250-500MW of additional capacity annually, are viewed as evidence that management can execute on an aggressive growth roadmap in a constrained power market.

- Improving financing conditions, including sizable secured note offerings priced at what some view as attractive levels, are seen as validating the TeraWulf credit profile and reducing balance sheet risk, which supports a lower cost of capital and higher valuation.

- The company’s control of high-quality, power-rich sites with access to low-cost renewable electricity and fiber networks is seen as a competitive advantage that positions it to capture a potentially outsized share of accelerating AI and GPU infrastructure demand.

Bearish Takeaways

- Some more cautious analysts point out that, despite recent contract wins and target hikes, the stock has experienced sharp volatility, suggesting execution missteps or delays could quickly pressure the shares and compress valuation multiples.

- There is concern that former bitcoin miners, including TeraWulf, may face a lengthy path before their debt and capital structures are viewed as investment grade, potentially limiting flexibility in a capital-intensive build-out cycle.

- While demand for AI and GPU infrastructure is strong, a growing set of competitors and new entrants in data center development could pressure long-term returns if pricing or contract terms normalize from today’s elevated levels.

- The strategy relies heavily on continued access to large power blocks and timely site development, so any slowdown in permitting, interconnects, or the supply chain for infrastructure could weigh on growth and delay the realization of targeted cash flows embedded in current price targets.

What's in the News

- TeraWulf executed a long term high performance computing joint venture with Fluidstack to develop 168 MW of critical IT load at its Abernathy, Texas campus, supported by a 25 year hosting commitment representing about $9.5 billion in contracted revenue, with TeraWulf holding a 51% majority stake and exclusive rights to partner on the next similar scale project.

- The joint venture will be project financed, with Google backing approximately $1.3 billion of Fluidstack long term lease obligations to support project related debt, which materially enhances the credit profile of the Abernathy build out.

- As a result of recent contracts, TeraWulf's contracted high performance computing platform now exceeds 510 MW of critical IT load, and the company has raised its growth outlook to target an additional 250 MW to 500 MW of contracted IT load per year.

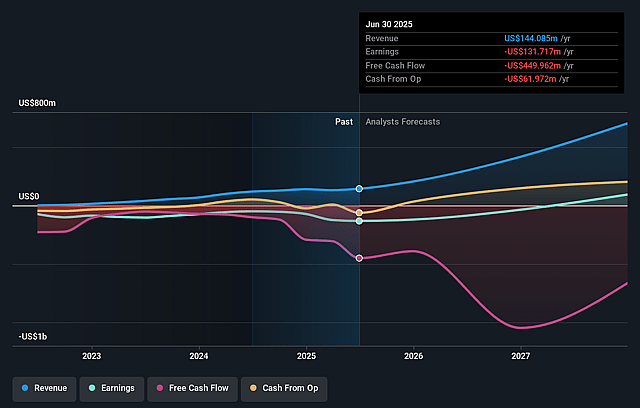

- TeraWulf issued new revenue guidance for the third quarter of 2025, projecting $48 million to $52 million in revenue, an increase of about 84% compared with the $27 million reported in the third quarter of 2024.

- The company completed its previously announced share repurchase program, buying back 24,468,750 shares for approximately $151.36 million, representing 6.38% of shares outstanding under the October 2024 authorization.

Valuation Changes

- Discount Rate edged lower from about 9.05% to 8.96%, modestly increasing the present value of projected cash flows.

- Revenue Growth remained essentially unchanged at approximately 83.74%, indicating no material shift in top line expansion assumptions.

- Net Profit Margin was effectively flat at about 7.72%, suggesting stable expectations for underlying profitability.

- Future P/E ticked down slightly from roughly 177.4x to 176.9x, reflecting a marginally lower valuation multiple on forward earnings.

- Fair Value Estimate held steady at about $21.44 per share, with no change in the model derived intrinsic value despite minor parameter adjustments.

Key Takeaways

- Transition to diversified digital infrastructure with major institutional backing reduces reliance on bitcoin price, boosting revenue stability and supporting margin growth.

- Expansion of sustainable, regulatory-compliant infrastructure positions the company to meet rising enterprise demand, drive new revenue streams, and achieve operational efficiency.

- Aggressive diversification into AI and HPC hosting exposes TeraWulf to rising costs, tenant risks, and operational challenges that threaten margin stability and long-term financial health.

Catalysts

About TeraWulf- Operates as a digital asset technology company in the United States.

- TeraWulf's recent multi-billion-dollar, multi-year hyperscale hosting agreements (e.g., with Fluidstack and Google), mark a significant shift from a pure bitcoin mining model toward diversified, contracted revenue streams in high-demand digital infrastructure-this underpins higher revenue visibility and insulates earnings from bitcoin price volatility.

- Long-term partnerships and investments from marquee players (Google's $1.8B lease backstop and equity stake) signal institutional validation, enhance creditworthiness, and are likely to lower WULF's future cost of capital, directly supporting margin expansion and accelerated infrastructure growth.

- Rapid expansion of zero-carbon, high-capacity digital infrastructure (Lake Mariner and Cayuga) positions TeraWulf to capture rising enterprise demand for sustainable, regulatory-compliant compute, supporting long-term revenue and improved net margins as regulatory and ESG pressures rise globally.

- Proven operational track record (on-time, on-budget delivery, experienced team, long-standing contractor relationships) de-risks future capacity scale-up and enables disciplined cost management, supporting sustained margin improvement and higher EBITDA.

- Growing momentum for institutional and enterprise digital asset adoption, coupled with TeraWulf's expansion into grid-interactive, renewable-powered data centers, positions the company to benefit from both higher transaction volumes and new ancillary revenue streams, enhancing long-term earnings stability and upside.

TeraWulf Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming TeraWulf's revenue will grow by 85.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from -91.4% today to 17.1% in 3 years time.

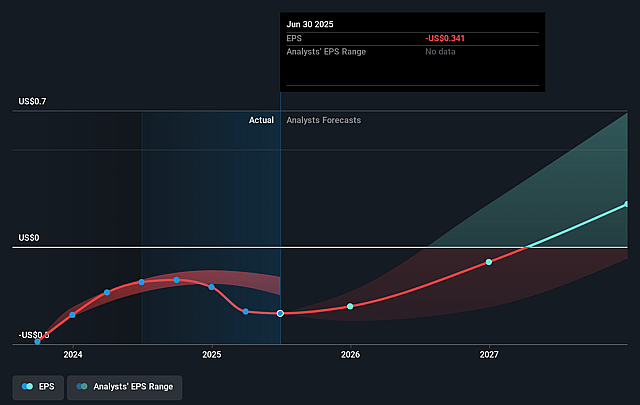

- Analysts expect earnings to reach $157.9 million (and earnings per share of $0.33) by about September 2028, up from $-131.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $405.2 million in earnings, and the most bearish expecting $-45.1 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 42.4x on those 2028 earnings, up from -27.8x today. This future PE is greater than the current PE for the US Software industry at 36.6x.

- Analysts expect the number of shares outstanding to grow by 1.56% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.78%, as per the Simply Wall St company report.

TeraWulf Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- TeraWulf's aggressive expansion into High Performance Computing (HPC) and AI data center hosting (e.g., the Fluidstack deal and Cayuga site development) requires substantial capital expenditures and increases debt exposure, introducing long-term risks to free cash flow, net margins, and balance sheet stability-especially if demand or execution timelines falter.

- The company's revenue stream is rapidly diversifying away from its legacy crypto mining business, but longer-term returns are highly dependent on maintaining "transformative" leases with newer tenants (e.g., Fluidstack) whose own financial stability, customer base, and AI sector demand are not fully transparent, creating potential risks to recurring revenue and earnings should counterparties struggle or market conditions shift.

- Although Google's backstop reduces near-term counterparty risk, its credit support for the Fluidstack lease declines over time and is tied to equity dilution, potentially impacting future shareholder value and exposing TeraWulf to ongoing concentration risks if similar structures are used in future expansions.

- TeraWulf faces escalating operational costs (e.g., labor, custom buildouts, supply chain constraints) as evidenced by higher CapEx on Fluidstack versus Core42 and increasing SG&A guidance, posing a risk to gross and net margins unless efficiencies scale materially or future contracts continue to deliver very high site-level net operating income.

- The company's long-term growth relies on sustained strong demand in both the AI infrastructure and crypto mining sectors, both of which could be adversely affected by regulatory changes (e.g., U.S. energy/environmental policy, digital asset legislation) or technology disruptions, leading to potential declines in revenue, EBITDA, or asset utilization if sectoral sentiment or policy support weakens.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $12.182 for TeraWulf based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $6.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $920.8 million, earnings will come to $157.9 million, and it would be trading on a PE ratio of 42.4x, assuming you use a discount rate of 8.8%.

- Given the current share price of $8.98, the analyst price target of $12.18 is 26.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on TeraWulf?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.