Key Takeaways

- AI-powered solutions and new AI products are expected to drive subscription growth, revenue, and profitability through enhanced conversions and direct monetization.

- Wix Studio's adoption and commerce platform strength contribute to partner revenue growth and net margin expansion, enhancing long-term earnings and cash flow.

- Intense competition and challenges in monetizing AI innovations could hinder Wix’s revenue growth and market share, despite significant investments in infrastructure and product innovation.

Catalysts

About Wix.com- Operates as a cloud-based web development platform for registered users and creators worldwide.

- Continued adoption and enhancement of AI-powered solutions like the AI Website Builder, which has improved user conversion rates by 13%, is expected to increase the number of paid subscriptions and improve revenue growth going forward.

- The launch of new AI products designed to transform business management and customer interaction is anticipated to open direct monetization avenues, likely boosting future revenue and profitability.

- The successful rollout and growing adoption of Wix Studio among agencies has driven a 30% year-over-year growth in partners' revenue; this momentum is expected to continue as Studio becomes a foundational element for professional users, improving long-term revenue growth.

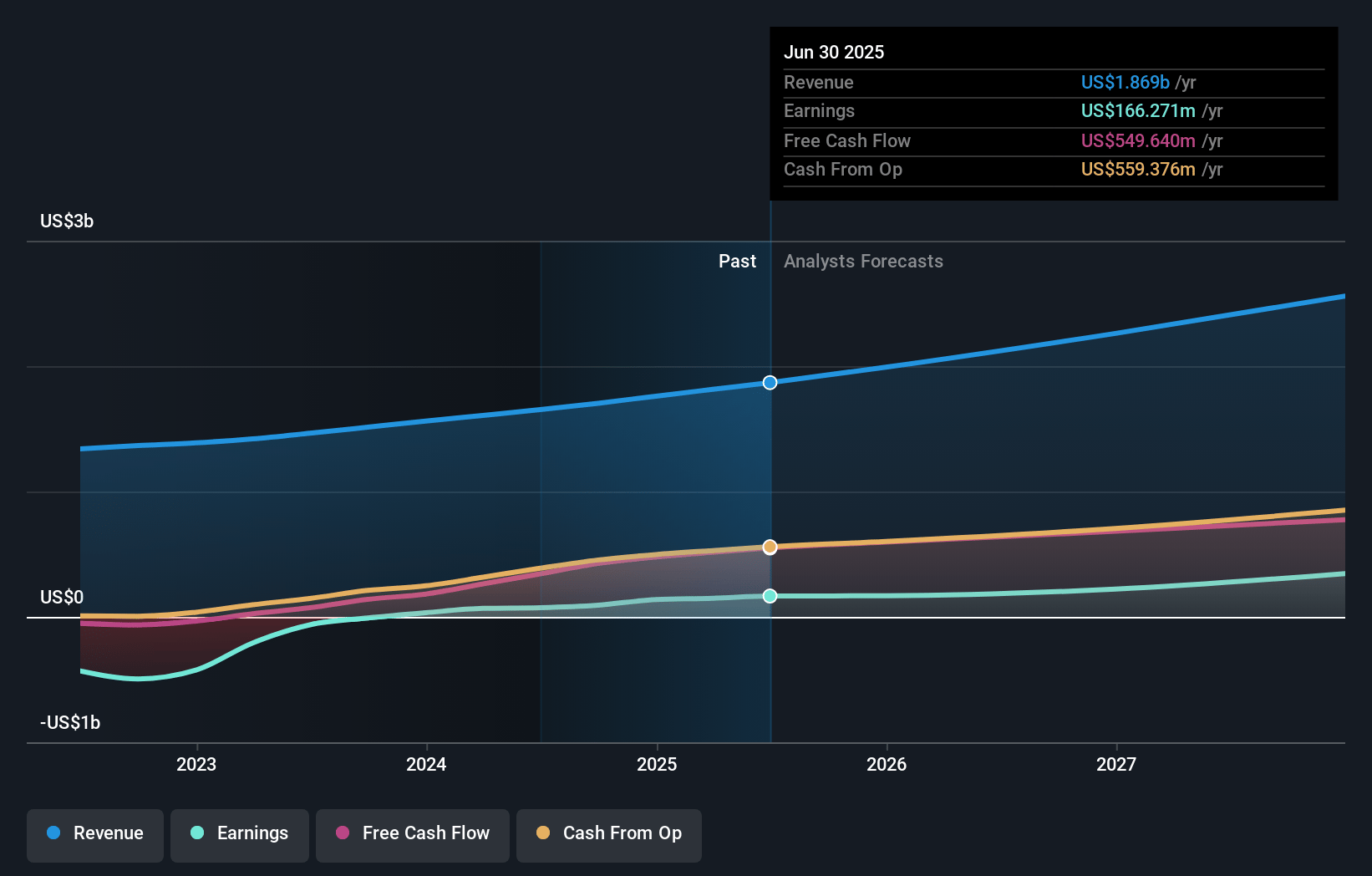

- The improvement in transaction revenue growth, helped by accelerating GPV growth and stable take rates, signals continued strength in the commerce platform, contributing to increased revenue and earnings.

- Operating cost stability alongside growth in high-margin business applications and improved payments, non-GAAP gross margins, and cost efficiencies suggest potential for further net margin expansion, enhancing earnings and cash flow in the coming years.

Wix.com Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Wix.com's revenue will grow by 14.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.5% today to 17.8% in 3 years time.

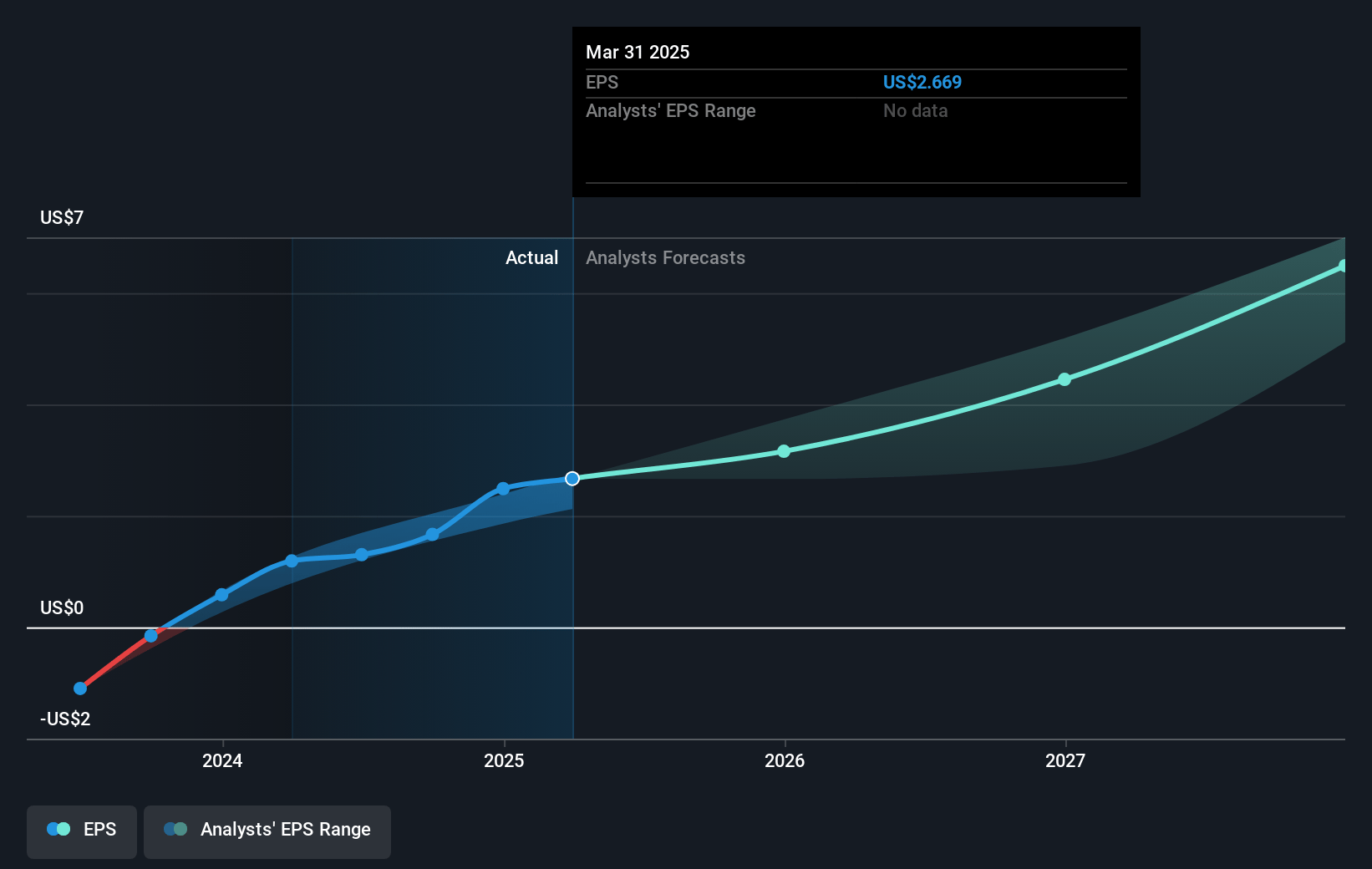

- Analysts expect earnings to reach $450.9 million (and earnings per share of $7.07) by about January 2028, up from $93.3 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $238.1 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 43.0x on those 2028 earnings, down from 148.1x today. This future PE is lower than the current PE for the US IT industry at 43.7x.

- Analysts expect the number of shares outstanding to grow by 4.43% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.77%, as per the Simply Wall St company report.

Wix.com Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The increasing reliance on AI products, while innovative, presents potential risks if the AI solutions do not meet market expectations or if competitors introduce superior products, which could impact Wix's ability to maintain its revenue growth.

- The company’s significant upfront investments in infrastructure and product innovation, especially related to AI and Studio, might not translate into proportional gains in revenue or profit, thereby impacting future earnings.

- Competition from established players like WordPress and new market entrants might erode Wix's market share, potentially limiting the growth in their self-creators and partner segments and affecting future revenue streams.

- The company's focus on high-intent cohorts and conversion efforts could see diminishing returns if the broader market for web-building solutions saturates, leading to stagnated user growth and impacting net margins.

- Any failure to effectively monetize upcoming AI products or misalignment between AI product offerings and customer demand could hinder revenue streams and expectations for margin improvements in the self-creators segment.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $238.93 for Wix.com based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $300.0, and the most bearish reporting a price target of just $166.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.5 billion, earnings will come to $450.9 million, and it would be trading on a PE ratio of 43.0x, assuming you use a discount rate of 8.8%.

- Given the current share price of $246.76, the analyst's price target of $238.93 is 3.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives