Last Update01 May 25Fair value Increased 46%

AnalystConsensusTarget made no meaningful changes to valuation assumptions.

Read more...Key Takeaways

- Expansion into voice commerce and innovative AI solutions aims to boost revenue through new partnerships and higher royalties, driving growth and profitability.

- Diversification of customer base and strategic acquisitions enhance financial stability, predictability, and market leadership, paving a path to stronger revenue and margins.

- SoundHound's dependency on partners and high R&D expenses poses financial risks, with challenges in net margins, customer concentration, and revenue predictability.

Catalysts

About SoundHound AI- Develops independent voice artificial intelligence (AI) solutions that enables businesses across automotive, TV, and IoT, and to customer service industries to deliver high-quality conversational experiences to their customers in the United States, Korea, France, Japan, Germany, and internationally.

- The unveiling of SoundHound's third business pillar, the voice commerce ecosystem, is expected to create a monetizable moment through revenue-sharing opportunities with OEMs, which could significantly boost future revenue streams.

- SoundHound's ability to innovate and implement generative AI solutions into its products, such as the SoundHound Chat AI Automotive, is expected to drive additional royalties per unit, resulting in higher revenue and improved profit margins.

- The company has significantly diversified its customer base across verticals like healthcare, financial services, and energy, reducing customer concentration and increasing the predictability of future revenue streams.

- By integrating its multimodal, multilingual foundation model, Polaris, with superior performance, SoundHound expects to consolidate its leadership in the voice AI market, enhancing its competitive edge and contributing to stronger revenue growth and improved net margins.

- SoundHound anticipates accelerating its path to profitability through strategic acquisitions, synergies, and increased SaaS-like recurring revenue streams, which are expected to improve financial stability and contribute to higher earnings over the longer term.

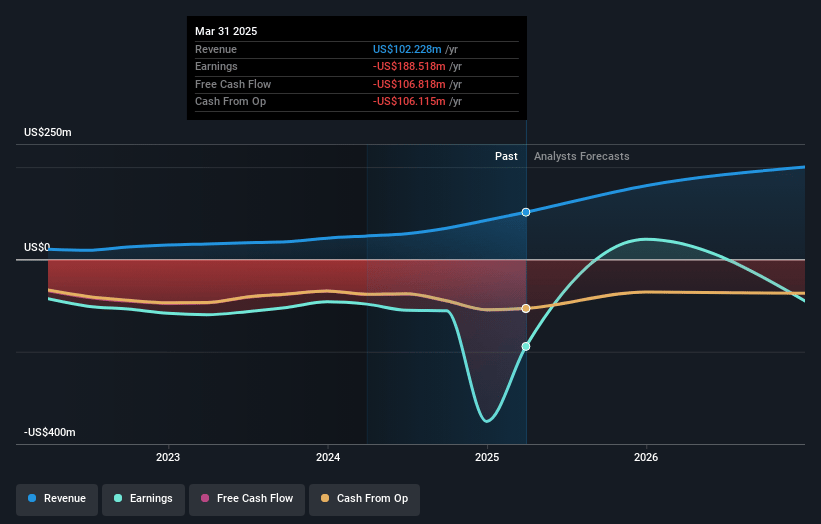

SoundHound AI Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming SoundHound AI's revenue will grow by 47.6% annually over the next 3 years.

- Analysts are not forecasting that SoundHound AI will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate SoundHound AI's profit margin will increase from -414.6% to the average US Software industry of 12.0% in 3 years.

- If SoundHound AI's profit margin were to converge on the industry average, you could expect earnings to reach $32.8 million (and earnings per share of $0.07) by about May 2028, up from $-351.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 258.3x on those 2028 earnings, up from -10.8x today. This future PE is greater than the current PE for the US Software industry at 31.6x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.64%, as per the Simply Wall St company report.

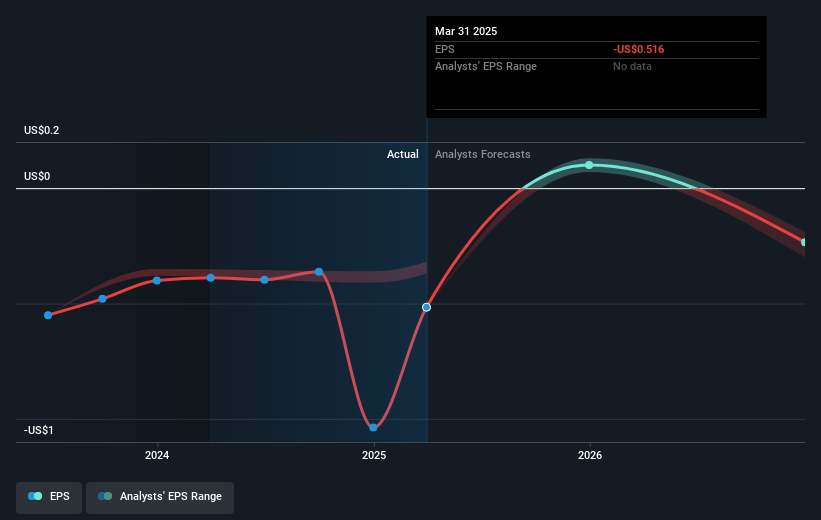

SoundHound AI Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- SoundHound's significant reliance on partnerships and third-party technologies for aspects of its platform (e.g., text-to-speech) may expose it to risks if these partners change terms or withdraw support, impacting its cost structure and margins.

- Despite strong revenue growth, SoundHound's net margins are challenged by expenses related to acquisitions, integration efforts, and high R&D costs, suggesting potential pressure on earnings and profitability.

- Customer concentration risks have improved but still exist, as a few customers previously accounted for a large portion of revenue. This could lead to revenue volatility if any key customer relationship deteriorates.

- The focus on automotive POCs and voice commerce, while promising, may have longer time horizons to revenue realization, potentially affecting near-term cash flow and predictability of earnings.

- The non-cash expense related to acquisition contingent liabilities and fluctuation in their valuation could lead to unpredictable swings in GAAP financial results, potentially impacting investor perception and share price stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $13.929 for SoundHound AI based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $8.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $272.5 million, earnings will come to $32.8 million, and it would be trading on a PE ratio of 258.3x, assuming you use a discount rate of 7.6%.

- Given the current share price of $9.47, the analyst price target of $13.93 is 32.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.