Last Update 15 Jul 26

Fair value Decreased 21%ROP: AI Execution And Buybacks Will Shape Future Upside Potential

Roper Technologies' analyst fair value estimate has been revised from $694.00 to $550.00 as analysts weigh mixed price target moves across the Street, alongside ongoing questions about how AI related disruption could affect the durability of the company’s financial model.

Analyst Commentary

Recent Street research on Roper Technologies presents a mixed but constructive backdrop, with several bullish analysts adjusting price targets higher while others stay cautious around AI related disruption and the durability of the company’s financial model.

The initiation of coverage at BMO Capital with a Market Perform rating and a US$393 price target underscores that some analysts see Roper Technologies as fairly valued for now, while they wait to see how management executes on internal AI initiatives and addresses sector wide concerns about business model durability.

At the same time, a cluster of recent price target changes, including increases of US$14, US$6 and US$10 from bullish analysts and a US$7 reduction from another firm, reflects an active debate about how to balance AI execution risk with the potential for long term growth and cash generation.

Bullish Takeaways

- Several bullish analysts have raised their price targets by US$6 to US$14. They frame this as a response to what they see as solid execution and a business mix they believe can support Roper Technologies' long term earnings power.

- These higher targets indicate that some on the Street view current valuation as reasonable relative to the cash flow profile they expect Roper Technologies to sustain, even as AI related questions remain unresolved.

- Bullish analysts highlight management’s internal AI initiatives as a potential positive catalyst. They argue that effective deployment could help preserve, and possibly extend, the durability of the company’s software heavy financial model.

- In the context of at least one lowered target, the cluster of upward adjustments suggests that a meaningful portion of the analyst community still sees room for upside if Roper Technologies continues to execute on its portfolio strategy and capital allocation plans.

What’s in the News for Roper Technologies

- Roper Technologies, Inc. (NasdaqGS: ROP) was dropped from the Russell Top 200 Index, according to index constituent updates.

- Roper Technologies was also dropped from the Russell Top 200 Value Benchmark, reflecting further index reclassification.

- The company was added to the Russell Midcap Index, shifting Roper Technologies into a different segment of the Russell index family.

- Roper Technologies was added to the Russell Midcap Value Benchmark, placing the stock within a value focused mid cap index group.

- From January 1, 2026 to April 30, 2026, Roper Technologies repurchased 5,772,000 shares, representing 5.41% of its shares, for US$2,028.4m. This brought total repurchases under the buyback announced on October 23, 2025 to 6,893,000 shares, or 6.46%, for US$2,528.22m.

- On April 23, 2026, Roper Technologies increased its equity buyback authorization by US$3,000m to a total of US$6,000m.

- During the first quarter 2026 financial results conference call, management said Roper Technologies is actively looking for acquisitions. They highlighted a pipeline of high quality opportunities and an approach that balances mergers and acquisitions with opportunistic buybacks, with comments attributed to President and CEO Laurence Hunn and Executive VP & CFO Jason P. Conley.

Valuation Changes for Roper Technologies

- Fair Value: revised down significantly from $694.00 to $550.00, reflecting a lower central estimate for Roper Technologies' share valuation in this model.

- Discount Rate: risen slightly from 9.00% to 9.34%, implying a modestly higher required return for the company in this framework.

- Revenue Growth: reduced from 14.51% to 10.75%, indicating a more restrained outlook for future top line expansion for Roper Technologies.

- Profit Margin: edged higher from 20.24% to 21.19%, suggesting a slightly stronger long term margin profile in the updated assumptions.

- Future P/E: moved down materially from 41.53x to 25.55x, pointing to a lower valuation multiple being applied to Roper Technologies' expected earnings.

Catalysts

About Roper Technologies

Roper Technologies is a diversified technology company that owns a portfolio of vertically focused software and tech-enabled businesses serving niche end markets.

What are the underlying business or industry changes driving this perspective?

- Broad adoption of AI across more than 20 vertical software platforms is expanding what Roper can sell into existing customers, as AI-enabled SKUs and features are layered on top of core systems of record. This supports potential uplift in recurring revenue and software margins over time.

- Deeply embedded vertical market software with proprietary workflow data, from legal and construction to health care and freight, gives Roper what management describes as a very high right to win in AI applications. This can support pricing power, high customer retention and resilient earnings.

- The buildout of AI driven freight automation at DAT, including carrier vetting, matching, automated rate negotiation and payments, targets meaningful per load labor savings for brokers. This can increase Roper’s monetization per transaction and support revenue growth and profitability in the Network Software segment.

- AI led automation in health care and public sector focused businesses such as CentralReach, Strata, CliniSys and others is already tied to strong bookings traction and higher value workflows. This can support growth in high margin recurring revenue and free cash flow.

- Rising digital and data needs at utilities, health care OEMs and other TEP customers, including ultrasonic metering and guidance enabled devices, are increasing software and data content per customer. This can help support revenue growth and, over time, mixed improvement in segment net margins.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Roper Technologies compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Roper Technologies's revenue will grow by 10.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 21.1% today to 21.2% in 3 years time.

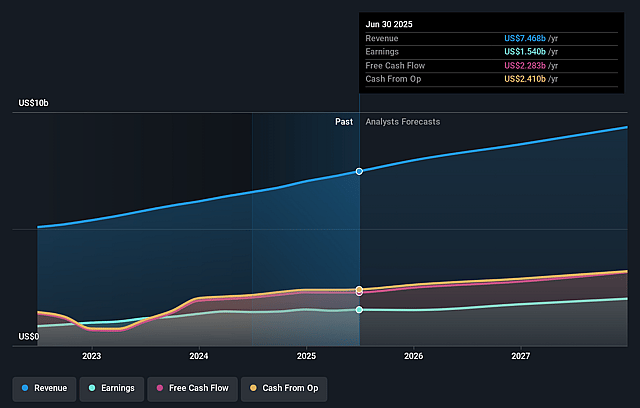

- The bullish analysts expect earnings to reach $2.3 billion (and earnings per share of $21.85) by about July 2029, up from $1.7 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $2.0 billion.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 25.6x on those 2029 earnings, up from 20.4x today. This future PE is lower than the current PE for the US Software industry at 28.9x.

- The bullish analysts expect the number of shares outstanding to decline by 6.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.34%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Prolonged weakness or repeated disruptions in key end markets such as government contracting and freight, including further government shutdowns or an extended freight downturn, could keep Deltek and DAT below their potential, which would pressure organic revenue growth and limit earnings expansion.

- Execution risk around AI commercialisation, where Roper successfully builds many AI features and SKUs but customers adopt them more slowly than expected or are unwilling to pay premium pricing, could mute the uplift in high margin recurring revenue and free cash flow that investors may be counting on.

- Higher input costs and tariff related actions similar to the Neptune copper surcharge, especially if utilities or other TEP customers resist or delay orders in response, could lead to ongoing timing issues and pricing friction that weigh on segment revenue and compress segment net margins.

- Roper’s heavy reliance on acquisitions and tuck ins to support growth, combined with moves like the unprofitable Convoy purchase, could expose shareholders to integration risk and earnings dilution if acquired businesses do not track to internal expectations, which would weigh on earnings and limit free cash flow per share growth.

- If competitive pressure in vertical software and freight automation intensifies, particularly as other vendors pursue AI based offerings and try to undercut on pricing, Roper’s “right to win” could be weaker than anticipated, which would affect pricing power, customer retention and ultimately revenue and EBITDA margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Roper Technologies is $550.0, which represents up to two standard deviations above the consensus price target of $445.92. This valuation is based on what can be assumed as the expectations of Roper Technologies's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $550.0, and the most bearish reporting a price target of just $349.78.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $11.0 billion, earnings will come to $2.3 billion, and it would be trading on a PE ratio of 25.6x, assuming you use a discount rate of 9.3%.

- Given the current share price of $346.65, the analyst price target of $550.0 is 37.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Roper Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.