Last Update 30 Jun 26

Fair value Decreased 13%APPF: AI Execution And 2026 Guidance Will Support Long-Term Re-Rating

Analysts have trimmed the AppFolio fair value estimate from $300 to $260, reflecting a reset in price targets after recent research updates that balance slightly softer revenue growth assumptions with more conservative P/E expectations and modestly stronger margin forecasts.

Analyst Commentary

Recent research on AppFolio points to a mixed but generally constructive backdrop, with some firms trimming price targets while at least one raised its target. This reflects differing views on how valuation, execution, and growth prospects line up at current levels.

Across these updates, analysts are recalibrating their models around revenue assumptions, P/E multiples, and margin expectations. There is still a clear cohort of bullish analysts who see room for upside based on AppFolio’s operating profile and longer term growth potential.

Bullish Takeaways

- Bullish analysts who raised their AppFolio price target cite enough support in the business to justify a higher valuation, even as others adopt more conservative P/E assumptions.

- Positive commentary around margin forecasts suggests some analysts see room for AppFolio to create value through improved profitability, not just top line growth.

- Despite several target cuts, the presence of an upward target revision indicates that some bullish analysts view recent research resets as an opportunity rather than a warning sign.

- Collectively, these reports show that while opinions differ on the exact fair value, there remains constructive sentiment around AppFolio’s ability to execute and support a premium valuation over time.

What’s in the News for AppFolio

- AppFolio rolled out a secure, native agent to agent connector that links its Realm-X AI suite with Anthropic’s Claude. This allows property managers to trigger complex leasing, accounting, and resident service workflows within governed accounting and compliance rules. The company plans to showcase the integration at the National Apartment Association’s Apartmentalize conference in June 2026. (Primary news)

- The company expanded the AppFolio Performance Platform with Anthropic powered agentic AI Performers that automate back-office accounting tasks, provide 24/7 multilingual leasing support, and support resident engagement, aiming to reduce manual work while maintaining data governance and compliance controls. (Primary news)

- Carillon Tower Advisers highlighted AppFolio in its Q1 2026 investor letter, noting the importance of the software for managing rental units, its relatively low-cost offering, and its industry-specific expertise as factors it sees as providing a competitive edge against generic AI tools. (Primary news)

- AppFolio was dropped from both the Russell 1000 Growth-Defensive Index and the Russell 1000 Defensive Index. This is a technical change that can affect how some index funds and quantitative strategies gain exposure to the stock. (Key developments)

- AppFolio reported that from January 1, 2026 to March 31, 2026 it repurchased 703,000 shares for US$125.1 million, completing a total of 946,987 shares for US$175.06 million under the existing buyback program. The company also communicated that 2026 revenue is expected to be in the range of US$1.11 billion to US$1.125 billion. (Key developments)

Valuation Changes for AppFolio

- Fair Value: Trimmed from $300 to $260, a reduction of about 13%, indicating a lower central estimate for AppFolio’s equity value.

- Discount Rate: Adjusted slightly higher from 8.47% to 8.54%, reflecting a modestly higher required return in the updated model.

- Revenue Growth: Tweaked from 18.16% to 17.93%, a small reduction that points to slightly softer top line assumptions for AppFolio.

- Profit Margin: Increased from 17.67% to 17.91%, suggesting a modestly stronger profitability profile in the revised outlook.

- Future P/E: Lowered from 48.36x to 37.52x, a significant compression that brings the valuation multiple assumptions closer to more conservative levels.

Key Takeaways

- Cloud-based, AI-enhanced platform and value-added services drive customer growth, improved efficiency, and recurring revenues in the digital property management sector.

- Industry consolidation and rising market demand position AppFolio for increased market share and long-term earnings expansion through innovation and strategic partnerships.

- Market dependency, intensifying competition, rising compliance costs, and challenges in expanding beyond core offerings threaten both revenue growth and long-term profitability.

Catalysts

About AppFolio- Provides cloud-based platform for the real estate industry in the United States.

- As more property managers and renters demand digital solutions to streamline and enhance their experiences, AppFolio’s cloud-based SaaS offerings and modern, mobile-first platform place it at the forefront of the ongoing shift to digital property management, driving sustained customer acquisition and ARPU growth, which directly benefits revenue.

- Rising rental housing demand from urbanization and shifting demographics expands the pool of multifamily units under management, supporting AppFolio’s continued unit growth momentum and opening opportunities to significantly scale revenue as well as increase customer stickiness in a growing market.

- Ongoing investment in AI-driven automation, including the adoption of Realm-X and other generative AI tools, is creating operating leverage by improving customer conversion rates and efficiency, which supports further expansion in net margins over time.

- The growing ecosystem of value-added services—including payment processing, screening, insurance, and new resident-centric features enabled through partnerships (such as with Second Nature and Zillow) and acquisitions (like LiveEasy)—enables AppFolio to increase recurring revenues and ARPU, which will drive top-line growth and potentially earnings expansion.

- Increasing consolidation in the property management software industry, combined with AppFolio’s innovation and strong balance sheet, positions the company to capture greater market share and pricing power, providing a long runway for above-market earnings and revenue growth.

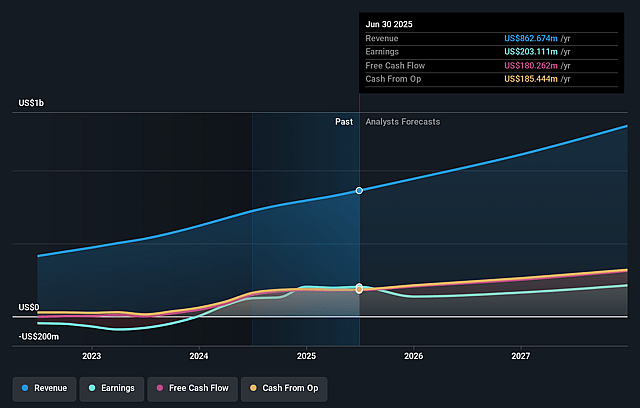

AppFolio Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on AppFolio compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming AppFolio's revenue will grow by 17.9% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 15.3% today to 17.9% in 3 years time.

- The bullish analysts expect earnings to reach $292.4 million (and earnings per share of $7.87) by about June 2029, up from $152.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 38.6x on those 2029 earnings, up from 36.4x today. This future PE is greater than the current PE for the US Software industry at 27.2x.

- The bullish analysts expect the number of shares outstanding to decline by 1.38% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.54%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- With AppFolio’s revenue and customer growth primarily concentrated in the U.S. residential property management sector, any prolonged slowdown or structural change in the U.S. real estate market — possibly driven by sustained high interest rates or falling demand for multifamily rentals — could cause significant volatility in its revenues and earnings over time.

- Increasing industry consolidation, with larger software competitors such as Yardi and RealPage gaining market power, may drive up customer acquisition costs and put pressure on AppFolio’s pricing, threatening both its future revenue growth and profit margins.

- Persistent investments in product development, AI innovation, and go-to-market strategies to keep up with rapid technological advances and meet customer expectations are already resulting in only modest headcount growth, but if operating cost increases outpace AppFolio’s pricing power, net margins could be pressured in the long run.

- Escalating regulatory scrutiny over tenant screening, fair housing, and data privacy demands greater investment in compliance and security features; this growing burden is likely to inflate general and administrative costs and weigh on future net earnings.

- As the market for property management software matures and core functionality becomes commoditized, AppFolio could face downward pressure on average revenue per user and greater customer churn if they fail to successfully expand into adjacent verticals beyond their current core, potentially capping long-term revenue potential.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for AppFolio is $260.0, which represents up to two standard deviations above the consensus price target of $224.25. This valuation is based on what can be assumed as the expectations of AppFolio's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $260.0, and the most bearish reporting a price target of just $185.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $1.6 billion, earnings will come to $292.4 million, and it would be trading on a PE ratio of 38.6x, assuming you use a discount rate of 8.5%.

- Given the current share price of $156.57, the analyst price target of $260.0 is 39.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AppFolio?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.