Last Update 02 Jul 26

Fair value Decreased 16%ALLT: Share Buyback And Earnings Outlook Will Support Bullish Repricing

Analysts have reduced their price target for Allot from $12.50 to $10.50, reflecting updated assumptions for revenue growth, profit margins, the discount rate, and the future P/E ratio in their valuation models.

What’s in the News for Allot

- The Board of Directors of Allot Ltd. authorized a share buyback plan on June 23, 2026, signaling a decision to allocate capital toward repurchasing shares. (Source: Key Developments)

- Allot Ltd. announced a share repurchase program of up to US$40 million of its ordinary shares, funded from existing cash resources, while continuing to invest in growth initiatives. (Source: Key Developments)

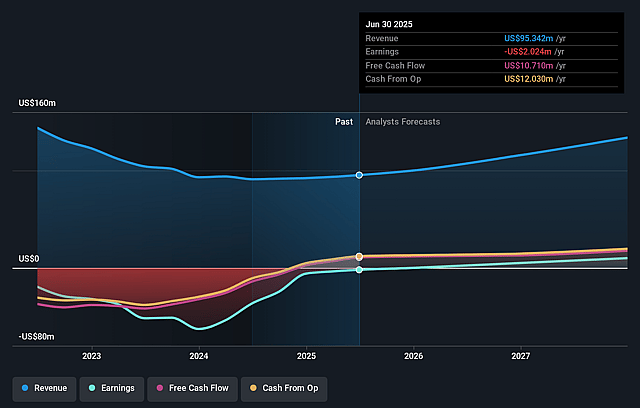

- Allot reaffirmed its 2026 earnings guidance, keeping revenue expectations in the range of US$113 million to US$117 million, with an emphasis on continued profitability improvements through the year. (Source: Key Developments)

- The company indicated it is looking for acquisitions, highlighting a capital allocation focus on organic growth, potential acquisitions and returning capital to shareholders, with the stated goal of maximizing long term shareholder value. (Source: Key Developments)

Valuation Changes

- Fair Value: Reduced from $12.50 to $10.50, indicating a lower central value estimate for Allot based on the updated model.

- Discount Rate: Adjusted slightly higher from 10.62% to 10.63%, reflecting a modest change in the required return used to discount future cash flows.

- Revenue Growth: Brought down from 15.71% to 11.75%, indicating more conservative expectations for Allot’s future top line expansion.

- Net Profit Margin: Increased from 13.27% to 13.81%, suggesting the model now assumes somewhat stronger profitability on each dollar of revenue.

- Future P/E: Trimmed slightly from 39.58x to 39.26x, indicating a marginally lower valuation multiple applied to Allot’s expected earnings.

Catalysts

About Allot

Allot provides cybersecurity and network intelligence solutions to communication service providers and enterprises.

What are the underlying business or industry changes driving this perspective?

- Although SECaaS annual recurring revenue of US$27.6 million and 60% year over year ARR growth highlight rising demand for consumer and telco cybersecurity services, a slowdown in new contract wins or lower attach rates at existing carriers could limit subscription expansion and temper future revenue growth.

- While the first OffNetSecure customer signals early adoption of security that follows users across any network and can create new subscription use cases, slower than expected uptake across the broader carrier base may restrict the product's ability to lift recurring revenue and delay any positive effect on earnings.

- Although recurring revenue accounted for 63% of Q3 2025 revenue compared with 58% a year earlier, a higher mix of lower margin or more resource intensive service contracts could cap the benefit of this shift and constrain further gains in gross margin and operating margin.

- While the smart network intelligence and Tera III product line is supported by a robust pipeline and a large installed base of tier one carriers, ongoing tight telco CapEx and challenging telecom sector conditions may limit project size and timing, which would weigh on product revenue and keep earnings growth uneven.

- Although Allot reports a strong cash position of US$81 million, no debt and three consecutive quarters of positive operating cash flow, execution missteps in scaling SECaaS globally or higher R&D and go to market spending to maintain technology leadership could compress net margins and reduce free cash generation.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Allot compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Allot's revenue will grow by 11.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 5.7% today to 13.8% in 3 years time.

- The bearish analysts expect earnings to reach $20.3 million (and earnings per share of $0.26) by about July 2029, up from $6.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 39.5x on those 2029 earnings, down from 71.2x today. This future PE is greater than the current PE for the US Software industry at 28.0x.

- The bearish analysts expect the number of shares outstanding to grow by 4.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.63%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- SECaaS currently contributes US$7.3 million of quarterly revenue and US$27.6 million of ARR. If telcos see weaker attach rates or slower subscriber adoption over time, subscription growth could flatten and limit revenue and earnings.

- The first OffNetSecure customer is an early proof point. However, if broad based adoption across carriers is slower than management expects, the product may not scale into a meaningful new use case, which would cap recurring revenue and pressure long term earnings growth.

- SECaaS is already 28% of revenue and recurring revenue is 63% of the total. This shift relies on continued R&D, marketing support and customer go to market investment. If operating expenses rise faster than subscription revenue, net margins and free cash generation could come under pressure.

- The smart and Tera III product line depends on ongoing spending by large carriers, and management already highlights tight telco CapEx and a challenging telecom sector. Prolonged cautious spending or delayed projects could limit product revenue and keep earnings growth uneven.

- Allot ended Q3 2025 with US$81 million in cash and no debt after a US$46 million follow on share offering. If the company needs further equity raises to fund long term growth, existing shareholders could see dilution while any slowdown in revenue or margin expansion would weigh on earnings per share.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Allot is $10.5, which represents up to two standard deviations below the consensus price target of $13.5. This valuation is based on what can be assumed as the expectations of Allot's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $19.0, and the most bearish reporting a price target of just $10.5.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $146.9 million, earnings will come to $20.3 million, and it would be trading on a PE ratio of 39.5x, assuming you use a discount rate of 10.6%.

- Given the current share price of $8.7, the analyst price target of $10.5 is 17.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Allot?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.