Last Update 07 Jul 26

Fair value Decreased 61%AEYE: Index Removal And Leadership Shift Will Reshape Future Performance

Analysts have reduced their fair value estimate for AudioEye from $18.00 to $7.00, citing updated assumptions that now reflect a higher discount rate, more moderate expectations for revenue growth and profit margins, and a lower future P/E multiple.

What’s in the News for AudioEye

- AudioEye is being removed as a constituent from multiple FTSE Russell benchmarks, including the Russell 2000 Index, Russell 2500 Index, Russell 3000 Index, Russell 3000E Index, and related growth and small cap completeness benchmarks.

- The company announced leadership changes, with Kelly Georgevich, previously Chief Financial Officer, appointed as Chief Executive Officer on May 4, 2026. Former CEO David Moradi became Executive Chairman and Chief Product Officer.

- On June 17, 2026, the Board approved the election of Matthew Domeyer as Chief Financial Officer, effective July 20, 2026, following Georgevich’s move to the CEO role.

- AudioEye changed its independent auditor on May 26, 2026, dismissing MaloneBailey, LLP and appointing RSM US LLP to audit the 2026 financial statements and review quarterly results starting with the quarter ending June 30, 2026.

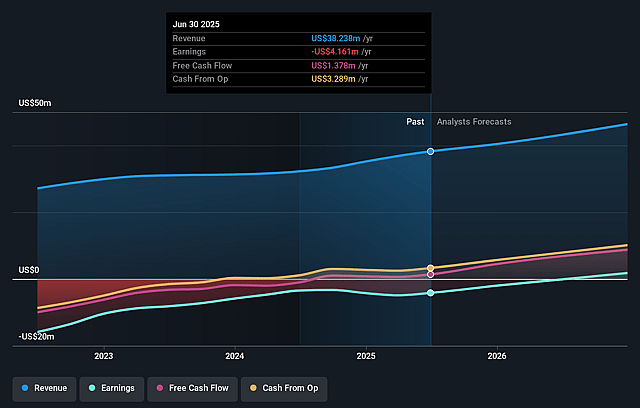

- The company issued earnings guidance for 2026. It expects revenue of approximately US$10.55 million for the first quarter, US$10.65 million to US$10.75 million for the second quarter, and US$43.25 million to US$44.25 million for the full year. The company also reported completing a share repurchase of 460,811 shares, or 3.71%, for US$5.05 million under the program announced on January 24, 2025.

Valuation Changes for AudioEye

- Fair Value: Reduced from $18.00 to $7.00, a significant downward reset in the analysts’ central estimate.

- Discount Rate: Increased slightly from 8.83% to 9.15%, implying a somewhat higher required return on AudioEye’s equity.

- Revenue Growth: Moderated from 12.81% to 9.72%, reflecting more measured assumptions for future revenue expansion.

- Net Profit Margin: Lowered from 19.24% to 11.32%, indicating a more conservative view on AudioEye’s future profitability.

- Future P/E: Reduced from 26.4x to 17.8x, pointing to a less generous valuation multiple being applied to potential future earnings.

Catalysts

About AudioEye

AudioEye provides digital accessibility solutions that help websites meet legal and usability requirements for people with disabilities.

What are the underlying business or industry changes driving this perspective?

- Although laws such as the DOJ Title II rule and the European Accessibility Act are set to increase demand for compliance tools, any delay in enforcement timelines or slower than expected customer adoption could limit the ramp in new contracts and keep revenue growth below management's aspirations.

- While the company is working AI capabilities like Playwright MCP into its platform to improve detection and accuracy, heavier reliance on AI tools may require sustained R&D spending and higher infrastructure costs, which could prevent the recent adjusted EBITDA margin of 24% from improving meaningfully.

- Although enterprise demand in the EU and U.S. is contributing to ARR of US$38.7m and higher average deal sizes in Europe, longer sales cycles or tighter IT budgets at larger customers could restrain ARR growth and slow progress toward higher earnings.

- While customer migration to the upgraded platform is expected to support gross margin improvement from the current 77%, any integration issues, unexpected churn or additional support costs could offset these gains and keep net margins under pressure.

- Although the Partner and Marketplace channel has a large SMB base and is tied to accessibility requirements that touch many smaller websites, partner renegotiations such as the one that reduced customer counts by about 3,000 and potential future repricing could weigh on reseller revenue and constrain free cash flow growth.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on AudioEye compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming AudioEye's revenue will grow by 9.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -9.0% today to 11.3% in 3 years time.

- The bearish analysts expect earnings to reach $6.1 million (and earnings per share of $0.48) by about July 2029, up from -$3.7 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $16.4 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 18.6x on those 2029 earnings, up from -24.3x today. This future PE is lower than the current PE for the US Software industry at 28.5x.

- The bearish analysts expect the number of shares outstanding to grow by 0.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.15%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- AudioEye is leaning heavily on regulatory catalysts such as the DOJ Title II rule in 2026 and the European Accessibility Act. If enforcement is slower, penalties are lighter than expected, or public sector budgets tighten, demand for accessibility tools could be weaker than management hopes, which would directly pressure ARR growth and revenue.

- The company is investing in AI approaches like Playwright MCP to improve detection and accuracy. If this technology does not translate into clear customer wins or cost efficiencies, AudioEye could see AI infrastructure and R&D costs stay high without matching pricing power, which would keep gross margin and adjusted EBITDA margins under strain.

- Enterprise deals in the EU and U.S. are described as larger, with some late stage opportunities above US$100,000 in ARR. If these long sales cycles slip, close at lower values, or face tougher competition as accessibility tools become more common, the mix shift toward enterprise could stall, limiting the long term uplift to revenue and earnings.

- The business is in the middle of migrating acquired customers to the Core platform to remove duplicate systems. If attrition from that integration is higher than expected or support needs increase, the company could see weaker ARR trends, more volatile customer counts, and less improvement in gross margin and free cash flow than it is aiming for.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for AudioEye is $7.0, which represents up to two standard deviations below the consensus price target of $15.75. This valuation is based on what can be assumed as the expectations of AudioEye's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $7.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $54.3 million, earnings will come to $6.1 million, and it would be trading on a PE ratio of 18.6x, assuming you use a discount rate of 9.2%.

- Given the current share price of $7.24, the analyst price target of $7.0 is 3.4% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AudioEye?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.