Last Update 24 Jun 26

Fair value Increased 5.87%QCOM: AI Data Center ASIC Deals Will Drive Future Rerating

Analysts have nudged the Qualcomm fair value estimate higher to $272.17 from $257.08, reflecting updated assumptions that factor in slightly higher long-term revenue growth, a marginally higher discount rate, and a modestly richer future P/E multiple tied to the company's push into broader AI compute markets beyond handsets.

Analyst Commentary

Recent Street research around Qualcomm centers on how far the company can extend beyond its handset roots and build a broader AI compute business spanning edge devices, automotive and IoT, and data center. Ahead of the upcoming investor day, several large firms have refreshed their models, which is feeding into a wider debate on long-term earnings power and what multiple that profile might support.

Across the bullish camp, the common thread is interest in Qualcomm's AI accelerator and custom ASIC ambitions in cloud and data center, alongside the existing AI100 Ultra footprint. Some analysts explicitly flag potential hyperscale partners and long-dated earnings frameworks. Others focus on the scale of data center revenue targets that may be discussed at the event.

On the more cautious side, several firms keep Neutral or Underperform stances even as they lift targets, citing an AI market that is described as fast growing but highly competitive, with entrenched incumbents and questions around product differentiation and execution. There are also mixed views on the outlook for the handset segment, with at least one downgrade tied to expectations for lower handset revenue in future fiscal years.

Overall, the Street is actively recalibrating Qualcomm valuation frameworks using later calendar and fiscal year assumptions. Higher outer year earnings estimates for AI and data center are often balanced by reservations around competition, handset trends, and the need to confirm execution milestones after the investor day.

Bullish Takeaways

- Bullish analysts are lifting Qualcomm price targets into a US$195 to US$265 range, with some rolling models to calendar 2028 or beyond, which signals higher confidence in longer term earnings potential from AI and data center initiatives.

- JPMorgan, while Neutral, explicitly places Qualcomm on its Positive Catalyst Watch and highlights potential data center revenue targets of more than US$3b in fiscal 2027 and US$35b in fiscal 2031. This frames a path to scale that underpins richer valuation scenarios if execution tracks those milestones.

- Some bullish analysts outline frameworks that reference earnings of roughly US$25 per share around fiscal 2031 and, in separate work, a bull case of more than US$2.50 of earnings per share per 1 gigawatt of AI capacity deployed. This points to meaningful operating leverage if Qualcomm secures sizeable hyperscale wins.

- Research citing Amazon Web Services as a likely lead hyperscale ASIC partner, alongside existing deployment of Qualcomm's AI100 Ultra and reports of relatively strong dollars per GPU hour, supports the view that the company has early traction with a major customer that could support growth and help justify higher long term P/E assumptions.

What’s in the News for Qualcomm

- Qualcomm is reported to be in advanced talks to acquire AI chip startup Modular Inc. for about US$4b, which would expand its AI infrastructure and data center processor capabilities beyond smartphone chips. (Source: Bloomberg summary)

- The company is also reported to be in advanced negotiations to acquire AI chip startup Tenstorrent in a potential US$8b to US$10b deal, focused on AI accelerators for data center and autonomous vehicle workloads. (Source: The Information summary)

- Qualcomm has agreed to supply millions of ASICs for ByteDance AI data centers and is in discussions to provide custom chip design services, marking one of its first large AI infrastructure wins outside handsets and adding a design services angle to the relationship. (Sources: primary ByteDance ASIC deal coverage, Reuters based summary)

- Ahead of its June 24 Investor Day, Qualcomm has set out an AI and data center roadmap that includes the Snapdragon C platform for AI PCs, the Dragonfly data center brand, and Dragonwing IQ10 robotics designs, along with plans for custom ASIC shipments starting in 2026. (Source: Investor Day preview coverage)

- Qualcomm continues to return capital to shareholders, with buyback updates showing 84,246,488 shares repurchased for about US$13.1b under the authorization announced on November 6, 2024. (Source: company buyback tranche disclosures)

Valuation Changes for Qualcomm

- Fair Value updated to $272.17 from $257.08, rising slightly on refreshed long term assumptions for Qualcomm's AI and data center opportunity.

- Discount Rate adjusted to 11.41% from 11.28%, rising slightly, which generally makes long dated cash flows less valuable in the model.

- Revenue Growth set at 3.46% from 3.39%, rising slightly, reflecting modestly higher long term top line expectations for Qualcomm.

- Net Profit Margin essentially unchanged at 25.09% versus 25.09%, indicating no material shift in long run profitability assumptions.

- Future P/E moved to 29.90x from 28.21x, rising modestly, suggesting the market model now applies a slightly richer valuation multiple to Qualcomm's projected earnings profile.

Key Takeaways

- Rapid expansion in automotive, IoT, and PC segments, combined with leadership in on-device AI, positions Qualcomm for above-industry-average earnings growth and margin improvement.

- Dominant patent portfolio and supply chain resilience provide robust downside protection, supporting stability and premium valuation amid industry and economic shifts.

- Growing competition, shifting customer strategies, and regulatory pressures threaten Qualcomm's core revenue streams, margins, and long-term profitability across handset and licensing businesses.

Catalysts

About QUALCOMM- Engages in the development and commercialization of foundational technologies for the wireless industry worldwide.

- While analyst consensus expects non-handset segment revenues (automotive, IoT, PC, XR) to hit $22 billion by fiscal 2029, recent quarterly growth rates in automotive (up 59% year over year) and industrial IoT (up 27% year over year) indicate that a substantially faster ramp is possible, potentially accelerating total company revenue and mix shift toward structurally higher-margin businesses.

- Analysts broadly agree that Snapdragon-powered PCs could reach just 12% market share by fiscal 2029, but current momentum-over 85 designs in development, major partnerships with Microsoft, and rapid expansion beyond the $600 price tier-suggests Qualcomm could far exceed share expectations in the premium and mass-market PC segments, driving upside to both PC revenues and blended operating margins.

- Qualcomm's leadership in on-device AI-enabled by its x85 5G platform, proprietary NPUs, and tight integration with leading foundation models-positions it to capitalize on an inflection point for AI at the edge, unlocking a multi-year upgrade cycle in smartphones, IoT, and XR devices that could boost average selling prices and long-term gross profit per unit.

- The global rollout of Wi-Fi 7 and early-stage 6G wireless standards leverages Qualcomm's dominant patent portfolio, enhancing recurring high-margin licensing revenues and providing robust downside protection to earnings, particularly as new device categories proliferate.

- Structural supply chain resilience due to geographic diversification and a growing share of automotive and industrial semiconductor content should allow Qualcomm to deliver more stable, above-industry-average earnings growth despite sector cyclicality or macro disruptions, supporting a premium valuation multiple.

QUALCOMM Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on QUALCOMM compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming QUALCOMM's revenue will grow by 3.5% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 22.3% today to 25.1% in 3 years time.

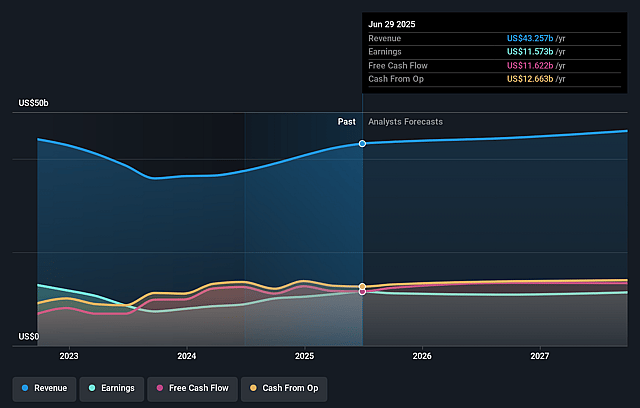

- The bullish analysts expect earnings to reach $12.4 billion (and earnings per share of $11.09) by about June 2029, up from $9.9 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $7.6 billion.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 29.9x on those 2029 earnings, up from 21.7x today. This future PE is lower than the current PE for the US Semiconductor industry at 68.8x.

- The bullish analysts expect the number of shares outstanding to decline by 2.32% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.41%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Growing insourcing of chip design by major customers-especially Apple, which is expected to further reduce its use of Qualcomm modems in upcoming product cycles-could erode Qualcomm's handset chipset revenues and compress gross margins as high-value customer contributions dwindle.

- Commoditization of mobile chipsets and intensifying competition from low-cost Asian competitors like MediaTek may increase price pressure in both premium and mid-tier segments, threatening Qualcomm's ability to maintain premium pricing and leading to declines in both revenue and net profit margins over time.

- Ongoing regulatory scrutiny, geopolitical tensions, and evolving tariffs-especially in China, where Qualcomm relies on a strong customer base-could restrict market access and increase compliance costs or operating risks, producing revenue volatility and added expense burden that pressure net income.

- The growing shift toward open-source and RISC-V architectures threatens Qualcomm's core intellectual property and licensing business, introducing the risk of reduced recurring royalties and licensing revenue which could lower overall operating margins and impact future profitability.

- Continued reliance on a small number of key smartphone OEMs-particularly in the premium Android and China market segments-creates revenue concentration risk and exposes Qualcomm to shifts in customer bargaining power, deteriorating the stability of its gross margins and increasing vulnerability to abrupt declines in earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for QUALCOMM is $272.17, which represents up to two standard deviations above the consensus price target of $186.5. This valuation is based on what can be assumed as the expectations of QUALCOMM's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $300.0, and the most bearish reporting a price target of just $100.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $49.3 billion, earnings will come to $12.4 billion, and it would be trading on a PE ratio of 29.9x, assuming you use a discount rate of 11.4%.

- Given the current share price of $204.13, the analyst price target of $272.17 is 25.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on QUALCOMM?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.