Key Takeaways

- Shrinking plus-size market and reliance on U.S. make long-term growth and revenue expansion increasingly challenging for Torrid.

- Rising e-commerce competition, store closures, and sustainability demands further threaten profitability and customer retention.

- Digital transformation, cost discipline, and brand-driven growth are enabling stronger margins, stable revenues, and sustained profitability despite physical store downsizing and market volatility.

Catalysts

About Torrid Holdings- Provides apparel, intimates, and accessories for curvy women in North America.

- The increasing consumer focus on health and wellness threatens to shrink the plus-size apparel market over the coming years, putting persistent downward pressure on Torrid's core addressable customer base and limiting long-term revenue growth despite any near-term brand or product innovation.

- As the shift to e-commerce accelerates, Torrid faces intensifying price competition from larger value retailers and digital-native brands with lower cost structures, significantly threatening net margin expansion and making it difficult to maintain profitability levels as online penetration rises toward 75 percent of sales.

- Ongoing store closures, while framed as optimization, heighten the company's exposure to the declining brick-and-mortar retail environment and risk further erosion of revenue due to customer attrition rates, with data showing only about 60 percent of customers are retained post-closure, which could drive further comparable sales declines and dampen top-line growth.

- Reliance on an overconcentration in the U.S. combined with a lack of meaningful international expansion opportunities leaves Torrid vulnerable to domestic economic weakness and limits the company's prospects for sustainable revenue and earnings growth outside its maturing core market.

- Growing pressure for investments in supply chain sustainability and changing consumer preferences may force significant capital commitments from Torrid, which could erode profitability and cash flow if not executed flawlessly, particularly as the industry's expectations for environmental and ethical manufacturing standards continue to rise.

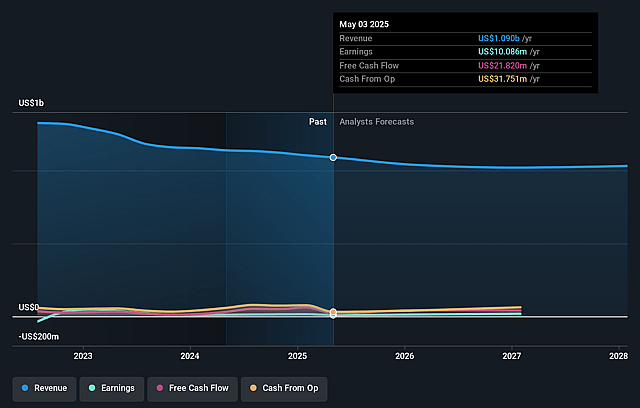

Torrid Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Torrid Holdings compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Torrid Holdings's revenue will decrease by 3.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 0.9% today to 2.5% in 3 years time.

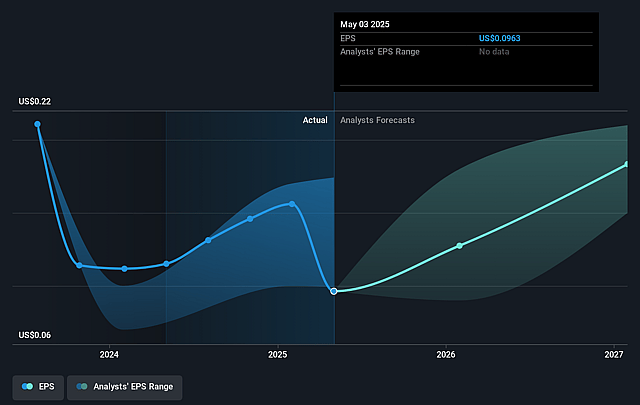

- The bearish analysts expect earnings to reach $25.2 million (and earnings per share of $0.24) by about July 2028, up from $10.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 13.1x on those 2028 earnings, down from 29.3x today. This future PE is lower than the current PE for the US Specialty Retail industry at 17.6x.

- Analysts expect the number of shares outstanding to grow by 0.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.55%, as per the Simply Wall St company report.

Torrid Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The accelerating growth and overperformance of Torrid's sub-brands, which are driving incremental demand from both new and younger customers as well as higher transaction sizes and higher-margin sales, could lead to increased revenues and improved gross and EBITDA margins over time.

- Strategic store optimization and rapid shift towards a digital-first model, with the ability to retain approximately 60% of customers after store closures through a robust loyalty program (encompassing 95% of the customer base), supports stable revenue and operating margin despite the contraction of physical retail.

- Investments in digital channel, data-driven marketing, and mobile app engagement are effectively driving customer acquisition, reactivation, and cross-category migration, supporting long-term sales growth and enhancing net margins through omnichannel synergies.

- The company's proactive efforts to mitigate tariff headwinds through diversified sourcing, cost-sharing with vendors, selective price increases, and pausing underperforming categories (such as shoes) demonstrate prudent cost management likely to protect or expand EBITDA margins in the future.

- Consistent discipline in expense management, along with a strategic reallocation of savings from store closures to marketing and technology investments, strengthens the foundation for enhanced profitability, sustainable revenue growth, and cash flow resilience over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Torrid Holdings is $2.25, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Torrid Holdings's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $7.0, and the most bearish reporting a price target of just $2.25.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $995.5 million, earnings will come to $25.2 million, and it would be trading on a PE ratio of 13.1x, assuming you use a discount rate of 11.6%.

- Given the current share price of $2.81, the bearish analyst price target of $2.25 is 24.9% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.