Last Update 05 Nov 25

Fair value Increased 0.77%JNJ: Upcoming Portfolio Shifts and Legal Uncertainties Will Shape Risk-Reward Balance

Johnson & Johnson's fair value estimate has increased by $1.52 to $199.56, as analysts point to improving core growth metrics, recent strong quarterly results, and expectations for higher margins following portfolio changes.

Analyst Commentary

Recent Street research reveals a mix of optimism and caution among analysts following Johnson & Johnson’s latest results, portfolio changes, and evolving sector dynamics. Analysts have updated their price targets and outlooks to reflect developments in the company’s structure and potential growth avenues.

Bullish Takeaways- Bullish analysts have raised price targets on Johnson & Johnson, citing strong quarterly results and the company’s confident guidance for 2025 operational sales growth.

- There is widespread enthusiasm regarding the planned separation of the orthopedics business. This move is expected to improve overall margins and growth rates for the remaining company.

- The company’s innovative medicine portfolio and robust pipeline are viewed as key drivers for future earnings momentum. Newer assets are becoming more central to the company's growth strategy.

- Despite challenges, analysts emphasize Johnson & Johnson’s defensive positioning and valuation. This suggests the stock remains attractive relative to its historical averages and sector peers.

- Bears remain cautious about near-term pressures, particularly the impact of Stelara’s loss of exclusivity. This development could temper short-term revenue growth.

- Ongoing legal risks, such as talc-related litigation and negative headlines surrounding subsidiary product lines, represent uncertainties that could impact consumer sentiment and sales momentum.

- Some analysts maintain a neutral stance and highlight only modest upward revisions to revenue guidance. They also reiterate concerns over potential pricing and tariff headwinds in the pharmaceutical sector.

- The transition and divestiture of slower-growth segments are closely watched for execution risk. There is a view that the benefits may take time to fully materialize.

What's in the News

- Johnson & Johnson faces its first UK lawsuits over allegations that its talc products cause cancer, with over 3,000 people suing the company and its subsidiary, Kenvue. J&J maintains it is not liable for litigation outside the U.S. and Canada, while Kenvue asserts their baby powder is safe (Reuters).

- A Los Angeles jury awarded a $966 million verdict against Johnson & Johnson to the family of a woman who died of mesothelioma. This marks the largest verdict to date in talc-related litigation against the company (Law.com).

- Reports indicate Johnson & Johnson is in talks to acquire Protagonist Therapeutics, a biotechnology company collaborating with J&J on oral treatments for immune diseases, in a deal potentially valued well above $4 billion (WSJ).

- Johnson & Johnson announced the withdrawal of the Linx Reflux Management System for acid reflux from markets outside the U.S., citing commercial reasons unrelated to safety or efficacy (Bloomberg).

- President Trump's administration is preparing investigations into whether U.S. trading partners are underpaying for pharmaceuticals. Johnson & Johnson and other global drugmakers could potentially be impacted by future trade or pricing actions (Financial Times).

Valuation Changes

- The Fair Value Estimate has risen slightly from $198.03 to $199.56 as a result of analyst updates.

- The Discount Rate remains unchanged at 6.78%, indicating no shift in the perceived risk profile.

- The Revenue Growth forecast has increased marginally from 5.08% to 5.10%.

- The Net Profit Margin is up modestly from 23.44% to 23.49%.

- The Future P/E Ratio has decreased from 23.97x to 23.33x, suggesting expectations for improved earnings.

Key Takeaways

- Johnson & Johnson is poised for growth in immunology and oncology despite facing challenges from loss of drug exclusivity, leveraging next-gen therapies for strengthened revenue.

- Strategic investments in U.S. operations, acquisitions, and MedTech expansion aim to boost future earnings and efficiency, with potential restructuring in surgery to aid profitability.

- Loss of exclusivity for key products and tariffs could significantly threaten revenue and margins, while ongoing litigation poses financial risks.

Catalysts

About Johnson & Johnson- Engages in the research and development, manufacture, and sale of various products in the healthcare field worldwide.

- Johnson & Johnson anticipates accelerated growth in their portfolio and pipeline, particularly in the Innovative Medicine sector, despite the headwind from STELARA's loss of exclusivity. This is expected to bolster revenues through next-generation therapies and significant market share gains in oncology and immunology.

- The company's substantial investment of over $55 billion into manufacturing, R&D, and technology in the U.S. over the next four years is projected to expand capacity for advanced medicines and devices, potentially increasing operational efficiency and future earnings.

- Recent acquisitions, such as Intra-Cellular Therapies, are expected to contribute substantial revenue streams, with products like CAPLYTA potentially reaching over $5 billion in peak sales, positively affecting the company’s revenue and EPS in the future.

- Ongoing expansion within MedTech, highlighted by strong performance from acquired cardiovascular units Abiomed and Shockwave, as well as developments in robotic surgery, are expected to drive revenue growth and enhance adjusted income margins over time.

- The company plans significant restructuring in their surgery business within MedTech to streamline operations and improve efficiency, anticipated to have short-term revenue disruptions but expected to enhance long-term profitability and margin expansion.

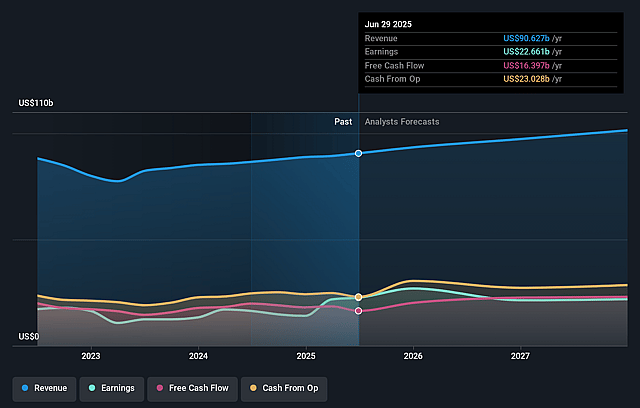

Johnson & Johnson Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Johnson & Johnson's revenue will grow by 4.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 25.0% today to 22.0% in 3 years time.

- Analysts expect earnings to reach $22.9 billion (and earnings per share of $10.07) by about September 2028, up from $22.7 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $19.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.8x on those 2028 earnings, up from 18.8x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 19.0x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.78%, as per the Simply Wall St company report.

Johnson & Johnson Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Loss of exclusivity for STELARA and the impact of biosimilar competition could significantly erode revenue from one of Johnson & Johnson's major products. This could affect overall revenue and net margins, especially in the innovative medicine segment.

- Tariffs, particularly those related to exports to China, could increase costs and impact the net margins negatively, due to increased cost of goods sold from tariffs being relieved through the P&L in future periods.

- The ongoing litigation related to talc, though controlled for now, poses a continual risk to financial stability and could impact net earnings and cash flow, particularly if adverse judgments or settlements occur.

- The orthopedics segment faced headwinds, including competitive pressures and challenges in the spine and sports areas. Ongoing issues could impact revenue and earnings unless the planned innovations drive a turnaround.

- Potential dilution from acquisitions such as Intra-Cellular Therapies and the impact of tariffs could affect operating margin improvement efforts, challenging overall earnings and net margins despite robust sales growth in some areas.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $177.468 for Johnson & Johnson based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $200.0, and the most bearish reporting a price target of just $155.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $104.1 billion, earnings will come to $22.9 billion, and it would be trading on a PE ratio of 22.8x, assuming you use a discount rate of 6.8%.

- Given the current share price of $176.96, the analyst price target of $177.47 is 0.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.