Key Takeaways

- Regulatory and competitive pressures, including from low-cost alternatives and FDA challenges, may impact revenue from key products like EYLEA.

- Significant R&D and expansion investments could strain financial resources, affecting margins and earnings in the near-to-medium future.

- Competitive pressures, regulatory challenges, and supply chain issues could hinder Regeneron's revenue growth and market share, impacting future earnings potential.

Catalysts

About Regeneron Pharmaceuticals- Regeneron Pharmaceuticals, Inc. discovers, invents, develops, manufactures, and commercializes medicines for treating various diseases worldwide.

- Regulatory challenges, such as the FDA's complete response letter for EYLEA HD pre-filled syringe, may lead to delays in EYLEA HD reaching its potential in the market, impacting revenues negatively.

- Increased competition from low-cost alternatives like Avastin due to funding gaps at co-pay assistance foundations could reduce demand for higher price-point products like EYLEA, thereby impacting net sales and revenue figures.

- Although Dupixent's sales are growing strongly, broader market competition and the need for further US regulatory approvals for new indications may moderate future revenue growth prospects.

- Compliance with increased FDA scrutiny on third-party component suppliers could result in delays and operational costs, thus potentially impacting net margins and profit levels.

- Despite pipeline progress, significant investments in R&D and manufacturing expansion might strain financial resources, potentially affecting net margins and earnings in the short to medium term.

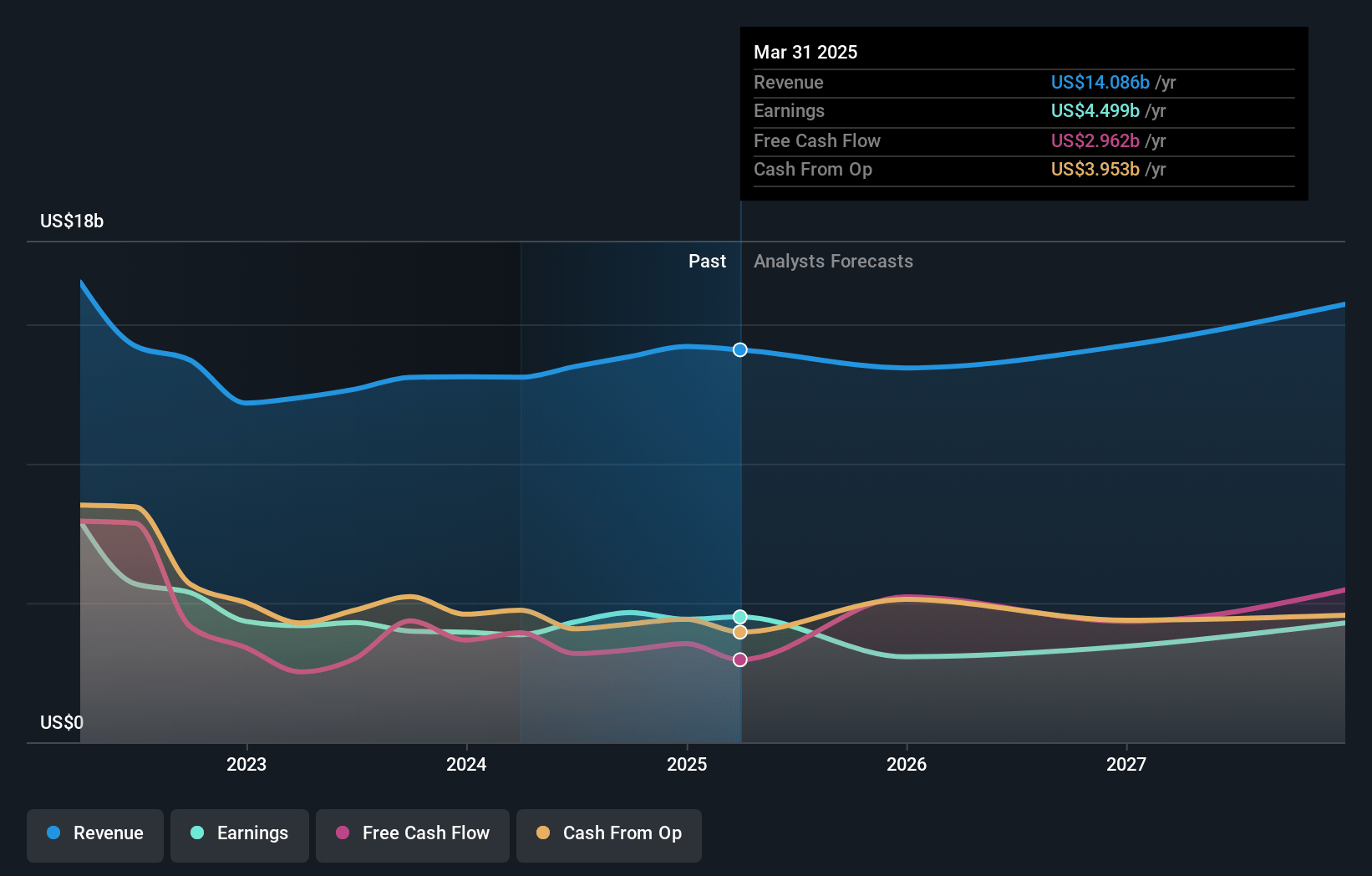

Regeneron Pharmaceuticals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Regeneron Pharmaceuticals compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Regeneron Pharmaceuticals's revenue will grow by 1.1% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 31.9% today to 17.8% in 3 years time.

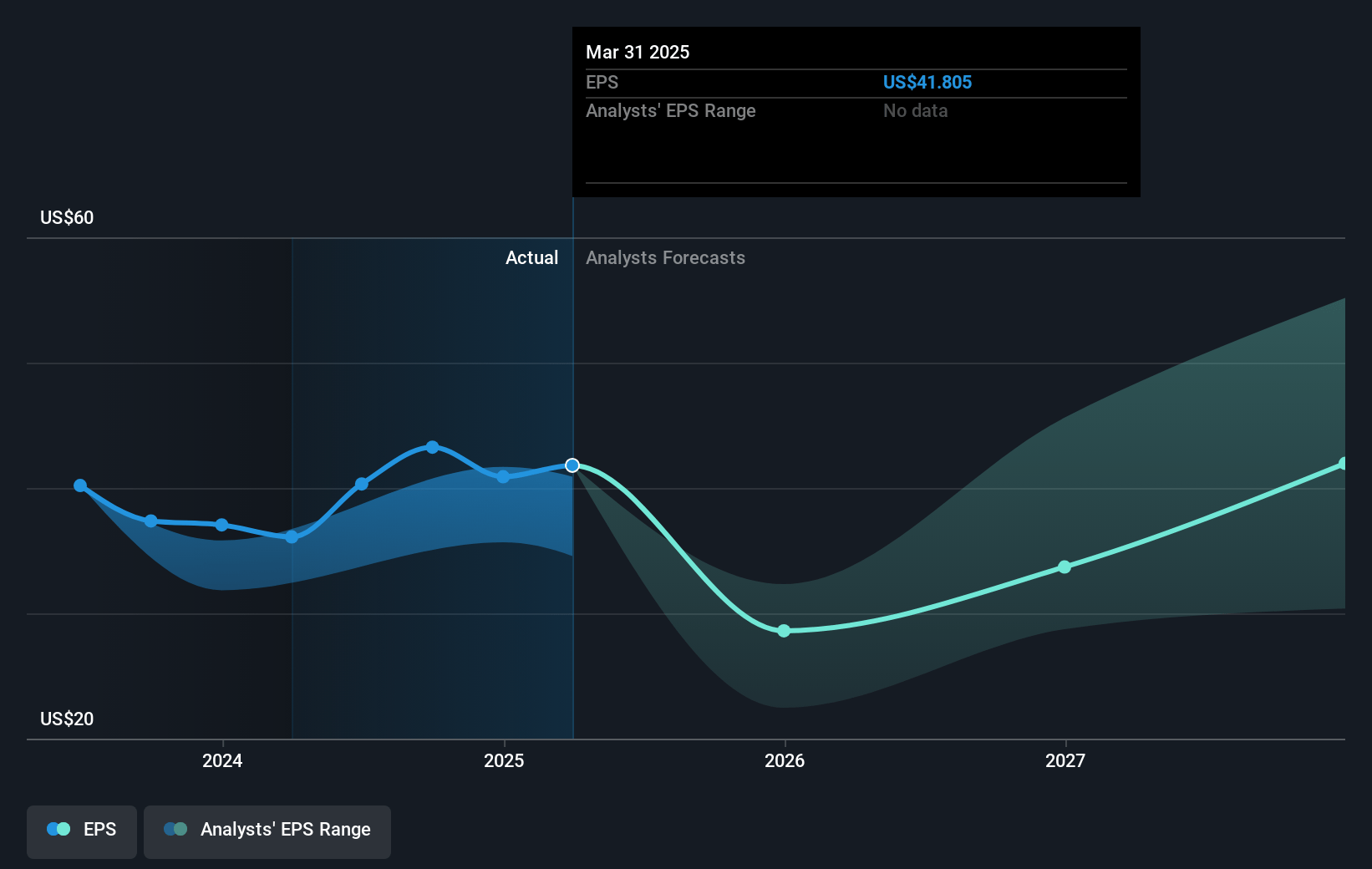

- The bearish analysts expect earnings to reach $2.6 billion (and earnings per share of $30.32) by about April 2028, down from $4.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 31.3x on those 2028 earnings, up from 14.1x today. This future PE is greater than the current PE for the US Biotechs industry at 20.4x.

- Analysts expect the number of shares outstanding to decline by 2.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.49%, as per the Simply Wall St company report.

Regeneron Pharmaceuticals Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in EYLEA's U.S. net sales by 39% year-over-year due to competition from low-cost off-label Avastin and wholesaler inventory issues indicates potential ongoing revenue and profit pressures.

- The issuance of a complete response letter by the FDA for the EYLEA HD pre-filled syringe suggests potential delays and regulatory hurdles that could affect future earnings growth.

- Potential supply chain and regulatory issues with third-party component suppliers, as indicated by issues with the EYLEA HD syringe, might lead to disruptions and increased costs, impacting net margins.

- The dependency on charitable foundations for patient assistance, combined with funding gaps, has led to a shift toward off-label Avastin, potentially affecting Regeneron’s market share and revenue.

- Regulatory scrutiny and frequent CRLs suggest potential operational inefficiencies, which could lead to delays in product launches and affect revenue growth projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Regeneron Pharmaceuticals is $677.01, which represents one standard deviation below the consensus price target of $807.63. This valuation is based on what can be assumed as the expectations of Regeneron Pharmaceuticals's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $979.0, and the most bearish reporting a price target of just $535.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $14.5 billion, earnings will come to $2.6 billion, and it would be trading on a PE ratio of 31.3x, assuming you use a discount rate of 6.5%.

- Given the current share price of $598.76, the bearish analyst price target of $677.01 is 11.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:REGN. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.