Key Takeaways

- Regulatory approvals and new market penetrations enhance revenue growth and strengthen Regeneron's competitive position in key therapeutic areas.

- Investments in manufacturing and R&D boost operational efficiency, while shareholder-focused actions aim to increase stock attractiveness.

- Competitive pressures, regulatory hurdles, and reliance on third parties risk negative impacts on Regeneron's profit margins and revenue streams.

Catalysts

About Regeneron Pharmaceuticals- Regeneron Pharmaceuticals, Inc. discovers, invents, develops, manufactures, and commercializes medicines for treating various diseases worldwide.

- Regulatory approvals and potential label enhancements for EYLEA HD, including monthly dosing and use in treating retinal vein occlusion, are expected to drive future revenue growth as they may strengthen EYLEA HD's competitive position in the anti-VEGF category.

- Dupixent's continued expansion across multiple Type 2 allergic diseases, with recent approvals in chronic spontaneous urticaria and potential approval in bullous pemphigoid, should significantly enhance revenue growth by penetrating new markets and maintaining leadership in existing indications.

- Ongoing pipeline developments, including pivotal readouts for itepekimab in COPD and other diseases, and anticipated oncology approvals for Libtayo and linvoseltamab, could contribute to higher future earnings by diversifying and expanding Regeneron’s market presence.

- Investments in U.S. manufacturing capacity expansion and R&D are set to enhance operational efficiencies, potentially improving net margins by supporting cost-effective production and enabling faster delivery of new treatments to patients.

- Share repurchases and a newly initiated dividend program aim to increase shareholder value, potentially growing earnings per share (EPS) and making the stock more attractive to investors.

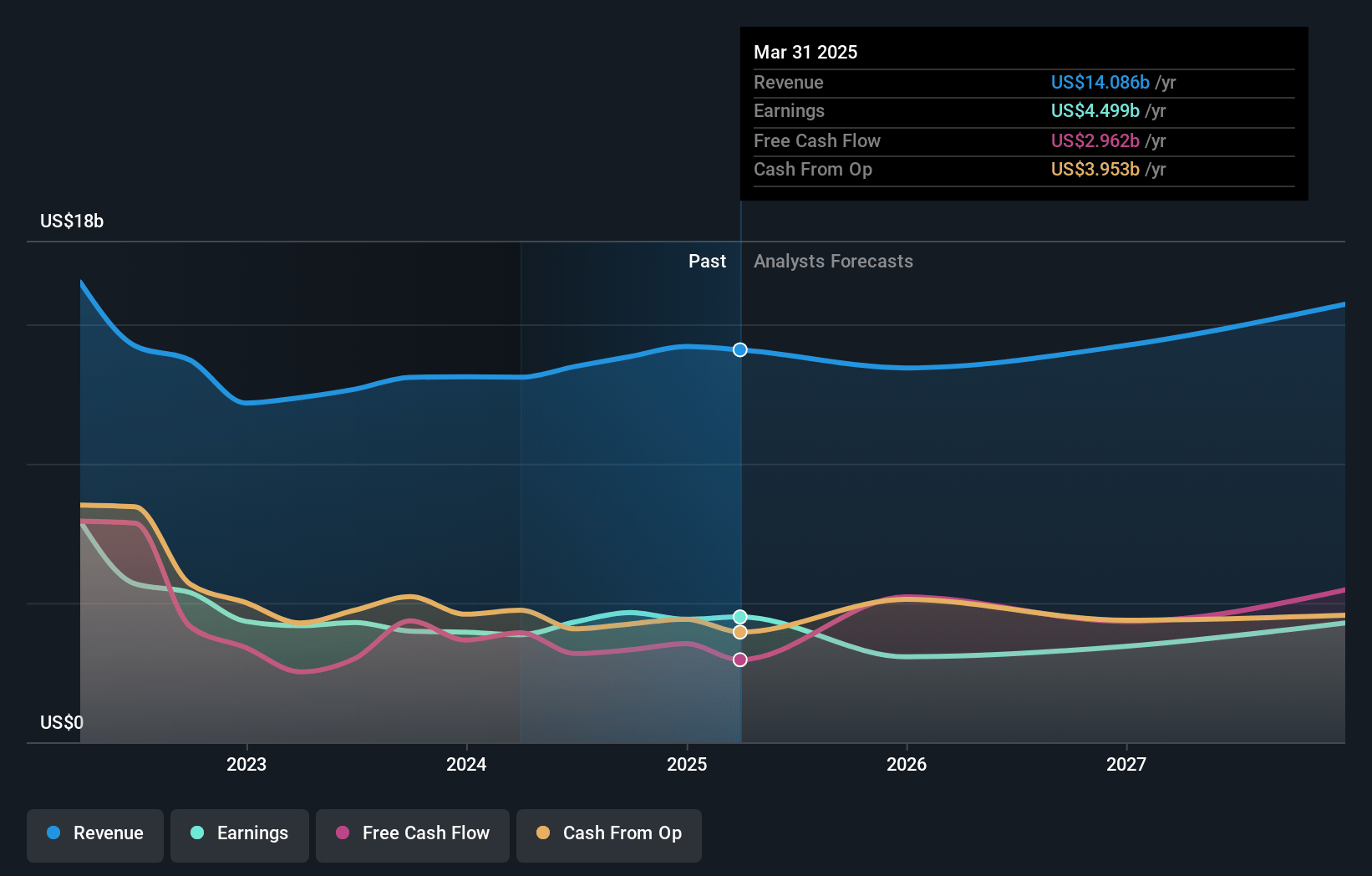

Regeneron Pharmaceuticals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Regeneron Pharmaceuticals's revenue will grow by 5.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 31.9% today to 28.7% in 3 years time.

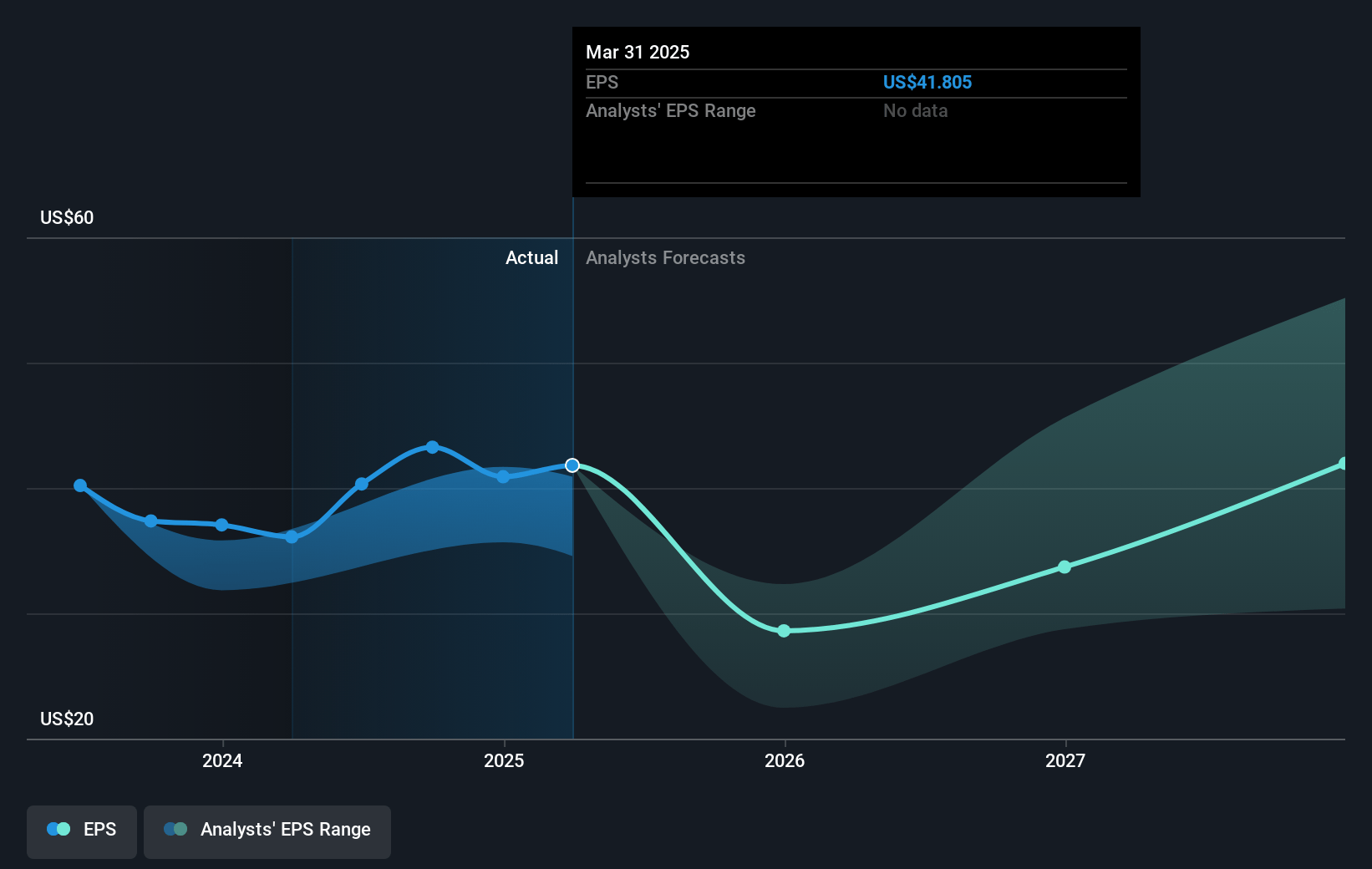

- Analysts expect earnings to reach $4.7 billion (and earnings per share of $45.1) by about May 2028, up from $4.5 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $5.8 billion in earnings, and the most bearish expecting $2.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.2x on those 2028 earnings, up from 13.1x today. This future PE is greater than the current PE for the US Biotechs industry at 18.3x.

- Analysts expect the number of shares outstanding to decline by 2.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.21%, as per the Simply Wall St company report.

Regeneron Pharmaceuticals Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Declining U.S. net sales of EYLEA due to increased competition and the reliance on low-cost off-label Avastin could continue to pressure revenues and margins.

- Regulatory setbacks such as the complete response letter from the FDA regarding the EYLEA HD pre-filled syringe highlight potential delays and costs that can affect earnings.

- The funding gap at co-pay assistance foundations, affecting accessibility of EYLEA for patients, if not resolved, could lead to further revenue declines.

- Continued reliance on third-party manufacturers and component suppliers for a range of products, which has led to CRLs, represents an ongoing risk to product approvals, potentially delaying revenue streams.

- The commercial pressures on established products like EYLEA, coupled with potential increased pricing pressures and regulatory scrutiny, could negatively impact profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $800.13 for Regeneron Pharmaceuticals based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $979.0, and the most bearish reporting a price target of just $535.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $16.3 billion, earnings will come to $4.7 billion, and it would be trading on a PE ratio of 20.2x, assuming you use a discount rate of 6.2%.

- Given the current share price of $558.52, the analyst price target of $800.13 is 30.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.