Key Takeaways

- Advancing Phase III trials and successful SERENITY outcomes could expand market access and boost revenue through FDA approvals and new partnerships.

- Cost reduction initiatives and strategic financing strengthen financial stability, improving margins and enabling further commercialization efforts.

- Financial difficulties are evident through revenue declines, increased costs, reduced expenses, and strategic financing needs, highlighting potential challenges to earnings growth and sustainability.

Catalysts

About BioXcel Therapeutics- A commercial-stage biopharmaceutical company, engages in utilizing artificial intelligence approaches to develop transformative medicines in neuroscience and immuno-oncology.

- The advancement of pivotal Phase III trials for BXCL501, targeting agitation in bipolar disorder and schizophrenia as well as Alzheimer's dementia, represents a significant growth opportunity. Successful trials could lead to new FDA approvals, expanding the addressable market, and increasing future revenue potential.

- The ongoing SERENITY At-Home trial, if successful, may unlock partnership opportunities for the agitation market in home settings, potentially increasing revenue streams and enhancing market penetration.

- The continuation of strategic financing alternatives and partnerships aims to strengthen the company's balance sheet, which could improve investor confidence and provide the financial stability needed to reach data readouts and commercialize new treatments.

- The cost reduction initiatives, including reprioritization efforts and a reduction in force, have significantly decreased research and development as well as selling, general, and administrative expenses. This is likely to improve net margins and reduce overall cash burn, enhancing future earnings potential.

- The potential to expand the therapeutic use of BXCL501 through externally funded studies, such as the Department of Defense grant for acute stress disorder, validates its broad therapeutic potential and could open additional revenue streams in new treatment areas.

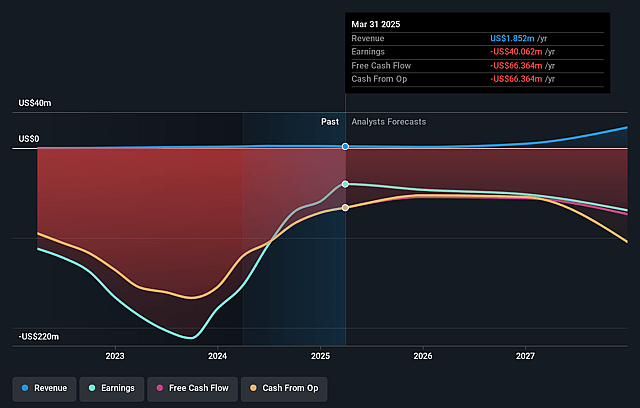

BioXcel Therapeutics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming BioXcel Therapeutics's revenue will grow by 224.4% annually over the next 3 years.

- Analysts are not forecasting that BioXcel Therapeutics will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate BioXcel Therapeutics's profit margin will increase from -2163.2% to the average US Biotechs industry of 10.5% in 3 years.

- If BioXcel Therapeutics's profit margin were to converge on the industry average, you could expect earnings to reach $6.7 million (and earnings per share of $0.95) by about July 2028, up from $-40.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.9x on those 2028 earnings, up from -0.3x today. This future PE is greater than the current PE for the US Biotechs industry at 16.5x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.6%, as per the Simply Wall St company report.

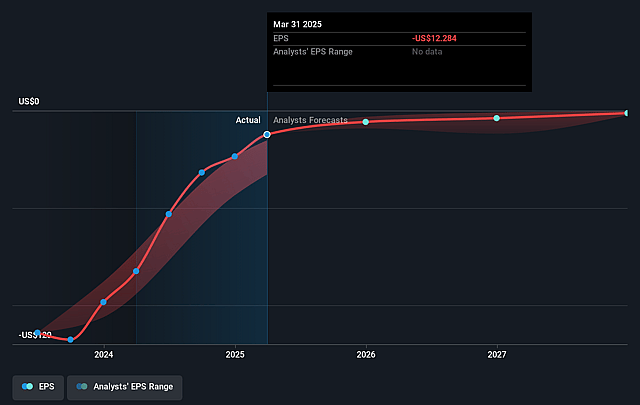

BioXcel Therapeutics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue from IGALMI decreased during the third quarter of 2024 compared to 2023, primarily due to the timing of reorders from existing customers, which could impact future revenue stability.

- The cost of goods sold increased significantly due to higher noncash charges for reserves for excess or obsolete inventory, which could negatively affect net margins.

- Significant reductions in research and development expenses and selling, general, and administrative expenses due to reprioritization and workforce reduction efforts may indicate financial stress, affecting the company’s ability to grow earnings in the future.

- The company's third-quarter net loss of $13.7 million, although reduced from the previous year, and the operational cash usage of $16.3 million despite these reductions, could impact its short-term financial sustainability and earnings.

- The company is actively seeking to strengthen its balance sheet and exploring strategic financing alternatives, which highlights potential liquidity risks that could affect future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $23.25 for BioXcel Therapeutics based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $66.0, and the most bearish reporting a price target of just $1.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $63.2 million, earnings will come to $6.7 million, and it would be trading on a PE ratio of 33.9x, assuming you use a discount rate of 11.6%.

- Given the current share price of $1.8, the analyst price target of $23.25 is 92.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.