Narratives are currently in beta

Key Takeaways

- Strategic focus on original programming and live events aims to boost subscriber growth and retention, driving potential revenue increases.

- Innovative ad formats and pricing strategies target enhanced user engagement and satisfaction, aiming for sustained long-term revenue growth.

- Rising competition and alternative platforms may hinder Netflix's market share growth, while economic and strategic challenges could strain revenue and engagement.

Catalysts

About Netflix- Provides entertainment services.

- Netflix's plan to grow engagement through original programming across multiple countries is expected to drive membership growth, which could lead to increased revenue. Streaming hits from global markets demonstrate their potential to capture untapped demand.

- The expansion of Netflix's advertising business, particularly in untapped markets and the introduction of innovative ad formats, is likely to become a more significant contributor to revenue growth, aligning with a broader trend toward monetizing user engagement.

- Investments in live events, including sports and exclusive shows, could strengthen subscriber retention and acquisition, supporting revenue growth by providing unique, high-engagement content.

- Continuous improvement in product experiences, such as the revamped TV homepage, is anticipated to enhance user engagement and satisfaction, potentially stabilizing or increasing average revenue per member (ARM) by making the platform more attractive.

- Netflix's pricing strategy, which focuses on delivering value before implementing price increases, aims to drive long-term revenue growth while maintaining customer satisfaction and reducing churn.

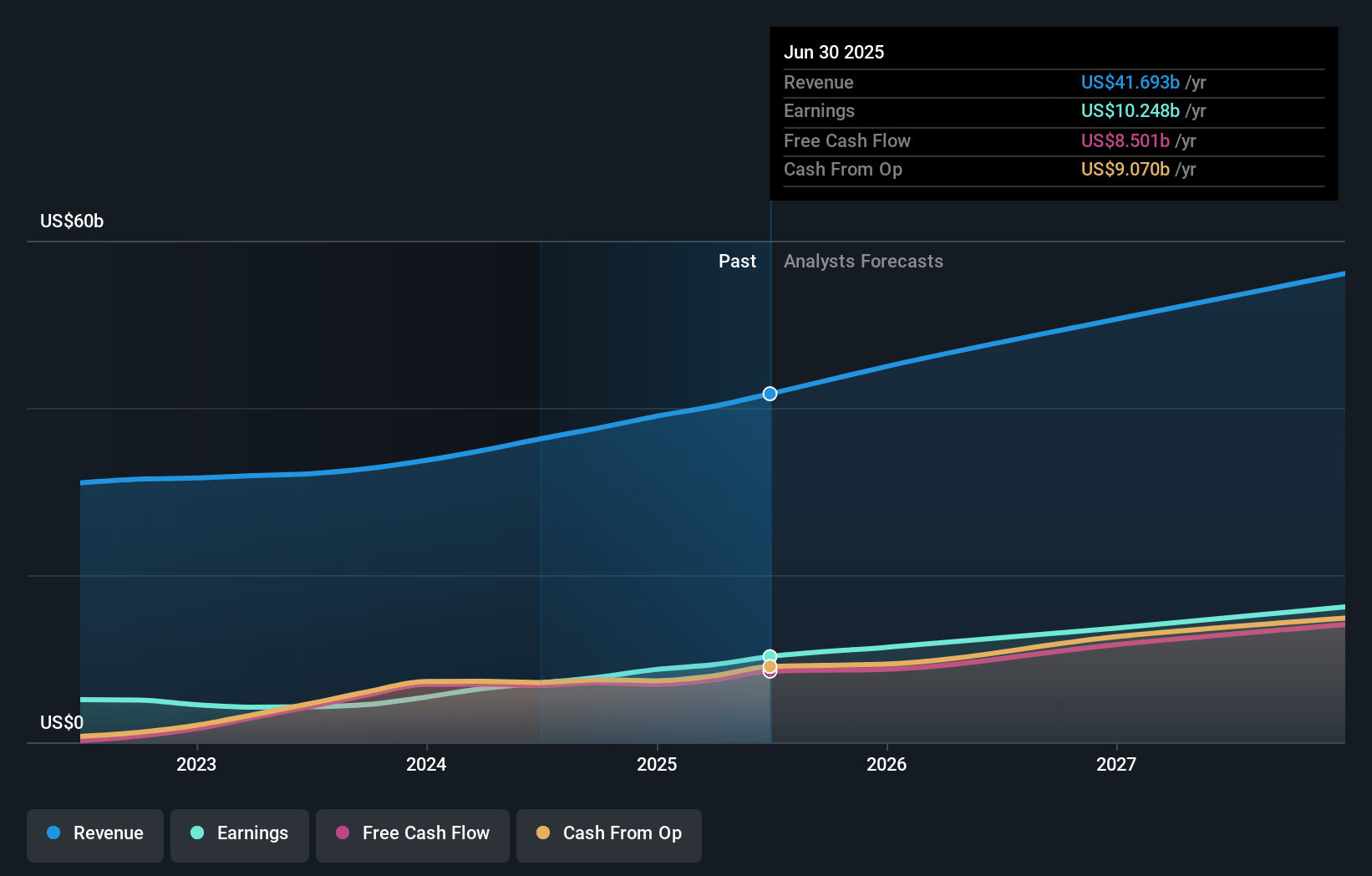

Netflix Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Netflix's revenue will grow by 11.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 20.7% today to 26.1% in 3 years time.

- Analysts expect earnings to reach $13.5 billion (and earnings per share of $31.98) by about January 2028, up from $7.8 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.8x on those 2028 earnings, down from 48.3x today. This future PE is greater than the current PE for the US Entertainment industry at 19.4x.

- Analysts expect the number of shares outstanding to decline by 0.32% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.42%, as per the Simply Wall St company report.

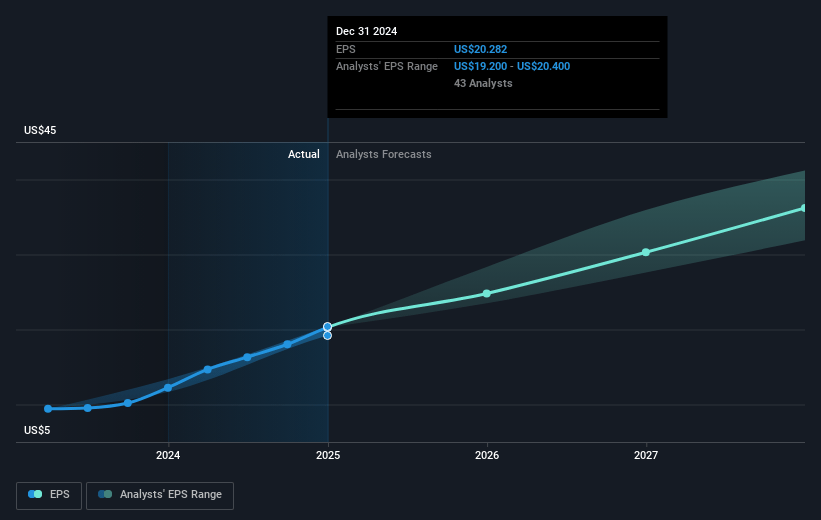

Netflix Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increased competition from major players in the entertainment industry and the rise of alternative media platforms like YouTube could impact Netflix's ability to grow its market share, affecting revenue and engagement.

- Netflix's ability to monetize its advertising inventory effectively is still developing, which could impede its potential revenue growth from ads in the near term.

- Economic factors, including foreign exchange rate fluctuations and potential price sensitivity among consumers, particularly with membership price increases, could impact revenue and net margins.

- The impact of Hollywood labor disputes, which have previously caused production delays, might continue to affect content delivery schedules, potentially impacting viewer engagement and overall retention rates.

- Netflix's significant investments in new initiatives like live events and gaming involve long-term development timelines and could strain earnings if these initiatives do not generate expected returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $845.73 for Netflix based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $1100.0, and the most bearish reporting a price target of just $550.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $51.9 billion, earnings will come to $13.5 billion, and it would be trading on a PE ratio of 32.8x, assuming you use a discount rate of 7.4%.

- Given the current share price of $879.19, the analyst's price target of $845.73 is 4.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

MI

Content Lead

Industry Consolidation and Internal Initiatives Will Support Subscriber growth

Key Takeaways Possible consolidation in the streaming market will benefit NFLX with better negotiating leverage Internal initiatives of ad-plans and paid sharing will drive user and revenue growth ARPM will increase due to future price increases and advertising revenue Advertising dollars will transition from Cable TV to NFLX as its ad-supported members base grows Discipline on content costs will increase net margins and push future earnings and cash flows higher Catalysts Industry Catalysts Consolidation Of Content In The Streaming Market After 25 years of expensive growth, Netflix has now become the most dominant, profitable streaming player in the world. With 238m subscribers, trailing 12 month revenues of $32bn and cash flows of $4.6bn (all as of June 30 2023), the company has reached scale economics that allow the streaming model to work profitably.

View narrativeUS$797.74

FV

7.6% overvalued intrinsic discount13.00%

Revenue growth p.a.

20users have liked this narrative

0users have commented on this narrative

15users have followed this narrative

about 2 months ago author updated this narrative

RI

Equity Analyst and Writer

Scale, Operating Leverage And Ad Plans Will Drive EPS Growth

Key Takeaways Netflix ad-supported plans will drive new revenue Revenue per user will decrease in short term from ad plans, but increase longer term Margins will continue to improve as costs grow slower than revenue (operating leverage) User growth expected from password sharing crackdown I believe these 3 catalysts will result in $52bn in revenue and $12.5bn profit by 2028 Catalysts Industry Catalysts There is Room For More Than One Streaming Platform The video streaming industry has become very competitive, and the market has been hyper focused on the question of “who will win the streaming war.” I don’t think this is a winner takes all situation, and there is room for a handful of platforms. There are pros and cons to each platform and many households end up subscribing to two or three platforms.

View narrativeUS$936.00

FV

8.3% undervalued intrinsic discount11.50%

Revenue growth p.a.

11users have liked this narrative

0users have commented on this narrative

13users have followed this narrative

2 months ago author updated this narrative