Key Takeaways

- Expanding premium ad products and programmatic solutions could drive higher ad revenue and boost the company’s financial performance.

- Investment in sales teams and advanced data analytics is poised to enhance advertiser retention, regional revenue, and earnings growth.

- Declining national and local advertising revenue, coupled with rising expenses and underutilized assets, threatens National CineMedia's future growth and short-term earnings stability.

Catalysts

About National CineMedia- Through its subsidiary, National CineMedia, LLC, operates cinema advertising network in North America.

- The strong performance in the box office, with significant year-over-year growth in attendance and revenue driven by hit movie releases, positions NCM well to capitalize on increased cinema traffic and potentially boost advertising revenue. This is likely to impact future revenue positively.

- The strategic focus on expanding the premium advertising product, such as Platinum, which is in high demand among advertisers, is expected to drive higher revenue from premium screen allocations, positively affecting overall revenue.

- The re-investment into local and regional sales teams aims to revitalize this previously strong segment of the business, potentially increasing local and regional advertising revenue and impacting net margins as scale is achieved.

- The company's advancements in data analytics through NCMx, allowing for precise audience targeting and measurement of advertising effectiveness, can lead to increased advertiser retention and new client acquisition, contributing to higher revenue and improved earnings.

- The introduction of programmatic and self-serve advertising solutions is expected to attract more advertisers by offering flexibility and efficiency, leading to a growth in advertising revenue and enhancing overall financial performance.

National CineMedia Future Earnings and Revenue Growth

Assumptions

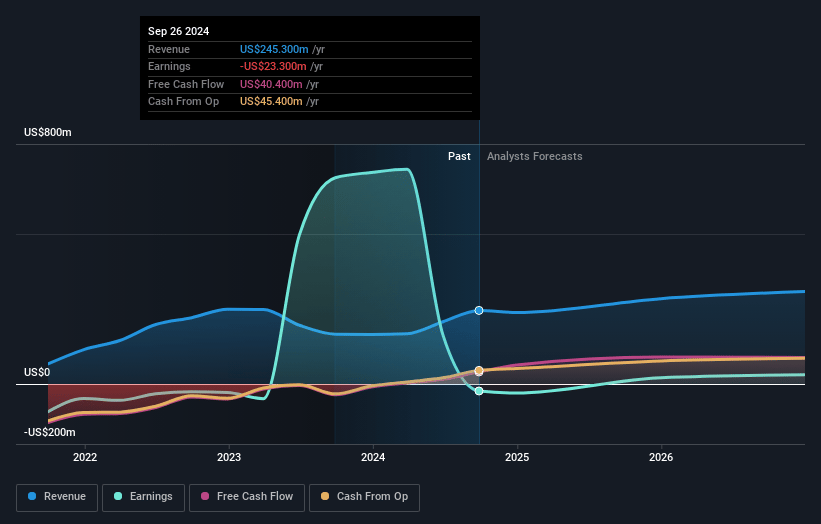

How have these above catalysts been quantified?- Analysts are assuming National CineMedia's revenue will grow by 9.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from -9.3% today to 8.1% in 3 years time.

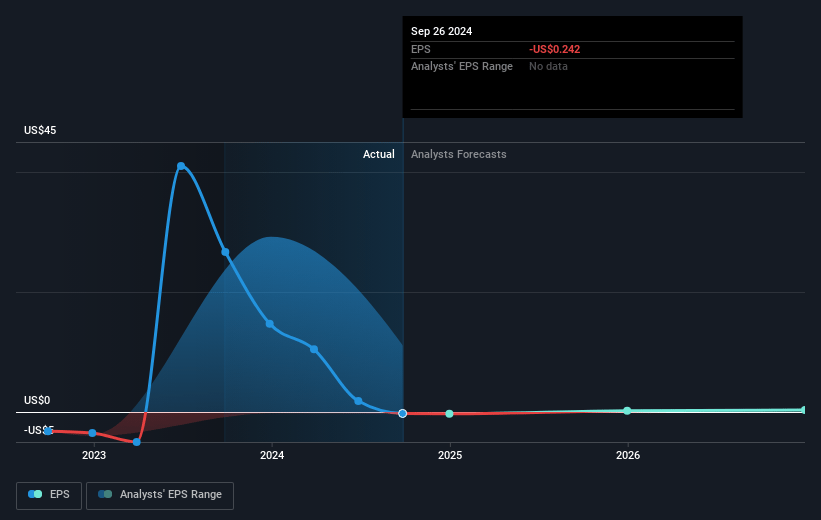

- Analysts expect earnings to reach $25.4 million (and earnings per share of $0.28) by about April 2028, up from $-22.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 32.2x on those 2028 earnings, up from -24.9x today. This future PE is greater than the current PE for the US Media industry at 13.6x.

- Analysts expect the number of shares outstanding to decline by 1.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.22%, as per the Simply Wall St company report.

National CineMedia Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decrease in national advertising revenue in the fourth quarter of 2024, driven by a 22% decrease in utilization despite flat pricing, could impact future revenue growth.

- The impact of an unfavorable mix of harder-to-monetize G and PG-rated movies could reduce net margins as higher-value advertising slots remain underutilized.

- Delays in advertising spend due to government spending reductions and tariff uncertainties could lead to volatility in quarterly earnings.

- Lower local and regional advertising revenue resulting from reduced contract sizes and a cautious approach by small businesses could affect overall revenue performance.

- Expected increases in SG&A expenses and capital expenditures to drive future growth may pressure net margins and earnings in the short term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $7.5 for National CineMedia based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $313.3 million, earnings will come to $25.4 million, and it would be trading on a PE ratio of 32.2x, assuming you use a discount rate of 6.2%.

- Given the current share price of $5.84, the analyst price target of $7.5 is 22.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.