Key Takeaways

- Strategic shifts towards mini and short dramas aim to boost user engagement and market adaptability, enhancing membership and advertising revenue.

- Overseas expansion and AI-driven efficiency improvements could significantly enhance revenue growth and net margins for reinvestment.

- Increasing competition, macroeconomic challenges, and strategic content shifts may impact revenue stability, net margins, and international market penetration efforts.

Catalysts

About iQIYI- Provides online entertainment video services in the People’s Republic of China.

- iQIYI's strategic pivot to include mini and short dramas could enhance user engagement and retention by catering to evolving consumer preferences, potentially boosting membership revenue and advertising growth.

- The introduction of a subscription model alongside free mini dramas is designed to aid in subscriber retention and acquisition, potentially stabilizing membership revenue, especially during macroeconomic uncertainties.

- The upcoming launch of over 300 new titles for 2024 and 2025 aims to capture diverse audience segments, which could drive increased viewership and ultimately improve advertising revenue and subscriber numbers.

- iQIYI's overseas market expansion, particularly in regions with high membership revenue growth like Hong Kong, Brazil, and Australia, suggests potential for significant revenue growth.

- The use of advanced AI technology to improve content production efficiency and reduce costs could lead to better net margins over time, allowing for reinvestment in growth initiatives.

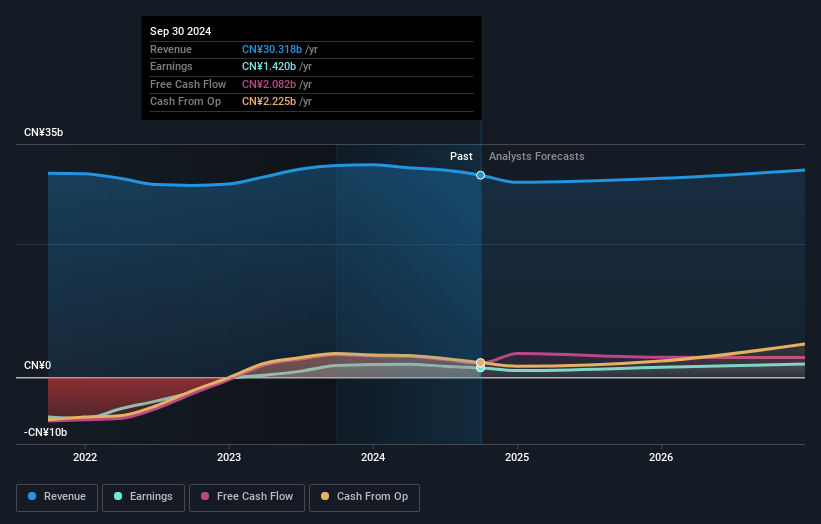

iQIYI Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming iQIYI's revenue will decrease by 0.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.7% today to 6.8% in 3 years time.

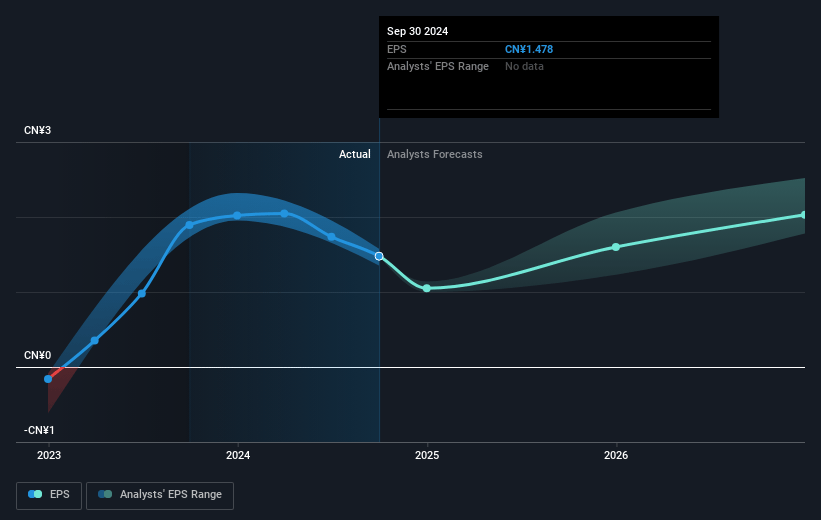

- Analysts expect earnings to reach CN¥2.1 billion (and earnings per share of CN¥2.14) by about January 2028, up from CN¥1.4 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.5x on those 2028 earnings, up from 10.9x today. This future PE is lower than the current PE for the US Entertainment industry at 19.0x.

- Analysts expect the number of shares outstanding to grow by 1.28% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.97%, as per the Simply Wall St company report.

iQIYI Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's membership revenues decreased due to a limited supply of certain popular content genres, macroeconomic headwinds, and competition from other entertainment options, potentially affecting future revenue stability.

- Advertising revenue saw a decline, particularly from the brand ad sector, influenced by reduced investments in variety shows due to economic uncertainties, which may further impact net margins as advertising is a critical income stream.

- The company acknowledges macroeconomic headwinds affecting consumer spending habits and the increasing competition from diverse entertainment options, which could pressure overall revenue growth and earnings potential.

- There is a risk that the company's strategic focus on mini and short dramas, while seeing popularity, might require substantial investment shifts from traditional long-form content, impacting cost management and potentially reducing net margins if returns don't meet expectations.

- Although the company is hopeful about its premium content's appeal in international markets, there are risks associated with its ability to effectively penetrate these markets and maintain its membership and revenue growth, which is central to their financial success.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $2.49 for iQIYI based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $3.62, and the most bearish reporting a price target of just $1.79.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥31.1 billion, earnings will come to CN¥2.1 billion, and it would be trading on a PE ratio of 11.5x, assuming you use a discount rate of 11.0%.

- Given the current share price of $2.23, the analyst's price target of $2.49 is 10.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives