Catalysts

About WD-40

WD-40 develops and markets branded maintenance products for household, industrial and professional uses across a global distribution footprint.

What are the underlying business or industry changes driving this perspective?

- Although the company sees a large remaining global market for its flagship multi-use product and specialist line, slower than targeted growth in key regions like the Americas and Asia Pacific suggests that realizing the estimated benchmark opportunity may take longer than planned, which could constrain revenue growth and delay operating leverage.

- While premium formats such as Smart Straw and EZ Reach and the broader WD-40 Specialist range support higher average selling prices, mix headwinds between direct and distributor markets and across product tiers may cap further gross margin expansion above the current 55 percent level, limiting future improvement in net margins.

- Although e-commerce and digital engagement are growing at a double digit rate and should enhance brand reach over time, the lumpy ordering patterns of distributor markets and potential channel conflict with traditional retail partners could increase sales volatility and blunt near term earnings growth.

- While investments in AI enabled systems, global sourcing and supply chain optimization have recently delivered material cost savings, the need to keep funding technology, risk management and compliance in a more complex operating environment may keep the cost of doing business elevated, dampening the pace of adjusted EBITDA margin recovery.

- Despite long runway opportunities in emerging and underpenetrated markets like India, Latin America and Southeast Asia, geopolitical risk, currency volatility and uneven macroeconomic conditions in these regions could periodically disrupt volume growth and offset the benefits to consolidated revenue and earnings per share.

Assumptions

This narrative explores a more pessimistic perspective on WD-40 compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

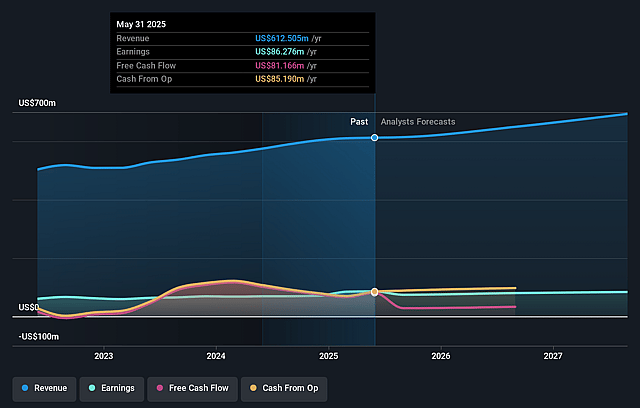

- The bearish analysts are assuming WD-40's revenue will grow by 6.8% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 14.6% today to 13.1% in 3 years time.

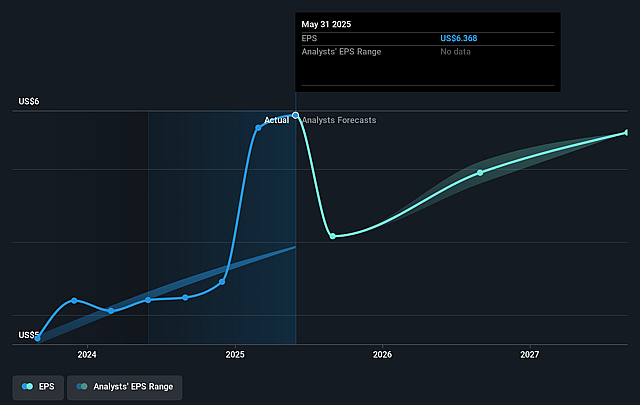

- The bearish analysts expect earnings to reach $98.6 million (and earnings per share of $7.41) by about January 2029, up from $90.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 38.3x on those 2029 earnings, up from 29.3x today. This future PE is greater than the current PE for the US Household Products industry at 17.1x.

- The bearish analysts expect the number of shares outstanding to decline by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.96%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Persistent underperformance versus long term regional growth targets in the Americas and Asia Pacific, where fiscal 2025 growth of 4% and 6% respectively lag the stated 5% to 8% and 10% to 13% objectives, could signal that the remaining benchmark market opportunity is harder to capture than expected. This may limit long run revenue expansion and earnings growth.

- Reliance on premiumization and specialist formats to sustain gross margin above 55 percent may be challenged by ongoing adverse sales mix between direct and distributor markets, bulk and higher value products and different regions. Management already cites this as a 140 basis point headwind, which could potentially cap further margin expansion and slow growth in net income.

- The strategy to divest Home Care and cleaning brands and concentrate on maintenance products increases dependence on a narrower set of categories. Any cyclical slowdown in industrial or household maintenance demand or a structural shift to competing technologies could therefore disproportionately impact consolidated revenue and reduce earnings resilience over the long term.

- Long term geopolitical tensions, tariff uncertainty, foreign exchange volatility and uneven macroeconomic conditions in key emerging markets such as Latin America, Mexico, China and broader Asia distributor markets could continue to disrupt order timing and volume. This may introduce structural volatility into regional sales growth and compress operating margins through higher logistics and compliance costs.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for WD-40 is $229.0, which represents up to two standard deviations below the consensus price target of $264.5. This valuation is based on what can be assumed as the expectations of WD-40's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $300.0, and the most bearish reporting a price target of just $229.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $755.0 million, earnings will come to $98.6 million, and it would be trading on a PE ratio of 38.3x, assuming you use a discount rate of 7.0%.

- Given the current share price of $196.76, the analyst price target of $229.0 is 14.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on WD-40?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.