Last Update 15 Jul 26

Fair value Increased 8.88%WDFC: Raised Outlook And Input Cost Pressures Will Shape Fairly Valued Shares

Analysts have lifted their blended price target on WD-40 to about $272 from roughly $250, citing a solid Q3 beat, expectations for higher sales despite near term margin pressure from input costs, and recent upward revisions to Street targets to $245 and $305.

Analyst Commentary

Recent research on WD-40 highlights a mix of optimism around execution in Q3 and caution on what higher input costs could mean for margins and earnings quality over the next several quarters.

Bullish Takeaways

- Bullish analysts point to WD-40's Q3 EPS of $0.77 coming in above consensus and their own estimates as evidence of strong recent execution and earnings power at the current valuation.

- The Q3 report is described as solid, with top line strength and upside to gross margins contributing to meaningful flow through against a relatively stable cost structure.

- Higher blended price targets, including moves to $245 and $305, reflect confidence that recent performance and revised estimates can support a higher valuation range.

- One firm links its higher target to expectations that updated FY26 estimates will move up, which it views as supportive for WD-40's medium term growth profile in its models.

Bearish Takeaways

- Bearish analysts highlight that higher input costs are expected to squeeze margins through at least the first half of FY27, which could pressure earnings even as sales move higher.

- The impact of rising input costs is expected to hit with a lag into Q4, raising questions about how durable recent margin strength will be.

- The full year guidance raise is flagged as being less than the Q3 beat implies, suggesting some give back to the upside and limiting how much Q3 strength can be extrapolated.

- Hold ratings alongside higher price targets indicate that some analysts see WD-40's stock as closer to fairly valued after the recent move, with less room for execution missteps.

What’s in the News for WD-40

- WD-40 Company reported fiscal Q3 2026 net sales up 24% year over year and operating income up 47%, with maintenance products accounting for 97% of total sales, according to recent earnings coverage.

- Adjusted Q3 2026 EPS came in at $2.33 versus analyst expectations of about $1.58, and management raised full year 2026 revenue guidance to a range of $675 million to $690 million and adjusted EPS guidance to $6.05 to $6.35, per the same reports.

- The company authorized a new $100 million share repurchase program to begin in September 2026 and maintained its $1.02 quarterly dividend, while continuing to emphasize higher margin maintenance and specialist products over lower margin homecare and cleaning brands, based on recent news coverage.

- On July 10, 2026, WD-40's stock price moved up 22.7%, with reports citing strong investor interest, potential growth initiatives, favorable market conditions, and a GF Score of 94 out of 100 as indicators of financial strength, according to GuruFocus.

- Recent filings show that from March 1, 2026 to May 31, 2026, WD-40 repurchased 31,250 shares for $6.76 million and has completed buybacks of 193,425 shares for $42.94 million under the program announced on July 10, 2023, while also disclosing that CFO Sara K. Hyzer intends to move into the role of Division President, Americas after a successor is appointed.

Valuation Changes for WD-40

- Fair Value: The updated blended fair value estimate has moved from $249.50 to about $271.67, a change of roughly 9%.

- Discount Rate: The model discount rate is essentially unchanged, holding around 7.11%.

- Revenue Growth: The assumed long term annual revenue growth rate has risen from about 6.24% to roughly 6.99%.

- Net Profit Margin: The projected net profit margin has been revised from about 12.81% to roughly 10.64%, indicating a lower earnings share on each $ of sales in the model.

- Future P/E: The assumed future P/E multiple has moved higher from about 40.8x to roughly 49.4x.

Key Takeaways

- Geographic expansion and direct market strategies in EIMEA indicate potential for sustained revenue growth and enhanced margins.

- Premiumization and divestment of less profitable brands aim to boost overall margins and refocus the company on higher-growth opportunities.

- Challenges such as divestiture uncertainty, currency fluctuations, and regional market conditions could affect WD-40's revenue growth and profit margins.

Catalysts

About WD-40- Develops and sells maintenance products, and homecare and cleaning products in North America, Central and South America, Asia, Australia, Europe, India, the Middle East, and Africa.

- The significant volume growth in Europe, India, the Middle East, and Africa (EIMEA), particularly driven by the transition to direct markets in areas like Brazil and potential new strategies for more markets, suggests continued revenue growth. This geographic expansion strategy will likely enhance revenue over the coming years.

- The company's focus on premiumization of products, with targets for a compound annual growth rate for premium products exceeding 10%, is poised to improve net margins by shifting the product mix towards higher-margin offerings.

- WD-40’s strategy to divest its less profitable home care and cleaning brands is expected to position the company as a higher growth and higher gross margin enterprise, ultimately boosting operational margins and net margins once complete.

- Supply chain optimization initiatives, such as improved efficiencies and cost savings through strategic supplier partnerships, are projected to mitigate potential tariff impacts and support margin expansion, contributing positively to gross margins.

- The focus on boosting digital commerce and expanding brand awareness via e-commerce platforms is anticipated to drive revenue growth and improve earnings by capitalizing on new customer acquisition and sales channels.

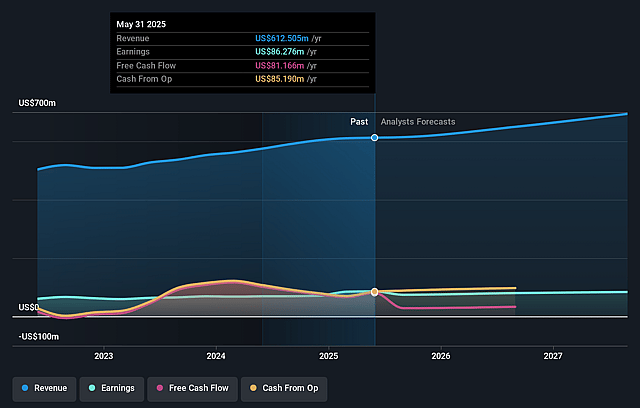

WD-40 Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming WD-40's revenue will grow by 7.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 13.2% today to 10.6% in 3 years time.

- Analysts expect earnings to reach $87.9 million (and earnings per share of $6.73) by about July 2029, down from $89.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 50.0x on those 2029 earnings, up from 37.6x today. This future PE is greater than the current PE for the US Household Products industry at 20.7x.

- Analysts expect the number of shares outstanding to decline by 0.71% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Uncertainty around the anticipated divestiture of WD-40's home care and cleaning business, which may impact revenue and operating income if not successfully completed as planned.

- Foreign currency exchange rate fluctuations present a headwind, impacting net sales and operating income as highlighted by currency-adjusted sales figures.

- Challenges in the Asia Pacific region, such as the 1% sales decline and weaker market conditions, could affect total revenue growth.

- Potential inflationary pressures and tariff impacts may necessitate price adjustments, potentially affecting profit margins and overall earnings.

- Higher operating expenses, particularly related to employee costs and brand-building activities, have increased the cost of doing business as a percentage of net sales, impacting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $271.67 for WD-40 based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $305.0, and the most bearish reporting a price target of just $245.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $826.4 million, earnings will come to $87.9 million, and it would be trading on a PE ratio of 50.0x, assuming you use a discount rate of 7.1%.

- Given the current share price of $249.12, the analyst price target of $271.67 is 8.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on WD-40?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.