Last Update 01 Jul 26

Fair value Decreased 10%WDFC: Mixed Research And Fresh Coverage Will Shape Fairly Balanced Outlook

Analysts have reduced their fair value estimate for WD-40 by $30 to $270, reflecting updated assumptions around discount rates, growth, profitability and future P/E multiples following recent mixed Street research.

Analyst Commentary

Bullish analysts see the recent fair value trim for WD-40 as a recalibration rather than a shift in the long term story, with updated targets and fresh coverage framed around the company’s ability to execute on its core brands and pricing strategy.

Some research has focused on aligning price targets with revised discount rates, profit assumptions and future P/E multiples, while new bullish coverage has highlighted what analysts view as an attractive entry point for investors who are comfortable with WD-40’s current valuation framework.

Bullish analysts also point to the stock’s liquidity profile and historical brand strength as reasons to keep WD-40 on the radar, even as they incorporate more conservative modeling into their fair value work.

Bullish Takeaways

- Bullish analysts emphasize that their updated fair value work still supports upside potential relative to current pricing, even after a US$30 reduction in the target level.

- Supportive coverage highlights what analysts see as resilient demand for WD-40’s core maintenance products, which they argue can underpin earnings quality over time.

- Positive commentary frames WD-40’s valuation as reasonable when factoring in the company’s long operating history and brand recognition in its category.

- Fresh bullish coverage suggests that, in analysts’ view, the recent adjustment to fair value can help set more realistic expectations and reduce the risk of future de-rating tied to P/E assumptions.

What’s in the News for WD-40

- WD-40 shares moved 6.8% higher after Northcoast Research initiated coverage with a "Buy" rating and a US$265 price target, according to the recent analyst report.

- The Northcoast initiation aligns with an average "overweight" rating from other analysts. This reinforces the recent focus on WD-40’s valuation and analyst coverage trends.

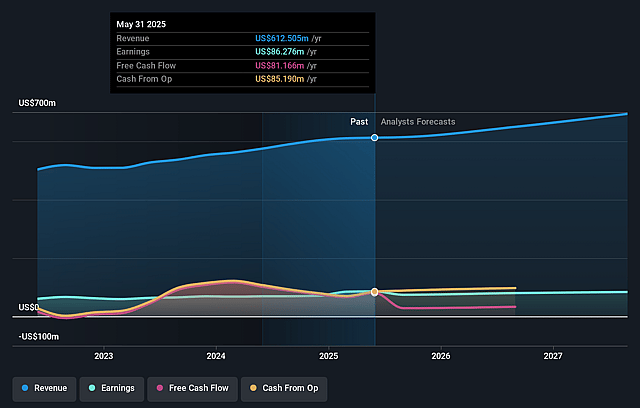

- WD-40 reaffirmed earnings guidance for Fiscal Year 2026, projecting net sales between US$630 million and US$655 million and operating income between US$103 million and US$110 million, with diluted EPS expected in a range of US$5.75 to US$6.15.

- The company reported that from December 1, 2025 to February 28, 2026, it repurchased 38,175 shares for US$7.99 million, bringing total buybacks under the July 10, 2023 authorization to 162,175 shares for US$36.18 million.

- WD-40 announced that current Chief Financial Officer Sara K. Hyzer plans to transition to Division President, Americas after a new CFO is appointed, while continuing to serve as CFO until a successor is in place.

Valuation Changes for WD-40

- Fair Value was reduced from $300.00 to $270.00, reflecting a decrease of $30.00 in the updated assessment.

- The Discount Rate rose slightly from 6.96% to 7.11%, implying a modestly higher required return in the new model.

- Revenue Growth edged higher from 6.67% to 6.97%, with analysts now using a slightly stronger top line assumption for WD-40.

- The Net Profit Margin was revised up from 13.09% to 13.27%, indicating a small uplift in expected profitability.

- The Future P/E was reduced from 50.22x to 41.71x, signaling that the updated fair value is based on a lower earnings multiple.

Catalysts

About WD-40

WD-40 develops and markets high performance maintenance and specialty products that protect, lubricate and preserve equipment for consumers and professionals worldwide.

What are the underlying business or industry changes driving this perspective?

- The company has captured only about one quarter of its estimated global potential for WD-40 Multi-Use Product and a little over one tenth for WD-40 Specialist, and continued geographic expansion and deeper penetration in large markets such as India, China and Latin America are key focus areas for pursuing additional revenue growth and potentially expanding earnings power.

- Premium formats like Smart Straw and EZ Reach already account for roughly half of Multi-Use sales and continue to grow at a high single digit to low double digit compound rate, which may steadily lift average selling prices and support gross margin above the current 55 percent level.

- Growth in higher value WD-40 Specialist, with a five year compound annual growth rate above 14 percent and traction across all regions, positions the portfolio to tilt toward more professional and industrial users, supporting mix driven revenue growth and potentially higher net margins.

- Ongoing investments in digital commerce, including AI enabled systems and global e commerce capabilities, are improving brand visibility, data driven marketing and channel reach, and may accelerate top line growth while leveraging the fixed cost base to enhance earnings.

- Supply chain optimization, disciplined global sourcing and the divestiture of lower margin home care and cleaning brands are simplifying the business and freeing resources for core maintenance products, supporting gross margin above 55 percent and contributing to operating income and EPS growth within or above stated guidance ranges.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on WD-40 compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming WD-40's revenue will grow by 7.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 12.5% today to 13.3% in 3 years time.

- The bullish analysts expect earnings to reach $103.4 million (and earnings per share of $7.35) by about July 2029, up from $79.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 42.4x on those 2029 earnings, up from 41.1x today. This future PE is greater than the current PE for the US Household Products industry at 21.0x.

- The bullish analysts expect the number of shares outstanding to decline by 0.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Growth in key regions such as the Americas and Asia Pacific is already running below long-term targets, with Americas revenue growth under the 5 to 8 percent goal and Asia Pacific below the 10 to 13 percent goal. This suggests the large stated addressable markets may prove harder to monetize than expected and could limit future revenue growth and earnings expansion.

- The strategy to divest Home Care and cleaning brands and concentrate even more on maintenance products increases reliance on a single category. Any saturation of WD-40 Multi-Use and Specialist demand or new competitive entrants could pressure pricing power and ultimately constrain revenue and net margin growth.

- Recent margin gains are heavily dependent on lower specialty chemical costs, favorable pricing, and ongoing supply chain savings. Persistent cost volatility, tariffs and higher warehousing and freight expenses, particularly in the Americas, could erode gross margin above 55 percent and reduce profitability and earnings.

- Distributor led growth in Asia Pacific and parts of EMEA introduces volatility in order timing and sales mix. If distributors cut inventories or shift focus due to local macroeconomic or geopolitical shocks, WD-40 could see uneven sales, less favorable product mix and downward pressure on both revenue and gross margin.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for WD-40 is $270.0, which represents up to two standard deviations above the consensus price target of $254.67. This valuation is based on what can be assumed as the expectations of WD-40's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $270.0, and the most bearish reporting a price target of just $229.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $779.1 million, earnings will come to $103.4 million, and it would be trading on a PE ratio of 42.4x, assuming you use a discount rate of 7.1%.

- Given the current share price of $243.64, the analyst price target of $270.0 is 9.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on WD-40?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.